Tydzień w gospodarce

Kategoria: RaportyPrzegląd wydarzeń gospodarczych ubiegłego tygodnia (16–20.05.2022) – źródło: dignitynews.eu

Historyczną konferencję szefa Fed poprzedziło oświadczenie komitetu ds polityki monetarnej (FOMC), w którym, po raz pierwszy od początku kryzysu, Fed przyznał iż rośnie inflacja, choć, jak dodał, jest to zjawisko przejściowe.

Commodity prices have risen significantly since last summer, and concerns about global supplies of crude oil have contributed to a further increase in oil prices since the Committee met in March. Inflation has picked up in recent months, but longer-term inflation expectations have remained stable and measures of underlying inflation are still subdued. (…) Increases in the prices of energy and other commodities have pushed up inflation in recent months. The Committee expects these effects to be transitory, but it will pay close attention to the evolution of inflation and inflation expectations.

Fed nie będzie kontynuował polityki ilościowego łagodzenia.

In particular, the Committee is maintaining its existing policy of reinvesting principal payments from its securities holdings and will complete purchases of $600 billion of longer-term Treasury securities by the end of the current quarter.

Bernanke chce utrzymać inflację (core inflation) nawet poniżej zakładanego poziomu i z tego faktu jest niezadowolony prof. Paul Krugman

That’s not supposed to be how it works. If you really think that around 2 percent inflation is right (I’d prefer 4, but that’s a different issue), you’re supposed to view 1 percent inflation as being just as bad as 3 percent; in a situation in which inflation is below the target rate, you’re supposed to see a rise in that rate as a good thing. And correspondingly, if you’re where we are now, with below target core inflation and high unemployment, all lights should be flashing green for expansion.

Instead, however, it’s clear that below-target inflation is considered no big deal, but that the Fed is extremely averse to seeing inflation rise above target, even temporarily

Podobny pogląd prezentuje prof. Brad DeLong.

To me the most surprising thing about Chairman Bernanke’s press conference was his apparent abandonment of that 2 percent per year inflation target.

I see no signs anywhere in the marketplace that there is any threat of rising inflation expectations. He stated that he was unwilling to undertake more stimulative policies because “it is not clear we can get substantial improvements in payrolls without some additional inflation risks.”

Profesor Tim Duy zwraca uwagę na fakt, że Bernanke zdawał się ostrzegać przed wzrostem inflacji płac.

The most interesting comments came in response to questions about whether the Fed should do more to lower unemployment and if QE2 is effective, shouldn’t the program continue? Here was a more hawkish Bernanke. As I noted earlier, growth forecasts returned to the pre-QE2 range, which should be a red flag. Unemployment remains high, with only moderate job creation. Core-inflation remains low, while the impulse from commodity prices on headline inflation is expected to be temporary. Finally, he claims that QE2 was in fact effective. So why not do more? Because the Fed needs “to pay attention to both sides of the mandate” and the “tradeoffs are less attractive.” Much talk by Bernanke at this point about inflation expectations, and the importance of maintaining those expectations, and not much (none, I think), about the issue (or non-issue) of wage inflation.

Calculated Risk cytuje inny pasus dotyczący niebezpieczeństwa dalszego wzrostu inflacji.

Ezra Klein zdecydował się, w nieco żartobliwym tonie, uzupełnić braki w wypowiedzi Bernanke (warto przeczytać cały tekst).

I have a lot of power. But I’m not a dictator. The Federal Reserve’s Open Market Committee has 12 members. If I’m being generous, five or six of them seriously understand how bad things are right now. And outside these walls, a guy who wrote a book called “End the Fed” now chairs the House committee that oversees us. Sarah Palin appears to be developing strong and incoherent views on monetary policy. Paul Ryan dabbles in this stuff. If I went public with what really needs to be done — buying bonds related to the real economy rather than Treasury bonds, paying a negative rate on bank reserves so they move the money we’ve given them out of our coffers and into the labor market, doing price-level targeting so we make up for the years of sub-2 percent inflation with a few years where inflation is above 2 percent — I’d be strung up tomorrow. I’d go from having the freedom to talk half-measures to maybe — maybe! — having the freedom to take quarter-measures.

