In the last quarter of 2016, the government eventually removed the difficulties in absorption of the EU funds under the financial framework 2014-2020, experienced for the entire previous year, and this contributed to the extended use of those funds. According to the Ministry of Development, the delays in using the funds in the majority of operational programs amounted to a year, and in the case of railway investment – even to two years.

The problems with releasing the EU funds resulted among others from the European Commission’s requirement to implement EU directives and the necessity to verify and update the sectoral investment plans. Adoption of plans harmonized with the EU legislation was the condition of releasing the payments under the new financial framework. Failure to adopt these regulations on time made it impossible to disburse the EU funds and thus contributed to a clear slowdown of public investment.

As a consequence of the government tackling the issues hindering the absorption of the EU funds, the use of those funds grew in Q4’16. The data concerning requests for payments under the EU framework 2014-2020 show that the EU funds involved in the co-financing of investment projects in the last three months of 2016 were doubled (EUR3.7bn at the end of the year as compared to EUR1.9bn at the end of September).

In 2017 this trend will continue, and as a consequence a considerable revival of public investment and increased capital expenditure in enterprises controlled by the public sector, which will be induced by the growing use of the EU funds.

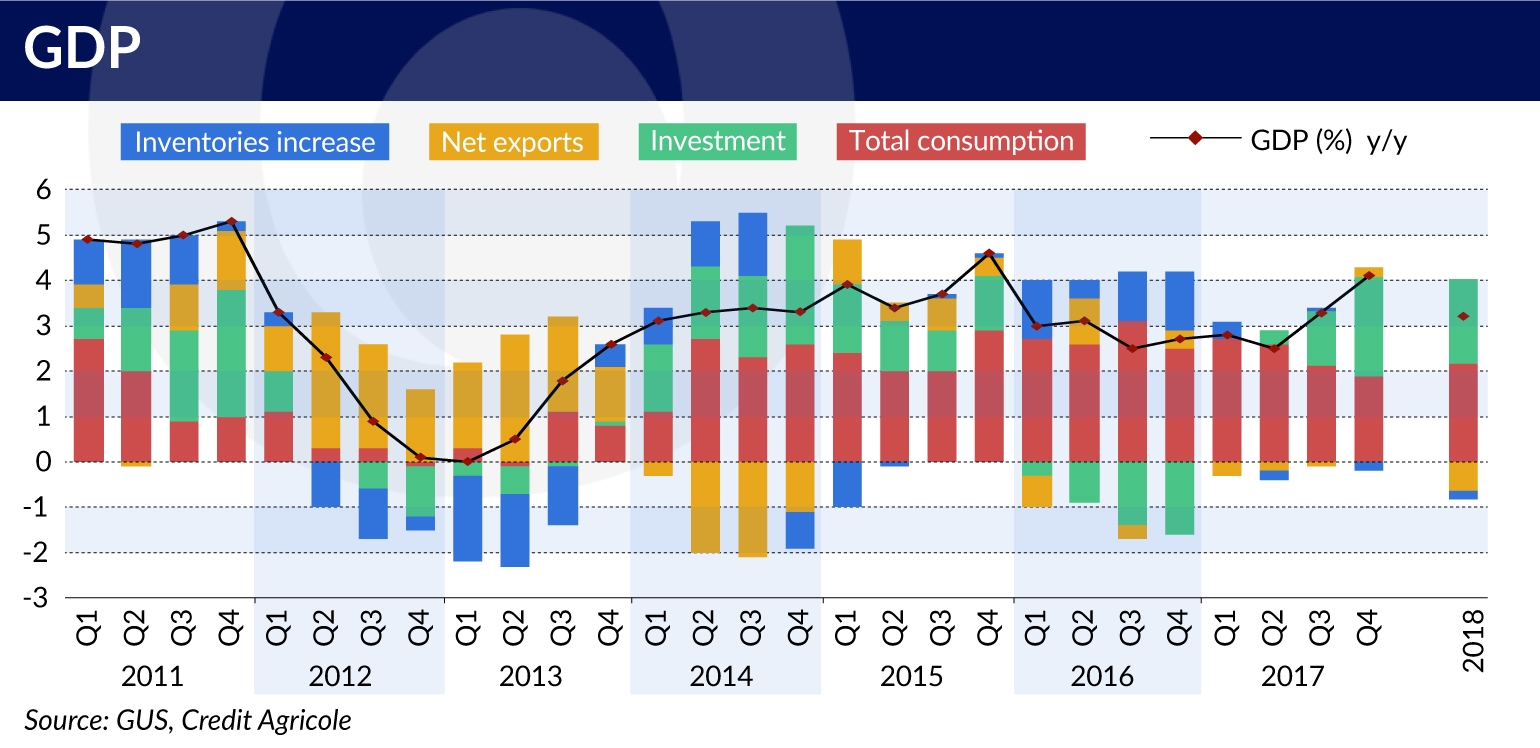

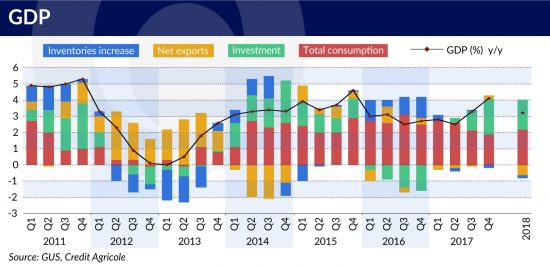

Poland is forecasting the total investment growth rate to increase to 5.3 per cent year to year as compared to -5.5 per cent in 2016, and as a result, the annual economic growth to accelerate to a considerable extent and exceed 4 per cent in Q4’16.

There is a corroboration in the data on construction and assembly output for which the growth saw a positive value for the first time since November 2015.

