Tak sugeruje jeden z dobrze poinformowanych ekonomistów-analityków Vitaliy Katsenelson. Chiny mogą nie dać rady pociągnąć boksującej Unii Europejskiej. Według prof. Paula DeGrauve i Marginal Revolution UE nie pomogła sobie zamieniając w przypadku Irlandii dług prywatny na publiczny. Eurostrefa jest słabsza - sugeruje raport Legatum Institute. A Pragmatic Capitalism uważa, że mimo wszystko Niemcy nie opuszczą unii walutowej.

Wygląda na to, że debata na temat euro przybiera kształt podobny do tej, która poprzedziła utworzenie wspólnej unii walutowej. Coraz więcej publikacji dotyczy kwestii fundamentalnych związanych z eurostrefą.

Legatum Institute opublikował raport pt. „Can the Euro survive?”, w którym sugeruje, iż kraje PIIGS mogłyby szybciej wydźwignąć się z kryzysu, gdyby wyszły z unii walutowej. W innym wypadku zapowiadane przez Unię oszczędności budżetowe spowodują długotrwałą recesję.

A second area where extraordinarily large imbalances have emerged in Europe’s periphery has been in the housing markets of Ireland and Spain. Fuelled by easy access to global credit, as well as by the ECB whose one-size-fits-all interest rate policy kept interest rates too low for too long for Europe’s periphery, Ireland and Spain experienced housing bubbles that make that experienced in the United States pale. (…) The bursting of the housing bubbles in Ireland and Spain has been a primary driver in the dramatic deterioration in their public finances. It has also been the primary factor in the rise in unemployment in Ireland and Spain to their present levels of around 13 percent and 20 percent respectively.

Autorzy raportu twierdzą, że finanse krajów peryferyjnych (Grecji, Hiszpanii, Portugalii i Irlandii) są niemożliwe do naprawienia. Nie pomogą zapowiadane poprawki do traktatu ani zaostrzenie polityki fiskalnej eurostrefy. Ponadto ratyfikacja traktatu wymaga czasu, którego brakuje w czasie obecnego kryzysu.

While the treaty modifications now being proposed would have had great merit when the Euro was launched in January 1999, how relevant they are today at a time when the periphery’s public finances have been compromised beyond repair and when there is every indication that the periphery’s crisis is deepening is questionable. While the periphery’s sovereign debt crisis is playing out in real time, past experience would suggest that treaty modification, which requires unanimous ratification by all European Union members, will take years to effect. In addition, it would appear that the proposed reforms overlook the fact that the major part of the periphery’s budget deficits is primary in nature.

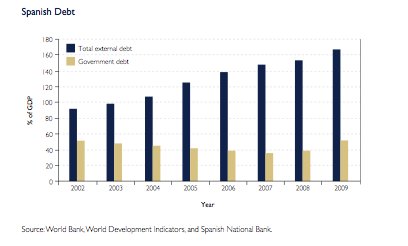

Nie pomoże też częściowa redukcja długu państw peryferii. W odróżnieniu od innych tego typu opracowań raport szczególnie zwraca uwagę na wpływ zadłużenia zewnętrznego. Wartość kredytów udzielonych deweloperom przez hiszpańskie (połączone nierozerwalnie z europejskim systemem bankowym) jest odpowiednikiem 45 proc. PKB tego kraju.

As such, even if the debt of the periphery were to be substantially written down, the periphery would still be left with very large budget deficits. And reducing these very large budget deficits to sustainable levels would still involve very deep recessions if such an exercise were attempted within the straitjacket of continued Euro membership.

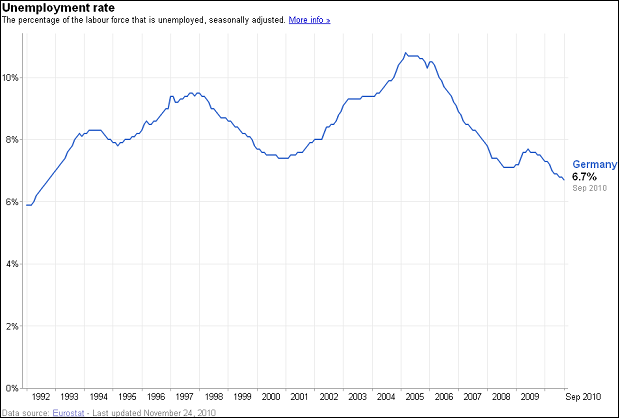

Mimo wszystkich problemów wbrew pogłoskom Niemcy raczej nie zechcą wycofać się z euro. Z wykresu można dowiedzieć się, że stopa bezrobocia w Niemczech wynosi około 6 proc. (i jest najniższa w Unii) i że wciąż spada.