And that’s fine. I understand why people are freaked out by the idea of some group of bearded economists getting together to decide what’s going to happen in the economy next year. But you know when exactly you get bearded economists making the big decisions? When Congress becomes too paralyzed and polarized to make them itself. I mean, good Lord. The division of labor here is — or at least is supposed to be — that the Federal Reserve holds interest rates down while Congress spends money to stimulate the economy. Then, in a few years, when the economy is working again, we begin tightening and they begin reducing the deficit. That’s what Japan should’ve done. In fact, I got hired for this job because I was one of the people telling Japan to do it. And now we should be doing it. But we’re not. Or, more precisely, Congress is not.

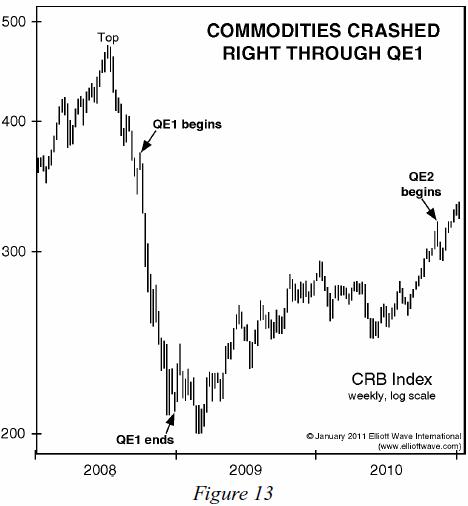

Według części ekonomistów skutki będą jednak odczuwalne jeszcze przez długi czas. Być może tak jak w początkowej fazie QE nastąpi spadek cen surowców naturalnych?

Ben Bernanke twierdził iż jest zadowolony z rezultatów „ilościowego łagodzenia”. Szef Fed do pozytywnych efektów zaliczył wzrost cen akcji (co jest automatycznym skutkiem) ale nie dodał, że nie wzrosły z nich zyski. Według części ekonomistów była to raczej krótkoterminowa korekta cen biorąc pod uwagę długość okresu inwestycji.

Chairman Bernanke: First, I do believe that the second round of securities purchases was effective. We saw that first in the financial markets. The way monetary policy always works is by easing financial conditions. We saw increases in stock prices. We saw reduced spreads in credit markets. We saw reduced volatility. We saw all the changes in financial markets and quite significant changes one would expect if one were doing a normal easing of policy regarding the federal funds rate.

Ważniejsze jednak jaki wpływ ma QE i obecna polityka Fed na dolara – na ten temat Zero Hedge. Fed zwiększył popyt na amerykańskie obligacje. Kupiły je przede wszystkim gospodarstwa domowe, fundusze emerytalne, fundusze inwestycyjne, banki i zagraniczni inwestorzy. Jednak ta inwestycja może, zdaniem części ekonomistów, okazać się nie trafiona.

the emphasis on the measure of Fed ease being the stock of assets owned rather than the flow— by implication the end of QE2 would be the end of additional easing but not the beginning of tightening — the implication for the FX market is that a backing up of asset prices at the end of QE2 would be unwelcome.

All that the Fed has had to do thus far to keep the game going is press the “on” button to its virtual printing press, crediting the account of the U.S. Treasury. In the process, the Fed has kept the demand for U.S. Treasuries high, perhaps deceptively so, attracting with its redolence many classes of buyers, including households, banks, pension funds, insurance companies and foreign investors. Their collective buying has created what we believe to be a profit illusion with many investors mistakenly believing they can continuously reap profits from perpetually falling bond yields and rising bond prices, just as they have had opportunity to do over the past 30 years, amid the great secular bull market for Treasuries and the bond market more generally. (…)

Treasury investors will also realize that not only has QE suppressed the rates they earn on their Treasury holdings, QE promotes financial and economic conditions that hurt Treasury bond holders, primarily because it boosts economic growth and inflation, resulting in confiscation of the skimpy Treasury yields they earn.