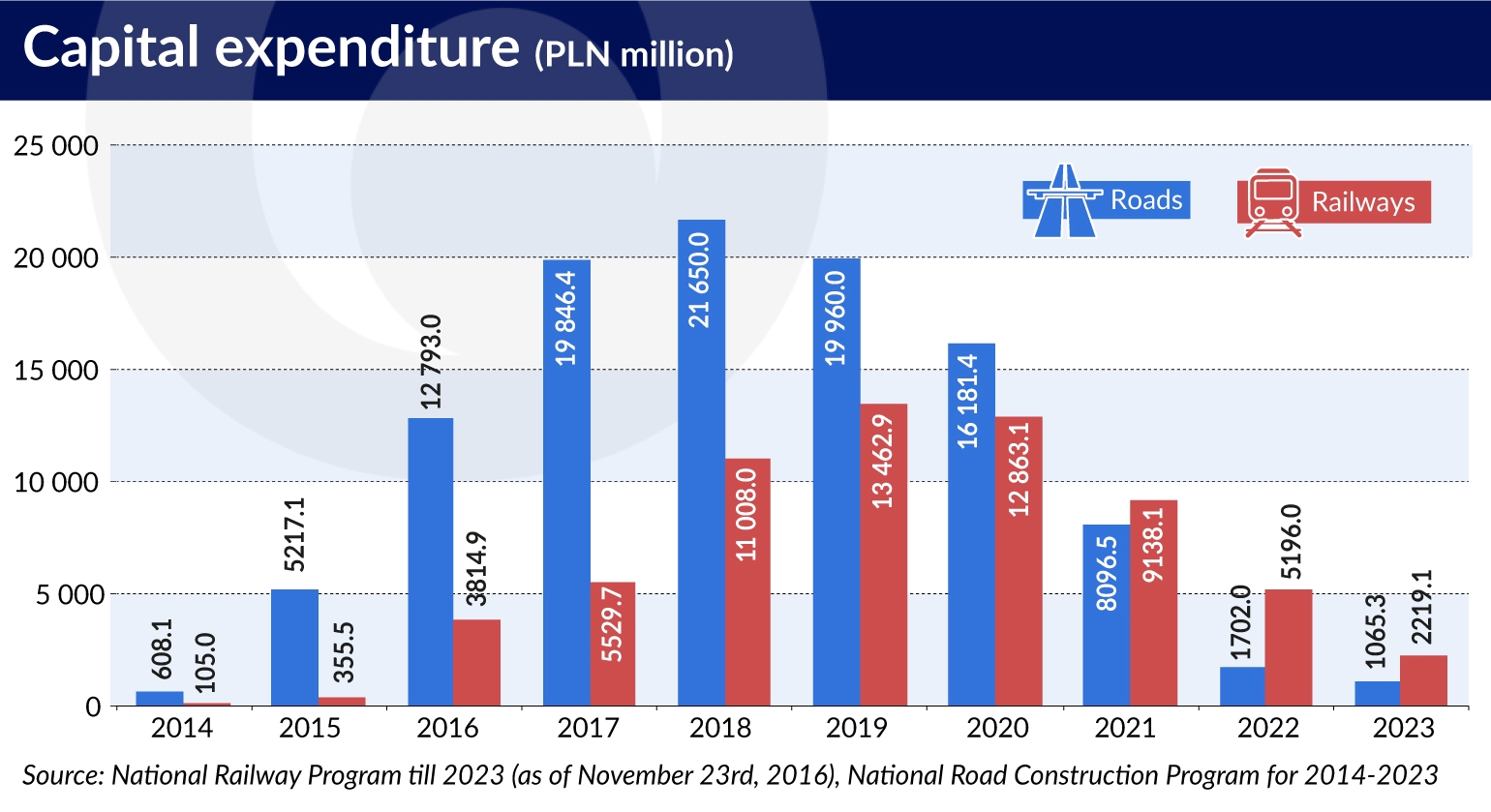

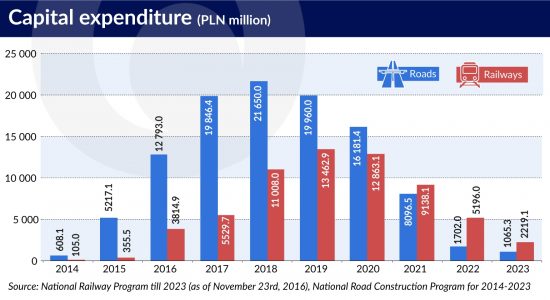

A substantial part of public outlays will be taken up by investment involving the construction of civil engineering structures, particularly road, railway and utility infrastructure (e.g. energy). The investment plans in those sectors are concisely presented in two documents: National Road Construction Program (NRCP) for 2014-2023 and National Railway Program (NRP) to 2023.

A large-scale review of energy investment projects up to 2030 published by the Ministry of the Treasury envisages the implementation of projects worth several billion euros within the upcoming years. The NRP and NRCP suggest an approx. 50 per cent growth of outlays for investment in road and railway engineering in 2017 as compared to 2016.

In the face of the fact that the NRP was adopted in November 2016, and the NRCP in September 2015 and its update is now in progress, the schedules proposed in both documents probably significantly differ from the current investment plans. Nevertheless, the public investment in 2017 will see a huge speedup, especially in the context of the low-base effects from the year before caused by the hindered absorption of the EU funds.

This is confirmed by the statement of the Minister of Construction and Infrastructure, Andrzej Adamczyk, summing up the government’s investment plans. For railway, investment projects for EUR1.7bn were in progress at the end of January, whereas in the case of road investment, approx. 125 km of express roads and motorways for EUR1.3bn were put into use in 2016, and the construction of 393 km of roads worth EUR3.5bn is planned for 2017. Adamczyk emphasized that as for now investment for more than EUR11.8bn was in progress under the new EU framework.

The acceleration of public investment and growth of capital expenditure expected in the public sector-controlled enterprises should contribute to the growth of production and investment activity in the private sector. There are two channels of impact: demand-side effect and the so-called crowding-in effect.