Pragmatic Capitalism przekonuje, że to właśnie niemieckie banki (bezpośrednio lub pośrednio) są w dużej mierze wierzycielami długu państw peryferii.

Jednak coraz więcej ekonomistów pyta dlaczego w przypadku Irlandii Unia zdecydowała się zamienić prywatny dług na publiczny? Marginal Revolution cytuje prof. Paul DeGrauve ( z tekstu „A Mechanism of Self-Destruction of the Eurozone”), który uważa, że UE stała się, wskutek tej decyzji, bardziej podatna na kryzysy. Jego zdaniem to dług banków i gospodarstw domowych rósł niemal w sposób niekontrolowalny, a dług publiczny był utrzymywany na racjonalnym poziomie.

Surprisingly, the only sector that did not experience an increase in its debt level during that period was the government sector, which saw its debt decline from 72 to 68% of GDP. Ireland and Spain, two of the countries with the severest government debt problems today, experienced the strongest declines of their government debt ratios prior to the crisis. These are also the countries where the private debt accumulation was the strongest.

Interesującą myśl podsuwa jeden z czytelników w dyskusji pod postem.

European leaders probably recognized then that their banking system was overleveraged, and they may need to cut government programs (or raise taxes) to shoulder new private debt from the the private banking system.

In other words, they never believed, nor could you have rationally believed, that there was really a plan to for the Europeans to „austere” their way out of a recession.

All three have high net foreign liability positions, liabilities are highly concentrated through banks who are borrowing overseas, all three have experienced some form of housing boom and lift in consumption, and finally all three appeared to have a relatively strong fiscal position before the GFC before moving into fiscal deficits after the shock. And yet (so far) while the Irish and Greek economies and banking systems have collapsed, New Zealand’s has been fine.

Jednak Nowa Zelandia sprywatyzowała wszystkie banki, a jej stopy procentowe są płynne. I większość długu została zdenominowana w nowozelandzkim dolarze. (Na ten temat także Matt Nolan).

Jeden z dobrze poinformowanych ekonomistów-analityków na temat sytuacji gospodarczej Chin Vitaliy Katsenelson uważa, że wzrost gospodarczy Chin oparty jest na nietrwałych podstawach. Chiński rząd zarządza kapitałem tak by realizować krótkoterminowe cele. Katsenelson przytoczył przykład budowania osiedli mieszkalnych, z których nikt nie mieszka. Jedno z nich, Ordos, które do dziś stoi puste, dla 1,5 mln mieszkańców powstało w środkowej Mongolii.

The vacancy rate on commercial real estate in China is fairly high, but they still keep on building new office buildings because they think they will always grow. So therefore as long as they keep building, that activity will be registered as growth, until they stop. And when they do stop, they’ll drown in overcapacity, and they won’t be building new skyscrapers for a very long time.

Katsenelson nazywa China superbańką.

Dla tych ekonomistów, którzy nie ufają statystykom chińskim poleca inną metodę obserwacji gospodarki. Przylądanie się danym: zużycia elektryczności (spadła w czasie recesji), sprzedaży żywności w restauracjach fast-food, ilość towarów transportowanych koleją a także sprzedaży amerykańskich i europejskich firm w Chinach.

ChatGPT zapoczątkował nowy etap automatyzacji. W nadchodzących latach generatywna sztuczna inteligencja może doprowadzić do głębokich zmian na rynku pracy oraz znacząco przyspieszyć wzrost gospodarczy.

Droga energia, slowbalizacja, brak rąk do pracy, nadmierna biurokracja, wieloletnie zaniedbania inwestycyjne oraz opóźnienia technologiczne spętały potencjał rozwojowy Niemiec. Gospodarka przechodzi przez polikryzys– spowodowany wieloma czynnikami – na który nie ma prostej odpowiedzi w postaci np. pakietu koniunkturalnego lub jednej, porządnej reformy. RFN potrzebuje w istocie polireformy – dziesiątków drobnych korekt, które jednak jako całość określą na nowo równowagę między rynkiem a państwem.

Ceny konsumpcyjne rosły w Stanach Zjednoczonych w tempie 3,5 proc., co stawia pod dużym znakiem zapytania perspektywę cięcia stóp procentowych za Oceanem. Odczyt inflacji CPI za marzec 2024 r. w USA był nieznacznie wyższy od rynkowego konsensusu i postawił Komitet Otwartego Rynku w niełatwym położeniu.