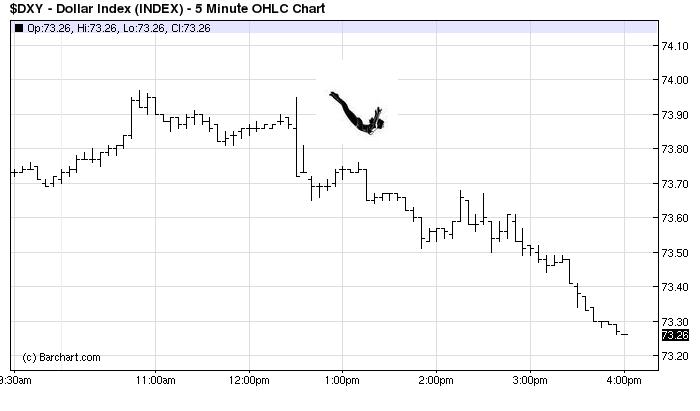

Mimo, że po oświadczeniu FOMC i konferencji Fed rynki poszybowały to dolar zanotował kolejny rekordowy spadek.

Podobny wykres przedstawia Global Macro Monitor.

Daily Reckoning przywołuje op-ed Bernanke opublikowany tuż przed rozpoczęciem QE. Bernanke stwierdza w nim, że w chwili gdy inwestorzy zaczną spodziewać się łatwego zarobku (easy money) wówczas będzie to koniec „ilościowego łagodzenia”.

Also Sprach Analyst porównuje dwa oświadczenia FOMC opublikowane w marcu oraz kwietniu i dostrzega ciekawe różnice co do sformułowań na temat tempa rozwoju gospodarki i interwencji Fed.

Czy rzeczywiście nie ma już instytucji, która koordynowałaby sytuację gospodarczą w skali globalnej? Swoją skuteczność straciły nie tylko G7 ale i niedawno powstałe G20 – twierdzą dwaj ekonomiści Nouriel Roubini i Ian Bremmer. A świat musi się oswoić z faktem, iż globalny porządek będzie dziś, jak to określają, światem G-Zero. Gospodarki światowe straciły wspólny cel gospodarczy i wskazuje na to, że ponownie poważnym problemem stanie się protekcjonizm.Ekonomiści jako przykład przywołują konflikty pomiędzy USA, EU, Brazylią, Chinami i Indiami w kwestii liberalizacji handlu. Bowiem coraz więcej rządów stosuje wszystkie środki by ochronić własnych pracowników i przemysł (konflikt na tle dopłat dla rolników, kwestii ochrony praw własności intelektualnej i sprawy niektórych barier celnych pomiędzy USA a EU). Konflikt pomiędzy USA i Chinami jest wielowymiarowy. Zdaniem autorów jego apogeum nastąpiło w połowie minionej dekady gdy Chiny próbowały kupić najpierw firmę energetyczną Unocal a następnie Dubai Ports by uzyskać częściową kontrolę nad amerykańskimi portami. To był wstęp do działań protekcjonistycznych podjętych na szerszą skalę w Azji i Europie.

Niemniej ważnym problemem jest polityka państw – eksporterów netto energii – zwłaszcza Rosji, która w niedalekiej przeszłości posługiwała się swoimi zasobami jako narzędziem w polityce zagranicznej. Ale najpoważniejszym źródłem konfliktu, według autorów, może być debata na temat środków antykryzysowych:

Innym polem konfliktu może być alternatywa wobec dolara jako waluty rezerwowej. Czy, biorąc pod uwagę dalszą perspektywę, będzie to juan? A w bliższej perspektywie: euro.

Te konflikty w najbliższej dekadzie mogą destablizować relacje gospodarcze w skali globalnej. Bo rządy, w erze postkryzysowej, będą zainteresowane stworzeniem własnych stablilnych systemów ekonomicznych odpowiednich co do własnego politycznego, kulturowego, geopolitycznego i historycznego kontekstu. W erze G Zero każdy rząd będzie próbował stworzyć swój własny, stabilny państwowy kapitalizm.