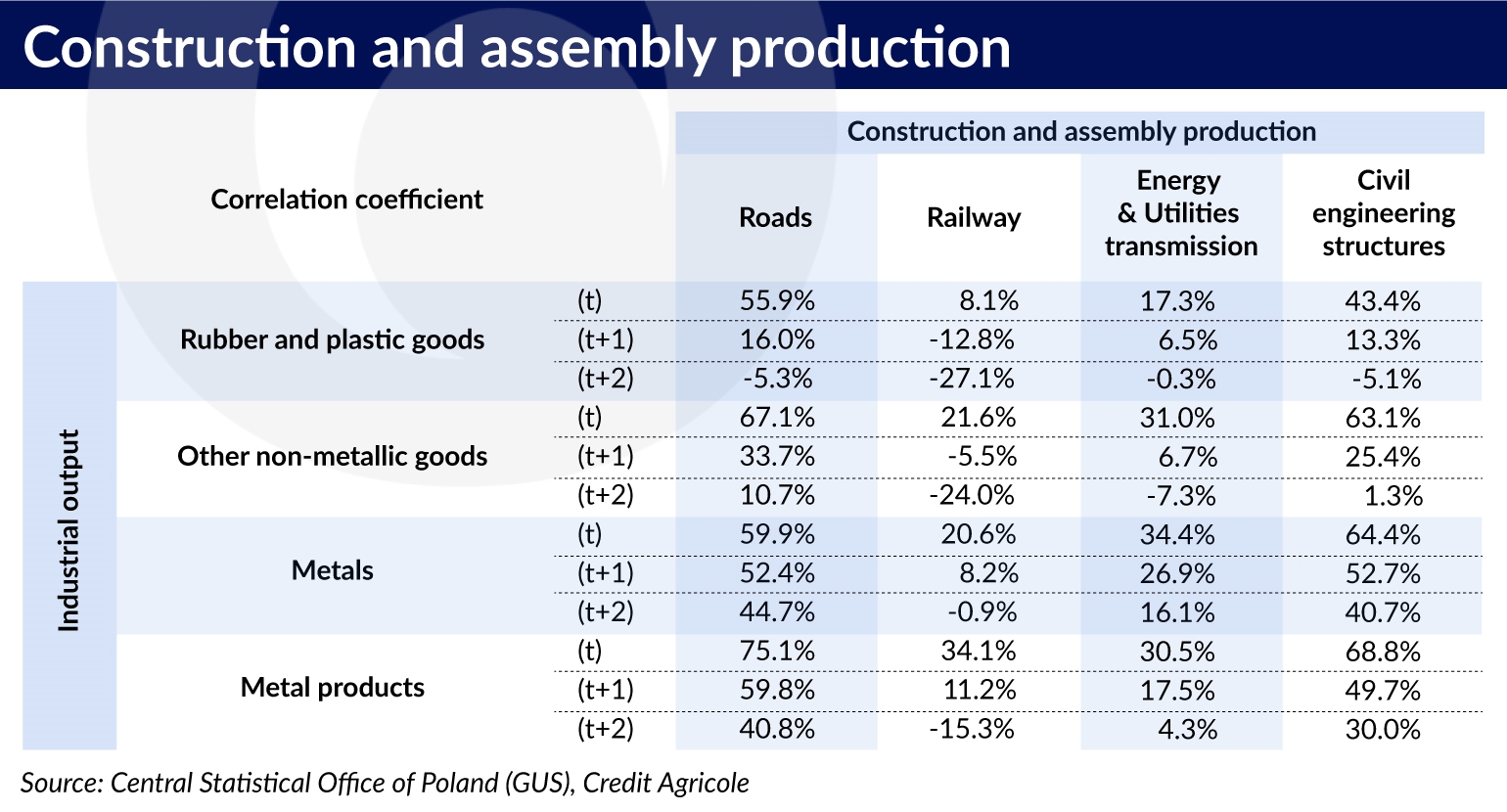

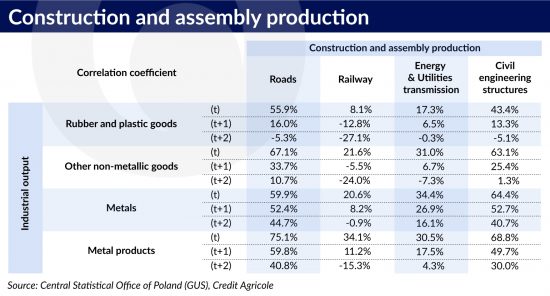

The demand-side effect will materialize as follows: higher public capital expenditure determines higher output in private companies related to the cycle in public investment. To analyze which industry branches will see the highest output growth, we have examined the historical correlation between construction and assembly output in the category “civil engineering structures” and the production activity of particular industry branches. Of particular interest was the influence of output related to construction works in railway, road construction and utility supply.

We have examined the relations with industrial output occurring simultaneously and with a delay of one or two quarters. The results of analysis show that the output grows mostly in branches involved in the supply of raw materials and materials used in construction projects.

These are primarily: production of metals (e.g. metal semi-finished goods, metallurgic articles, pipes, bars) and manufacture of metal goods (e.g. metal structures, metal tools, wires, conduits, screws, nails), manufacture of other non-metallic mineral goods (e.g. asphalt, cement, plaster stone, glass fibre, ceramic goods) and manufacture of rubber and plastic goods (e.g. semi-finished goods made of plastic, containers, artificial stones).

The scale of correlation varies in the case of selected segments of infrastructure investment (roads, railway, utility supply), whereby the highest correlation may be observed in road investment projects.