Oczekiwaniom inflacyjnym gospodarstw domowych zazwyczaj nie poświęca się zbytniej uwagi przy monitorowaniu i prognozowaniu inflacji, częściowo dlatego, że wykazano, iż mediana ich oczekiwań ma mniejszą moc predykcyjną niż oczekiwania innych podmiotów. Niniejszy artykuł ma na celu dowieść, że zmiany w rozkładzie oczekiwań inflacyjnych gospodarstw domowych są istotne dla prognozowania inflacji w najbliższym czasie i oferują dodatkowe informacje w porównaniu z miernikami rynkowymi i oczekiwaniami prognostów. Sugeruje to, że oczekiwania inflacyjne gospodarstw domowych powinny odgrywać większą rolę w monitorowaniu inflacji, a w konsekwencji w kształtowaniu polityki pieniężnej.

W niedawnych badaniach zasugerowano, że wynagrodzenia poniżej prawnie ustalonej płacy minimalnej są zaskakująco powszechnym zjawiskiem. W niniejszym artykule omówiono tzw. „kradzież płac” w Stanach Zjednoczonych oraz jej wpływ na wzrost wynagrodzeń, który mógłby być udziałem pracowników.

Najnowsze wydanie „Obserwatora Finansowego” ukazuje nam wizje przyszłości bliskiej i dalekiej. W tym numerze, najlepsi eksperci postarają się odpowiedzieć na kilka kluczowych pytań, dotyczących sztucznej inteligencji i tego jak generatywna AI wpłynie na bankowość, edukację oraz inne dziedziny naszego życia.

Nieefektywność nadzoru prowadzi do występowania nieprawidłowości i nadużyć na rynku funduszy inwestycyjnych w Polsce – taką sensacyjną tezę stawiają autorzy monografii „Nieprawidłowości i nadużycia na rynku funduszy inwestycyjnych”.

Budowa Centralnego Portu Komunikacyjnego wzmocniłaby znacznie pozycję Polski w europejskiej gospodarce – stwierdził w rozmowie z „Obserwatorem Finansowym" dr Andreas Wittmer, dyrektor zarządzający Centrum Badań Lotniczych na Uniwersytecie w St. Gallen.

Sztuczna inteligencja powoli zmienia sposób działania banków i instytucji finansowych. Pomaga im zredukować ciężar biurokracji, ale także podejmować szybsze decyzje oraz utrzymywać efektywny kontakt z klientami. A będzie jeszcze lepiej. W perspektywie czeka kilkunastoprocentowy wzrost EBITDA.

Dywersyfikacja metod płatności, rozumiana jako poszerzanie dostępnej ich gamy, zwiększa wybór płatników i odbiorców płatności, stymuluje konkurencję na rynku i innowacyjność dostawców usług płatniczych, redukuje ryzyko, ponieważ uniezależnia rynek płatności od jednego, potencjalnie dominującego systemu płatności. Podobnie ma się sprawa z formami pieniądza, które się uzupełniają a jednocześnie konkurują i substytuują wzajemnie.

Współczesne problemy prawne Unii Europejskiej, sztuczna inteligencja w bankowości oraz polityka pieniężna były tematami grudniowego zjazdu na podyplomowych studiach MBA organizowanych w ramach drugiej edycji projektu „Akademia NBP”.

Portal ekonomiczny NBP „Obserwator Finansowy” ponownie znalazł się w czołówce najbardziej opiniotwórczych mediów w kategorii „Media ekonomiczne i biznesowe”, wyprzedzając m.in. „Parkiet”. Wzrost cytowalności treści publikowanych na łamach serwisu wzrósł w kwietniu w odniesieniu do marca 2023 r. o 37 proc.

Sytuacja gospodarcza w Polsce na tle innych krajów przedstawia się korzystnie. Warto zauważyć, że w szybkim tempie nadrabiamy dystans dzielący Polskę od poziomu życia w wybranych państwach europejskich. W ciągu ostatnich czterech lat dynamika wzrostu PKB plasowała Polskę powyżej innych krajów europejskich, zarówno strefy euro, w tym Niemiec i Francji, jak i krajów Unii Europejskiej z własną walutą, np. Czech.

Większość polskich przedsiębiorców odczuła skutki wojny w Ukrainie, choć jej wpływ oceniają w zróżnicowany sposób – wynika z badania przeprowadzonego przez Polski Instytut Ekonomiczny.

W styczniu 2020 roku Wielka Brytania formalnie opuściła Unię Europejską. Oczekiwane korzyści z brexitu, poza odzyskaniem suwerenności w zakresie kształtowania prawa i zewnętrznych relacji gospodarczych, jednak się nie zmaterializowały. Widoczny jest natomiast spadek wydajności i konkurencyjności brytyjskiej gospodarki, co wpływa także na kondycję rynku pracy.