A na czym on będzie polegał? Także zdaniem prof. Francisa Fukuyamy i dr Nancy Birdsall świat, którego drzwi się właśnie otwierają będzie spolaryzowany. I żadna grupa państw nie będzie dominować przez dłuższy okres (jak miało to miejsce w czasie Zimnej Wojny). Swoją rolę do odegrania będą miały Japonia i USA dostarczając gospodarczych zasobów i idei. A Brazylia, Chiny, Indie, Wietnam czy Południowa Afryka będą głównym motorem gospodarki.

Według autorów, prof. Francisa Fukuyamy i dr Nancy Birdsall. podstawą państwowego kapitalizmu będzie funkcjonalna biurokracja. W tym systemie nie będzie kluczowej roli odgrywał kapitał zagraniczny. Autorzy by podkreślić iż ten element okazał się nieskuteczny w konstruowaniu stabilnego systemu gospodarczego przywołują sformułowanie ekonomisty Arvinda Subramaniana „fetysz kapitału zagranicznego”. Ich zdaniem kombinacja otwartych rynków kapitałowych i nieuregulowany sektor finansowy oznacza katastrofę o czym państwa azjatyckie przekonały się na początku lat 90 a USA i Wielka Brytania podczas obecnego kryzysu. I te kraje, które podążyły za owym „fetyszem kapitału zagranicznego” najbardziej ucierpiały wskutek kryzysu. Dlatego pierwszą konsekwencją obecnego załamania gospodarczego będzie jak to ujmują „koniec fetyszu” kapitału zagranicznego. Innym rozwój polityki społecznej. Przykładem mogą być obecne wysiłki Chin na rzecz utworzenia nowoczesnego systemu emerytalnego ( interesująca praca tutaj ).

Autorzy przyznają jednak, że utworzenie dobrze funkcjonujących biurokracji to długi proces historyczny. I często brał swój początek w wydarzeniach niegospodarczych, jak wojna (w przypadku Prus) i wiązały się z budowaniem tożsamości narodowościowych.

Ta debata w Chinach ma jeszcze jeden wymiar. Na nowo odczytywany jest artykuł dr Zhao Xiao, który był doradcą ds gospodarczych premiera Chin „Market Economies With Churches and Market Economies Without Churches” (tłumaczenie). Przekonuje on iż chińska gospodarka potrzebuje elementu chrześcijańskiego. Podobnie, jak niegdyś Max Weber czy Alexis de Tocqueville, dr Zhao twierdzi iż wartości odgrywają fundamentalną rolę w budowaniu stabilnego systemu gospodarczego.

Then where does the greatest difference between the US and China ultimately lie? My personal opinion: churches. Only in this area is the difference between China and the US not a question of numbers, but rather an essential difference between presence and absence. In the US, the spires of churches are more numerous than China’s banks and rice shops.

Ultimately, why is it that we need a market economy? It is because the market economy has one major advantage: it discourages idleness. The planned economy is different — its faults are faults of having no system of encouragement. Good work and poor work are identical. Under a free market system lazy people cannot live. So the market economy will force competition; it is an efficient economic system. However, the market economy can only discourage idleness; it cannot discourage people from lying or causing harm. This brings to the market economy a certain danger; that is, it may result in an unsavory situation: it may entice people to be industrious in their lies, industrious in bringing harm to others, and to pursue wealth by any means. Some people may say that this is because the market economy is imperfect, and that a perfect market economy would not be this way. However, a market economy that relies solely on the individual will never be perfect, since it can only call people away from idleness but cannot discourage lies and injury.

The majority of followers go to church because they truly have a devout faith. Confucius said, “A true gentleman seeks out wealth according to the Way.” To the average person, this may be difficult to achieve since the average person is not a true gentleman. In comparison, it is people who turn their eyes to church spires who generally respect financial norms and integrity. Why? Here is the secret: Puritans, though they may be called the most fervent people in the world in their drive to accumulate wealth, nevertheless do not pursue wealth for personal benefit but rather “to the glory of God,” and to ensure that after they die they can enter heaven. This monetary ethic renders inseparable the motive and means of the Puritans’ pursuit of wealth, and those whose only thought is to create wealth for God will naturally be able to become true gentlemen — gentlemen among gentlemen.

Wiele wskazuje, że Chiny otwierają się nie tylko na nowe idee, ich gospodarka mimo pewnych trudności, jakie stanowi np inflacja, dość dynamicznie się rozwija.

