Tydzień w gospodarce

Category: RaportyPrzegląd wydarzeń gospodarczych ubiegłego tygodnia (16–20.05.2022) – źródło: dignitynews.eu

PZU has been declaring its appetite to purchase banks since 2015. The high level of equity and investment funds of the largest state-controlled insurer in the Central and Southeast Europe allowed it to make such plans. Moreover, successive governments, unable to obtain domestic capital from other sources, encouraged the company to pursue the repolonization of banks.

In the middle of 2015, PZU spent PLN1.6bn on the purchase of 25.25 per cent of shares in Alior Bank, founded less than a decade earlier by private owners as a start-up. The insurance company paid PLN89.25 per share, or 1.95 times the book value. Alior Bank, which was already a large institution with assets exceeding PLN30bn, was supposed to become a vehicle to consolidate a banking group.

Following the global crisis, every few years another parent company of a Polish bank was forced to sell its assets in order to save itself. This created an opportunity to purchase another bank. Alior Bank had already exhibited an appetite for acquisitions by purchasing Meritum Bank, which was small but had a highly developed network of branches, for PLN325.5m in early 2015.

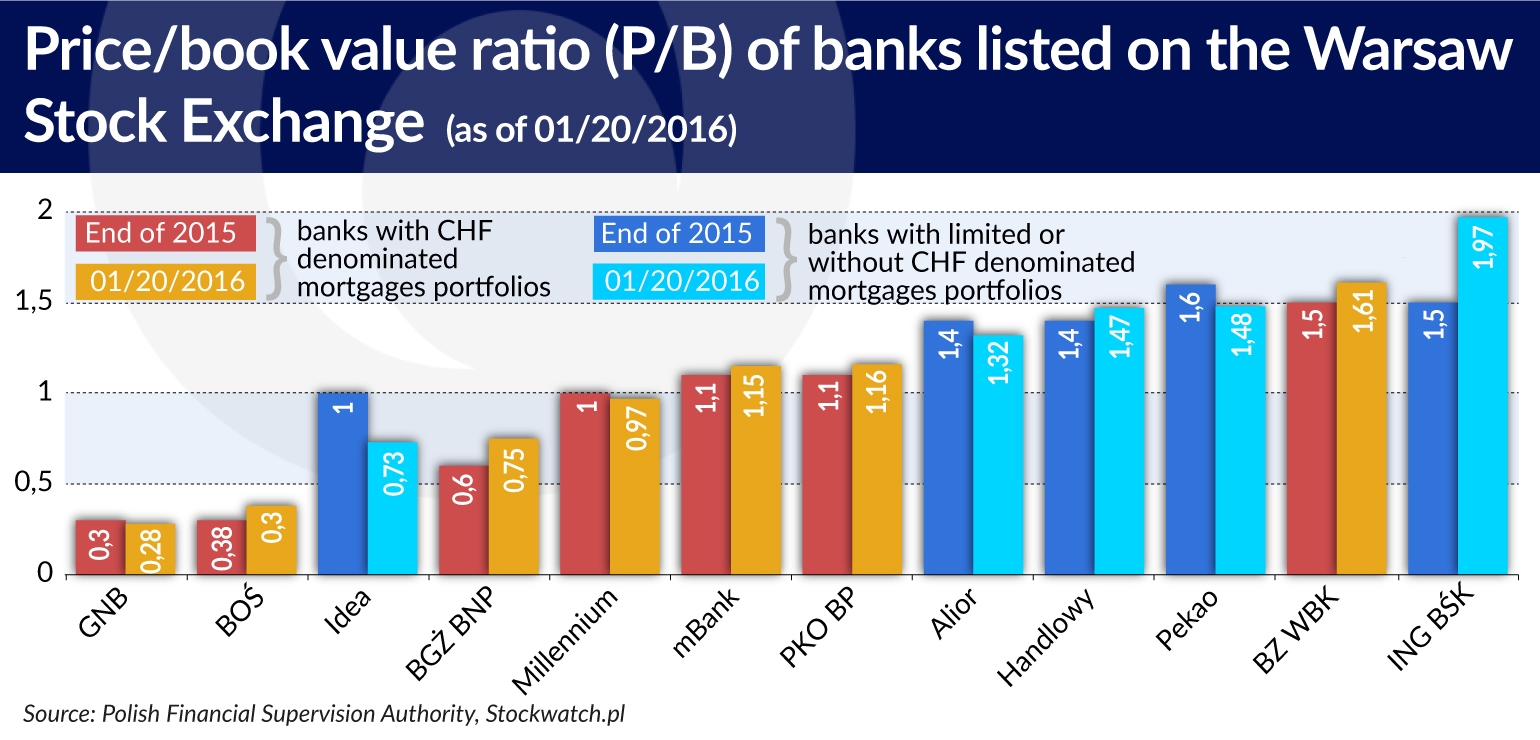

Two decisions which would prove important for the Polish market were made almost at the same time in 2015. The global giant General Electric decided to withdraw from banking and focus on its core business. This meant that Bank BPH, belonging to GE Capital Group, would sooner or later be put up for sale. We should add that this bank was in a poor condition, was implementing a recovery program, and had one of the highest proportion of CHF denominated mortgages in its balance sheet out of all the Polish credit institutions.

A few months earlier, the Austrian Raiffeisen Zentralbank decided that its subsidiary company, Raiffeisen Bank International (RBI), would sell its operations in Ukraine, Hungary, Slovenia and Poland, as the parent company needed capital. It announced the sale of its Polish company for EUR1bn, that is, at book value. The market immediately decided that this valuation was too high, considering the portfolio of CHF denominated mortgages. The discussion about a conversion of the CHF denominated mortgages into the PLN denominated ones was already gaining steam, and banks were regularly estimating how many billions they would lose on such an operation.

