Tydzień w gospodarce

Kategoria: Trendy gospodarczePrzegląd wydarzeń gospodarczych ubiegłego tygodnia (30.05–03.06.2022) – źródło: dignitynews.eu

Debata na temat nowych regulacji dopiero się rozpoczęła. W odredakcyjnym komentarzu The New Republic (TNR) domaga się jasnych reguł w sprawie derywatów. Zwłaszcza CDS (credit default swaps), które pogorszyły sytuację na rynku finansowym w czasie kryzysu w 2008 r. Jednak, jak zauważa autor komentarza, nawet zwolennicy regulacji różnią się poglądem co do ich szczegółowych rozwiązań. Według TNR ustawa powinna zmusić przedsiębiorstwa do wyzbycia się zaległości spowodowanych derywatami. Jednak Chris Dodd zamierza pozostawić pewien margines, zezwalając ubezpieczycielom na posługiwanie się derywatami do zawierania układów z bankami inwestycyjnymi.

Ekonomista zajmujący się rynkami finansowymi i jeden z doświadczonych inwestorów John Mauldin uważa, że CDS powinny podlegać takim samym zasadom jak futures i rynek surowców. Powinien być to zrozumiały i transparentny rynek.

As I have been pounding the table about for years, we need to put CDS on an exchange. ASAP. I am not against CDS, per se. CDS are good things, just like futures. But they must go to a transparent exchange. There need to be position limits, just as there in futures and commodities. There needs to be very transparent pricing and commissions. And someone needs to monitor who owns them and what risks they are taking. Why hasn’t this been done? In a word, money. Banks make huge commissions selling CDS, as much as 2-3%, I am told. If they were on an exchange the commissions would be $10 a round turn. An enormous profit center would get blown up. So, the banks hire lobbyists to persuade Congress not to regulate CDS. Dodd’s bill basically says we will deal with them later.

Obszerną i ciekawą pracę na ten temat publikuje dr Robert Litan z Brookings Institution. Dr Litan nie jest przeciwnikiem nowoczesnych instrumentów finansowych. Ma więcej nadziei niż Mauldin. Twierdzi, że jednak jakaś forma standardowych derywatów zostanie uregulowana.

Fortunately, there is a growing consensus among financial regulators and academic experts about what to do at least with respect to “standardized” derivatives, or those that resemble readily traded stocks or futures contracts, and thus how to help keep financial actors who are heavily engaged in derivatives activities and also run into financial trouble from infecting other institutions and conceivably entire markets.

Omówienie pracy dr Litana zamieszcza Mike Konczal tutaj i tutaj. Mike tłumaczy, co jest kością niezgody tej reformy – przede wszystkim transparencja cenowa przed transakcją i po.

I agree with his recommendations for regulating the over-the-counter derivatives market and especially the credit default swap market(CDS): create a strong presumption for over-the-counter derivatives to go through clearing, and to be traded on an exchange with pre-trade price transparency. Those that can’t should have margins posted and have post-trade price and volume transparency.

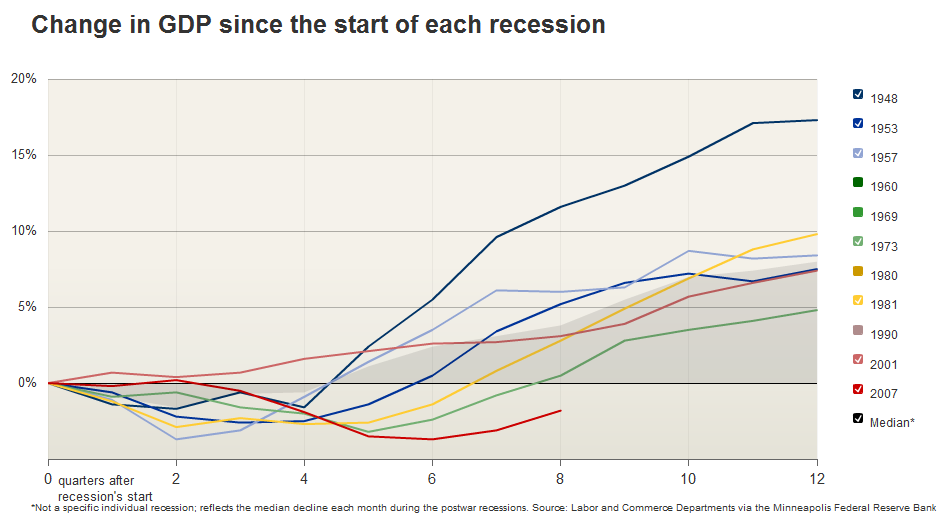

Daily Capitalist podziela pogląd NBER, że recesja jeszcze nie dobiegła końca. I podaje 5 przyczyn, które według niego o tym świadczą, m.in. : 1) program stymulacyjny nie generuje zdrowego procesu gospodarczego; 2) kosumenci będą raczej powstrzymywać się od powrotu do nadmiernych wydatków; 3) kredyt i podaż pieniądza maleją. Dodaje też, że produkcja przemysłowa maleje, a bezrobocie utrzymuje się na wysokim poziomie, obrazując to wykresem porównującym obecną recesję z innymi.

Our recession is the red line and you will see it is at the bottom of all the others which says something about the breadth of it. The NBER pegs December, 2007 as the commencement date of the current recession. While it shows a bottoming out of GDP after 6 months, industrial output and employment has contracted far more than in the other measured cycles.

Ale lekiem na zmniejszenie bezrobocia nie są jednak długoterminowe zasiłki, podkreśla Cynical Economist. A według FROMC przedłużenie i zwiększenie zasiłków mogło nawet spowodować, że bezrobocie urosło do rozmiarów z poprzednich kryzysów.

Mr. Summers is merely reflecting what numerous economic studies have shown. The Federal Reserve Open Market Committee put it this way in its January minutes: “The several extensions of emergency unemployment insurance benefits appeared to have raised the measured unemployment rate, relative to levels recorded in past downturns.” It continued: “Some estimates suggested it could account for 1 percentage point or more of increase in the unemployment rate during the recession.”

Jednak prof. Brad DeLong uważa, że dwucyfrowe bezrobocie należy zwalczać zwiększaniem deficytu.

W ostatnich miesiącach ceny ropy naftowej utrzymywały się w relatywnie wąskim przedziale wahań. Główne czynniki wpływające na rynek tego strategicznego surowca to eskalacja działań wojennych w kilku regionach świata oraz polityka krajów OPEC.

W styczniu 2020 roku Wielka Brytania formalnie opuściła Unię Europejską. Oczekiwane korzyści z brexitu, poza odzyskaniem suwerenności w zakresie kształtowania prawa i zewnętrznych relacji gospodarczych, jednak się nie zmaterializowały. Widoczny jest natomiast spadek wydajności i konkurencyjności brytyjskiej gospodarki, co wpływa także na kondycję rynku pracy.