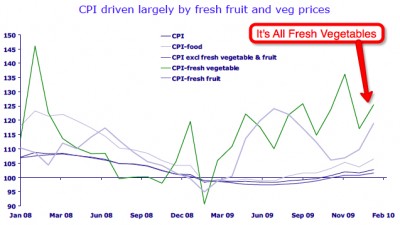

Dr John Rutledge, ekonomista, profesor Chińskiej Akademii Nauk, przekonuje iż problem inflacji Chin jest tymczasowy. (Choć George Soros stwierdził iż chińska gospodarka może spowolniać ze względu na inflację: „You now have /China/ inflation somewhat out of control, and causing some serious danger of wage-price inflation” źródło). Spowodowany jest przede wszystkim wysokimi cenami produktów żywnościowych, zwłaszcza świeżych owoców i warzyw. I jego zdaniem istotne jest by nie utożsamić tej sytuacji z ogólną kondycją gospodarczą. Tak było 2010 r. i ta sytuacja utrzymuje się także w tym roku, jak stwierdził w programie Larry Kudlowa w CNBC.

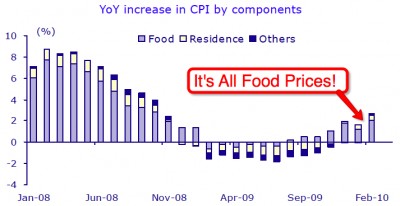

Food prices make up a much larger share of the CPI basket than they do in the U.S. or Europe. Food prices in February were +6.2% higher than a year earlier. Most of the increase was due to the 25.5% increase in fresh vegetable prices and +19% increase in fresh fruit prices, as shown in the chart below. Both were caused by severe weather and the New year holiday, which fell in February this year. Together, fruit and vegetable prices accounted for about one-third of the total CPI increase in February.

Rising incomes in China make the CPI increase negligible, as shown in the chart below. In fact, rising food prices drive higher income growth for China’s farmers. This is exactly the kind of relative price/wage pattern we expect in a country with fixed exchange rates and sharply rising productivity. Traded goods prices are constrained by global competition and rising productivity. But wages grow strongly to reflect rising output levels. It is important in this situation not to confuse rising wages with inflation when setting overall economic policy.

Tempo rozwoju gospodarczego jest w 2011 r. nieco słabsze, ale sytuacja jest stabilna. Według najnowszego raportu World Economic Outlook Międzynarodowego Funduszu Walutowego Chiny także nie wpadną w pułapkę w jakiej znajduje się Japonia od lat 90. I nie grozi im stagflacja. Ekonomiści wymieniają trzy powody. Wśród nich są m.in.:

Płynność gospodarstw domowych, firm i rządu jest niższa niż miało to miejsce w Japonii przed pryśnięciem bańki. Podobnie ryzyko nadmiernego zadłużania się jest mniejsze.

Chiny nie wprowadziły płynnego kursu wymiany, ograniczyły dopływ kapitału z zewnątrz jednocześnie budując silny zasób rezerw.

W konsekwencji ekonomiści IMF prognozują iż w 2016 r. Chiny będą dominującą gospodarką. A USA znajdzie się na drugiej pozycji.

According to IMF’s forecast based on „purchasing power parities”, China’s GDP will rise from $11.2 trillion in 2011 to $19 trillion in 2016, while the US’ economy will increase from $15.2 trillion to $18.8 trillion. Correspondingly, China’s share of the global economy will ascend from 14 percent to 18 percent, while the US’ share will descend to 17.7 percent.

Jednak część ekonomistów, wśród nich dr Arvin Subramanian, uważa iż Chiny są już największą gospodarką światową. Według prognoz opartych „purchasing power parities” zdaniem ekonomisty w lutym 2011 gospodarka Chin stanowiła 14,8 tryliona dolarów.

(…) two adjustments increase China’s GDP from the current estimate of $10.1 trillion to $14.8 trillion (an increase of 47 percent, of which 27 percent is due to the revision in the 2005 estimate, and the rest due to smaller-than-assumed increases in the cost of living between 2005 and 2010). This $14.8 trillion figure exceeds US GDP of $14.6 trillion. It must be emphasized, of course, that the difference is small enough to be within the margin of error.