Raiffeisen owed its CHF denominated mortgages portfolio, with its low quality, mainly to the Polish subsidiary of the Greek Eurobank Ergasias, Polbank EFG, , which Raiffeisen acquired in 2012. The Greek institution, which was actually owned by funds from Switzerland and Luxembourg, launched its activities in Poland in 2006. Like all banks that entered the Polish market too late, it began with aggressive expansion, mainly through the sale of CHF denominated mortgages to customers more risky than those who were granted loans by institutions better established in Poland. The mortgages were mainly financed by the inflow of foreign funds, since Polbank EFG could not keep up with the creation of a deposit base.

When the Greek parent-bank was rescued from bankruptcy in 2012 with public funds, a decision was made to separate its foreign operations. At the end of 2011, Polbank was the sixth institution in Poland in terms of value of extended loans. It granted loans for a total amount of EUR5.23bn and serviced more than 660,000 clients.

Raiffeisen bought Polbank for EUR460m. It’s hard to say what the intention and insight into the situation were, but from today’s perspective we can see that Polbank, deprived of funding, was in a critical situation. Some bankers still claim that if not for the offer of Raiffeisen, Poland would have had to spend over a dozen of billions of public funds on the payment of guaranteed deposits.

Alior – supported by PZU’s strong equity and the guarantee of success in the offering of new shares – started its acquisitions with BPH. It ultimately bought 87.23 per cent of BPH shares in April 2016 for the amount of PLN1.23bn, that is, paying 0.93 times the book value. Alior took over the banking operations without the foreign exchange and PLN mortgages. These will be further managed by a separate institution which will most likely generate losses.

The combined assets of Alior and BPH amount to PLN62bn, which gave it the ninth place in the Polish banking sector. The strategic goal of the bank was to become one of the 5 or 6 largest lenders in Poland. In order to do this, Alior would have to grow by at least another PLN10bn.

It seemed that after selling the leasing company to PKO BP, Raiffeisen would also sell its Polish bank to Alior. Meanwhile an opportunity suddenly presented itself for PZU to purchase a controlling stake in Pekao from UniCredit, which still held 40 per cent of its shares and was intensely looking for capital. The transaction with the participation of the Polish Development Fund was finalized in December 2016 – the Polish institutions ultimately paid PLN10.6bn for a 32.8 per cent stake in Pekao, that is 1.3 times the book value. This was a reasonable price for a bank with such great potential. In addition, PZU OFE already held 2 per cent of shares in Pekao.