According to the results of the GUS business tendency survey of enterprises, the above branches are currently characterized by high involvement of production capacity: it is as much as 80 per cent. In the context of the sustained high level of production capacity utilization, increased demand from the public sector will determine increased capital expenditure of companies.

Investment will also grow in companies of other industry sectors – with lower dependence on the cycle in public investment – because the utilization of production capacity is at a very high level in the case of nearly all sectors. The utilization of production capacity in manufacturing at a level higher than the current one could be observed only in the period of Q1-3 2008, i.e. the period of overheating of the economy.

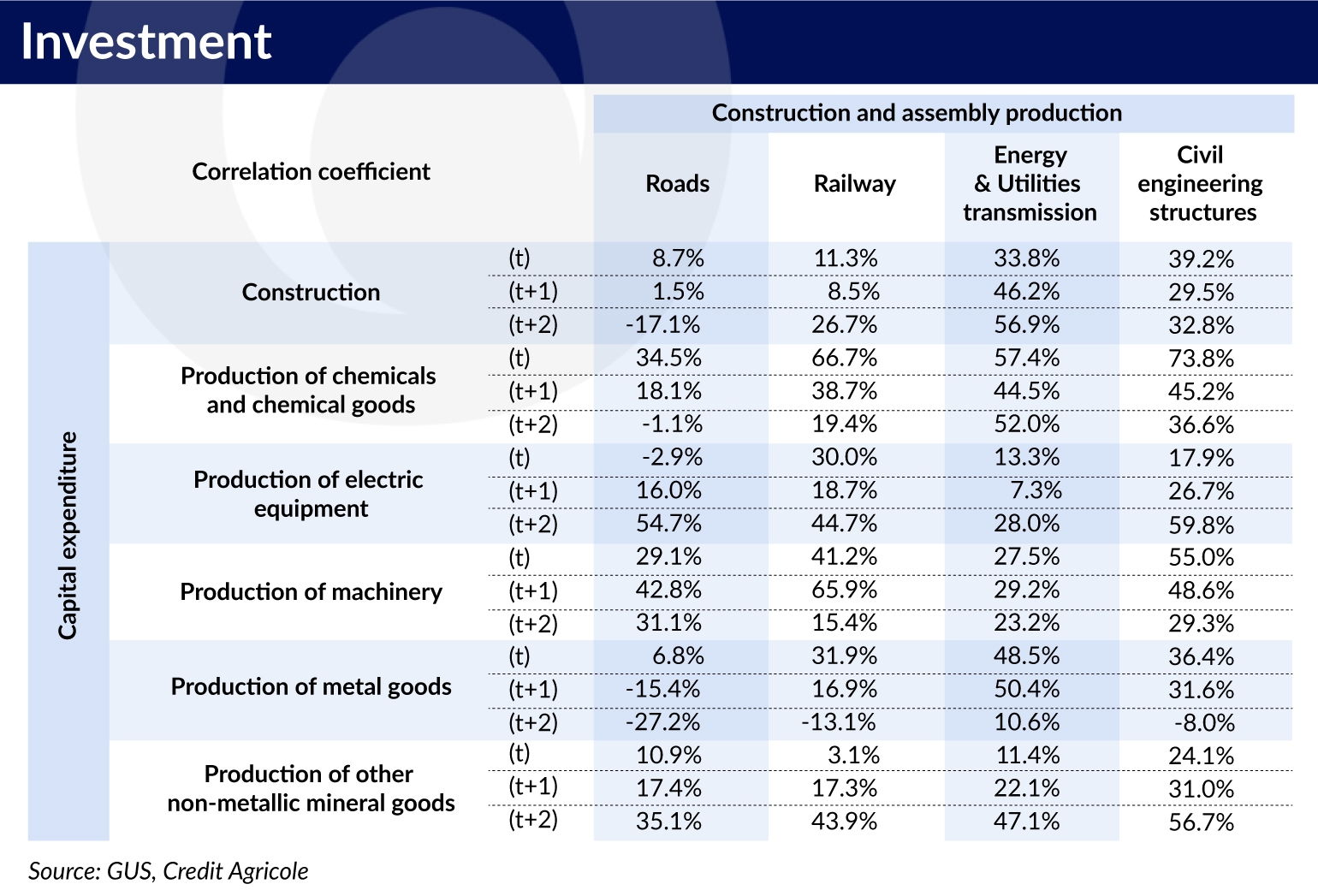

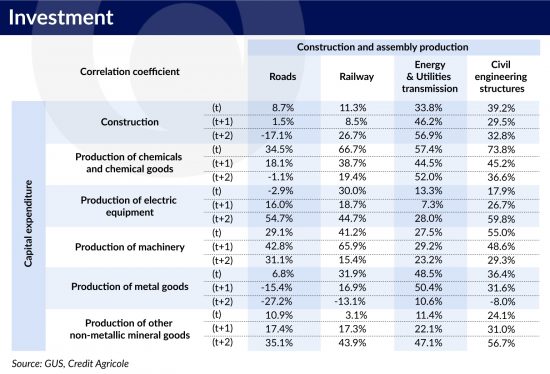

In order to analyze in which branches investment will grow the most, we have analyzed the correlations again, this time between the production and assembly output in the category “civil engineering structures” and investment of companies with at least 50 employees in various sectors of industry, services, and construction.

As expected, these are categories directly or indirectly related to the service of construction projects, and primarily: construction, manufacture of machinery and equipment (e.g. tools, industrial devices), manufacture of electric equipment (e.g. cables, lighting), chemical industry (e.g. paints, varnishes, adhesives), and the abovementioned manufacture of metallic and other non-metallic mineral goods.

In 2017, the pick-up of investment in companies associated with the increased capital expenditure of the public sector will be mostly visible in the abovementioned branches; however, it will not be limited to those categories. This will be the result of the second aforesaid channel of impact: the crowding-in effect.