Warto się zapoznać także z wpisem Cynicus Economicus na ten temat.

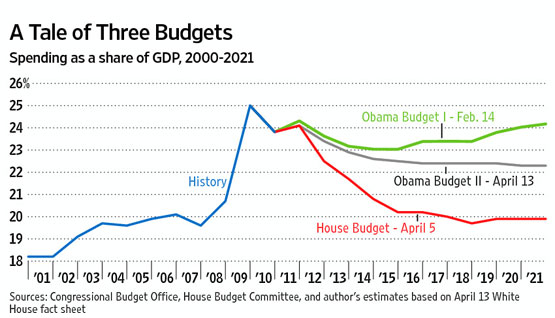

USA nie mogą domknąć budżetu. A zdaniem prof. Taylora powodem jest brak przejrzystości finansów w budżecie proponowanym przez Biały Dom. Jego zdaniem zawiera się w nim koncepcja walki z bezrobociem poprzez rozbudowę sektora publicznego. Przede wszystkim chodzi o zwiększenie wydatków na szereg instytucji rządowych.

When I show people this chart they ask why Washington is even having the debate. They say: If government agencies and programs functioned with 19% to 20% of GDP in 2007, why is it so hard for them to function with that percentage in 2021, when GDP will be substantially higher and with many opportunities for reforms and increased efficiencies? And if GDP and employment grow more quickly, as they would if private investment increased as a result of lower government spending and debt, then that 19% to 20% share of GDP could provide much more in the way of public goods.

Z prof. Taylorem debatuje prof. Paul Krugman.

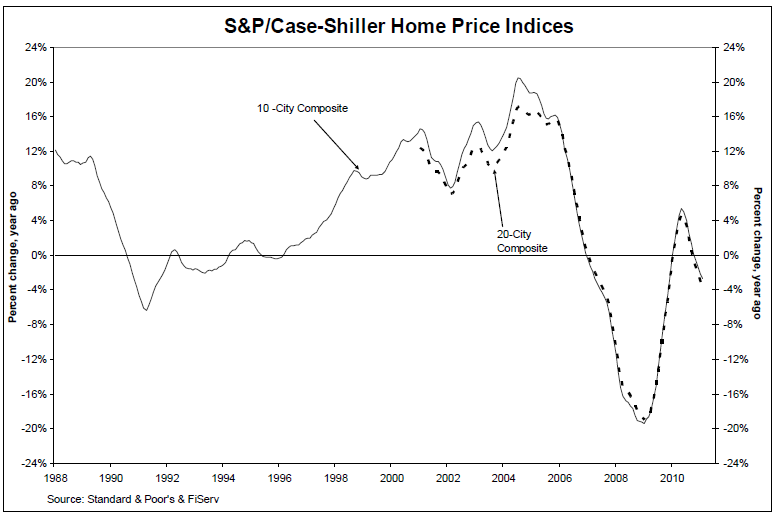

Professor Robert Schiller nie wyklucza iż przed gospodarką amerykańską drugie dno, przynajmniej jeśli chodzi o rynek nieruchomości.

Data through February 2011, released today by S&P Indices for its S&P/Case-Shiller1 Home Price Indices, the leading measure of U.S. home prices, show prices for the 10- and 20-city composites are lower than a year ago but still slightly above their April 2009 bottom.(…) Ten of the 11 cities that made new lows in January 2011 saw new lows again in February 2011. With an index level of 139.27, the 20-City Composite is virtually back to its April 2009 trough value (139.26); the 10-City Composite is 1.5% above its low.

Opracował Tomasz Pompowski

W styczniu 2020 roku Wielka Brytania formalnie opuściła Unię Europejską. Oczekiwane korzyści z brexitu, poza odzyskaniem suwerenności w zakresie kształtowania prawa i zewnętrznych relacji gospodarczych, jednak się nie zmaterializowały. Widoczny jest natomiast spadek wydajności i konkurencyjności brytyjskiej gospodarki, co wpływa także na kondycję rynku pracy.