In this way PZU now has strategic packages in two banks and one problem. It will not be able to combine them. And only the merger of Alior and Pekao could create a new quality on the Polish market – it would accelerate further mergers and acquisitions and open the opportunity for further steps in the repolonization of the banks.

Grzegorz Cimochowski, a partner at Deloitte, who has prepared reports on the banking sector in CSE for the past several years, believes that the merger of Alior and Pekao could accelerate decision-making processes at the headquarters of foreign owners on whether it is worth staying in Poland.

“It could take two years before the effects of synergy would kick in and the new entity would start to compete on the market. Then we would not only have an awareness that a large entity can compete, but also the effects. It would be clear that it’s difficult to compete with such an entity,” he told the CE Financial Observer.

Alior and Pekao are two entirely different banking cultures. The former has been using the latest technology since its creation, with its business model resembling that of a fintech company (as the CEO Wojciech Sobieraj likes to call his bank) or a loan company, as it flawlessly entered the consumer finance market, achieving a net interest margin (NIM) at the level of 450 basis points. The price for that is the cost of risk reaching 230 bps.

Pekao, in turn, is the largest bank servicing corporations, with a conservative approach to credit risk, with low risk costs of 48 bps in the third quarter of 2016, reserves coverage at 74.3 per cent and a relatively low net interest margin – 280 bp. It began to pursue the digital agenda relatively recently, although it has achieved undeniable success in this field, such as the introduction of card payment in the Biedronka discount chains. In addition it has approx. PLN7.9bn in surplus capital, which gives a huge potential for organic growth or acquisitions.

A bank created from the merger of Pekao and Alior would have PLN225bn in assets, and would get closer to PKO BP (the largest bank in Poland), leaving other institutions far behind. The State Treasury could then directly or indirectly control two banks – PKO and the newly formed entity.

This could have happened if Pekao acquired Alior, but PZU will probably not be able to achieve a majority in the Pekao Supervisory Board and have sufficient influence on the decisions of the bank with its current stake. If it increased its holdings and exceeded 33 per cent, it would have to announce a call for shares to reach a stake of 66 per cent. However, it doesn’t have enough funds for that.

The question arises as to why PZU purchased Pekao in the first place. Although after this transaction Polish capital exceeded a 50 per cent share in the assets of the Polish banking sector, the sector hasn’t changed much in terms of structure.

Meanwhile PZU, as the owner of large blocks of shares of two banks, finds itself in a vulnerable position. The challenge will be to communicate with the market in such a way as to fend off any suspicion that the insurance institution could engage in arbitrage.

The preferred instrument for the consolidation of a banking group should probably be Alior – in line with earlier plans – and it should acquire banks of its own size. The opportunity to buy Pekao appeared quite suddenly, the pace of negotiations was very quick and perhaps because of that there was no time to find a way to structure the transaction and to fulfil all corporate procedures so that ultimately Pekao could be purchased by Alior.

When the opportunity arose to buy shares in Pekao, Alior was involved in negotiations for the acquisition of Raiffeisen Polbank. The business daily “Puls Biznesu” wrote that Raiffeisen had already notified the Polish Financial Supervision Authority that negotiations were concluded, but Alior ultimately withdrew from the deal. The stated reason was that PZU did not want to carry out two transactions simultaneously.

Market sources claim that the deal was supposed to be similar to the case of BPH – the CHF denominated mortgages would be excluded from it. We don’t know what price the parties reached in the negotiations, but Raiffeisen had declared previously that it wanted to sell the Polish company for no less than the value of equity. That was not a tempting offer.

A little earlier, before the first preparations of banking groups to exit the Polish market, we saw the beginning of a discussion on the conversion of CHF denominated mortgages into PLN ones. A similar operation was carried out a few years earlier in Hungary, which plunged the local banking sector into long-term lack of profitability. These discussions are still going on, despite the calculations of Poland’s central bank NBP and the Polish Financial Supervision Authority. According to the supervision authority, depending on the variant, the losses of the sector would amount to PLN56.2-66.9bn, not including the cost of payment of guaranteed deposits from several banks that would go bankrupt.