A traditional approach in the literature on the subject is the assumption that higher public capital expenditure contributes to crowding out private investment. While contributing to the growth of domestic demand, it affects the growth of interest rates, and thus the growth of the cost of capital, which restrains private investment. On the other hand, other research shows that this correlation occurs mainly in developed economies.

In the case of developing economies, increased public investment results, by operation of the crowding-in effect, in a rise in private investment. This is because in the emerging economies public investment is complimentary to the investment activity of the private sector. Higher investment of public funds increases the availability of (poor at first) infrastructure for enterprises, which increases the rate of return on private investment and affects its better growth. Thus, the crowding-in effect prevails over the crowding-out effect.

In recent years, Poland has seen a positive correlation between the growth of public capital expenditure and the growth rate of private investment. A temporary impairment of the correlation occurred in the period of preparations to the organization of EURO 2012. This is why the crowding-in effect is reflected also in Poland.

The available literature on the subject shows that the crowding-in effect stimulates private investment mainly when the public sector implements projects involving the development of transport and communications infrastructure. This is a situation we are going to observe this year in Poland. The raised growth rate of investment carried out by the public sector and companies controlled by the public sector units will thus determine the intensified investment activity of companies this year.

Taking into consideration the said mechanism, we forecast the total growth of investment to increase to 5.3 per cent year to year in 2017 as compared to -5.5 per cent in 2016, and as a consequence, the economic growth rate in annual terms to considerably accelerate this year and exceed 4.0 per cent in Q4.

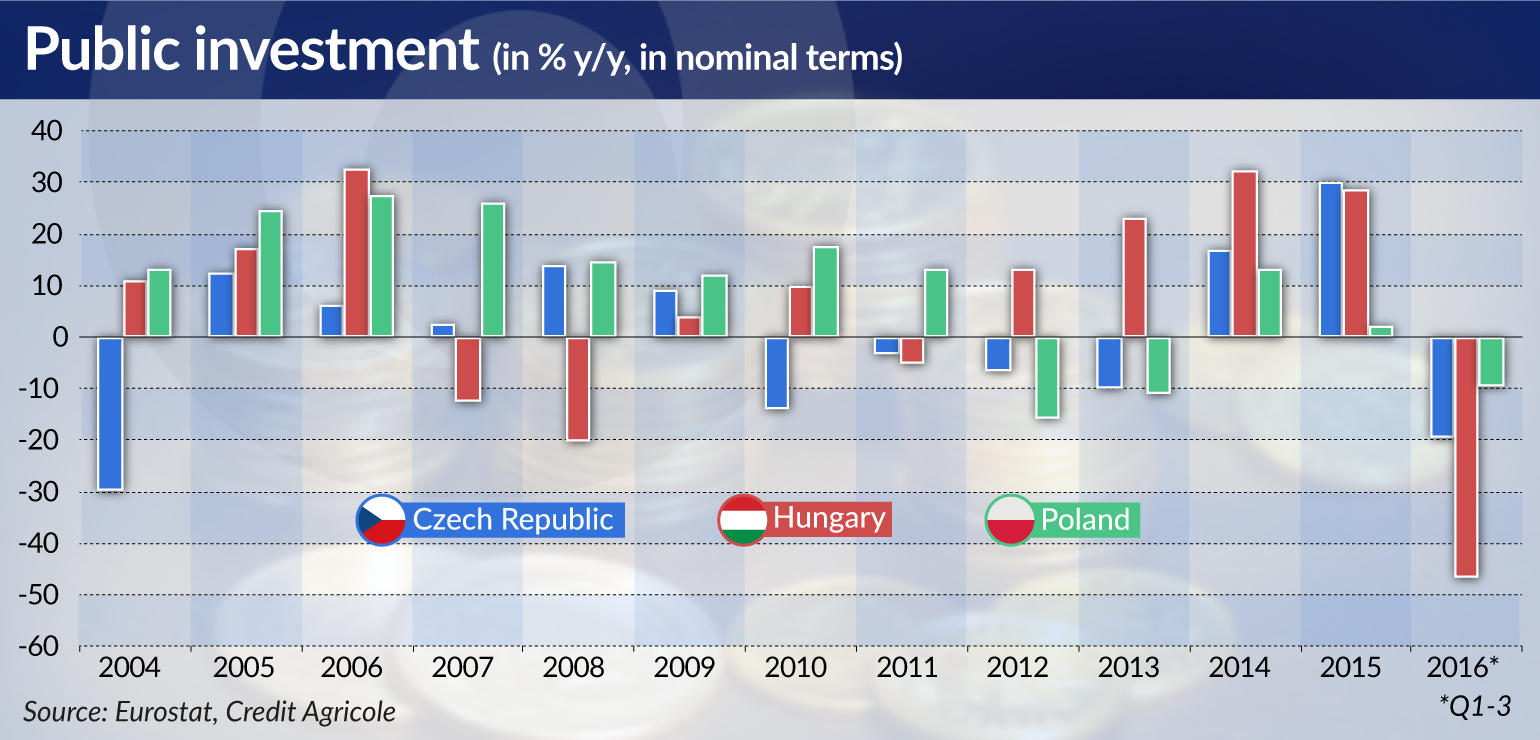

Investment dropped substantially in 2016

The capital expenditure of the public sector from Q1 to Q3 2016 decreased by 9.6 per cent as compared to the corresponding period of the previous year. A similar situation could be observed also in other countries of the region: Hungary and the Czech Republic. Since the beginning of 2016, a marked decrease in income on the capital account to GDP was observed in Poland, Hungary and the Czech Republic. This item includes investment capital transfers (for the Visegrad Group countries this is mainly the inflow of EU funds under the structural and investment programs).

In Hungary and the Czech Republic, a drop of total investment annually was noted since the beginning of 2016, as was also in Poland, which to a large extent resulted from the slowed growth of capital expenditure in the general government sector. However, for Poland, the scale of annual investment drop in the period of Q1-3’16 was considerably lower as compared to the other two countries of the region.

According to the Poland’s central bank, Narodowy Bank Polski survey on the economic climate of the enterprise sector, only 23.5 per cent of the respondents suggested a negative impact of the decline in investment in the economy (primarily public investment) on the standing of their own enterprise, whereas only in half the cases such an assessment was caused by the limitation of own investment in the enterprise. But if we take into account all companies that plan to reduce or have already reduced own investment (16 per cent in total), this was mainly (in 70 per cent of cases) caused by lower investment level in the economy.

In the light of the above results, it may be stated that despite the scale of lower public investment impact on the private sector was probably not very large (if measured by the share of enterprises experiencing the negative effects of the situation), this phenomenon to a large extent translates into the decision to reduce investment in companies.

Jakub Borowski is Chief Economist at Credit Agricole Bank Polska; Assistant Professor at the Department of Economics II of the Warsaw School of Economics.

Krystian Jaworski is Economist at Credit Agricole Bank Polska; PhD Student at the Collegium of Economic Analysis of the Warsaw School of Economics. He is the winner of the 4th edition of the Financial Observer Contest: “If it was up to me, then…”.