The discussions on the issue of CHF denominated mortgages that have gone on for several years and generated increasingly radical proposals caused a spectacular drop in the valuations of Polish banks. In January, the Financial Stability Committee determined that the portfolio of foreign currency mortgages does not create systemic risk in itself, but generates such risk “in the context of the potential consequences of the invasive legal solutions proposed in the public debate”. This is an important signal that solutions undermining the stability of the Polish banking system should not be adopted.

Right now everyone – the management boards of banks, the shareholders, the owners – is wondering what solutions will be adopted. At the same time, the profitability of the Polish banking sector dropped to 8.6 per cent ROE at the end of the third quarter of 2016 and is getting closer to the average for the region of CSE, although it still remains much higher than in the euro area.

“Central Europe has caught up with us, and we have made a step backwards,” says Grzegorz Cimochowski commenting the results of the last Deloitte report.

It is rather certain that the owners of the banks involved in CHF denominated mortgages will not be able to count on dividends over the next few years. While until now – including the recent transactions of UniCredit or the plans of Raiffeisen – parent-banks have been selling banks in Poland in order to save themselves, the current decisions may have different motivations. They will be more strongly associated with strategies and an assessment of the prospects for the Polish market. It is possible that these assessments will prove to be much weaker than 2-3 years ago.

The additional capital buffers introduced so far by the supervision authorities in order to cover the risk of CHF denominated mortgages mean that the capital ratios of some institutions have reached 20 per cent. The requirements will be even higher, because the Financial Stability Committee is now recommending an increase of risk weights for foreign currency mortgages from the current level of 100 per cent to 150 per cent.

According to the recommendation of the Financial Stability Committee, the Supervisory Review and Evaluation Process (SREP) is supposed to account to a greater extent for the full range of risks associated with foreign currency mortgages, and the Loss Given Default (LGD) parameter, specifying the proportion of exposure that may be lost in the event of default by the borrower, is to be increased. All of this will increase the security of the system, but will reduce the return on equity. This position, however, has eliminated concerns about the fulfilment of the worst possible scenarios.

Who could leave the Polish market? In general, out of the foreign groups only Santander (BZ WBK), Commerzbank (mBank) and ING (ING BŚK) seem to have a safe position. Virtually, all the remaining entities could exit the market. The reasons could range from the group’s strategy to the lack of profitability of the Polish investment, or the cost of increasing the capital of the Polish company. And discussions on this topic are already taking place in the banking circles.

For now this is merely talk, because real valuations and discussions regarding prices will be possible in two or three years, when the effects of regulations relating to CHF denominated mortgages will not only enter into force, but also bring results. During this time it is difficult to expect any transactions caused by reasons other than the ones that have applied thus far.

Who could be on the side of the buyers? Probably not the banks. It is possible that in two or three years investment funds from various parts of the world will start playing a major role in the consolidation of the Polish sector, provided that they determine it to be sufficiently attractive. And discussions with such owners will be much more difficult for the supervision authorities than with the current parent-banks.

“Banks are now purchased by non-banking entities, and especially funds. They buy banks much more frequently than other banks do,” says Grzegorz Cimochowski.

Meanwhile, the potential for acquisitions by Polish companies controlled by the State Treasury has been significantly exhausted, as evidenced by the breakdown of talks between Alior and Raiffeisen. In the case of large transactions we can only count on Pekao.

The refund of currency exchange rate spreads to the Swiss franc borrowers and additional capital requirements will affect two banks the most. These are Bank Ochrony Środowiska (BOŚ) and Getin Noble (GNB), which are both owned by the Polish capital. The market was surprised by the fact that in mid-2016 GNB was able to meet the capital requirements along with the additional capital requirements of the Polish Financial Supervision Authority. BOŚ had to perform an emergency share issue, and it succeeded thanks to the Polish Development Fund, which obtained a 9.6 per cent stake in the increased capital. In December 2016, GNB was already valued at less than PLN1bn. It is possible that Pekao will have to invest some of its surplus capital in this venture. Not for business reasons, but pro bono publico.