Tydzień w gospodarce

Category: RaportyPrzegląd wydarzeń gospodarczych ubiegłego tygodnia (16–20.05.2022) – źródło: dignitynews.eu

Ever since the early nineties of last century, Inflation Targeting (IT) has become increasingly popular throughout the world and is currently being implemented in 11 advanced and 25 developing countries (albeit not in the US, China and the Eurozone, where central banks have – along with the level of inflation – also other targets). A ‘pure’ IT regime essentially means the manipulation of policy interest rates with the aim of achieving a well-defined level of inflation (‘inflation target’). Besides, it assumes a freely floating exchange rate: the operation of foreign exchange market is unperturbed by central bank’s interventions or by administrative controls.

Is such IT regime the right choice for present-day Ukraine, whose economy is small, open and highly dollarized?

There are widely accepted theoretical arguments why the implementation of a ‘pure’ IT accompanied by a flexible exchange rate regime in a highly dollarized economy can be problematic.

In a non-dollarized, small open economy, a negative exchange rate shock (that is, currency depreciation) tends to both fuel inflation (via higher prices of imported goods) and support economic growth (by making the economy more competitive). Monetary policy tightening by the central bank would be an appropriate policy response to such a shock: it ‘cools down’ the economy in order to prevent excessive ‘over-heating’.

However, in a highly dollarized economy, exchange rate depreciation is likely to fuel inflation but suppress economic growth. The volume of outstanding foreign currency loans (expressed in domestic currency terms) goes up in line with the exchange rate and results in additional financial burden for the borrowers, which weighs on the domestic demand (the so-called ‘balance-sheet effect’ of currency depreciation).

Under these conditions, policy tightening by the central bank would be a sub-optimal response: albeit it helps bring down the inflation rate, it amplifies the contractionary impact of currency depreciation and thus works pro-cyclically. Thus, in a dollarized economy, a ‘pure’ Inflation Targeting regime may contradict the task of macroeconomic stabilization, which should be a key concern for the central bank (at least implicitly).

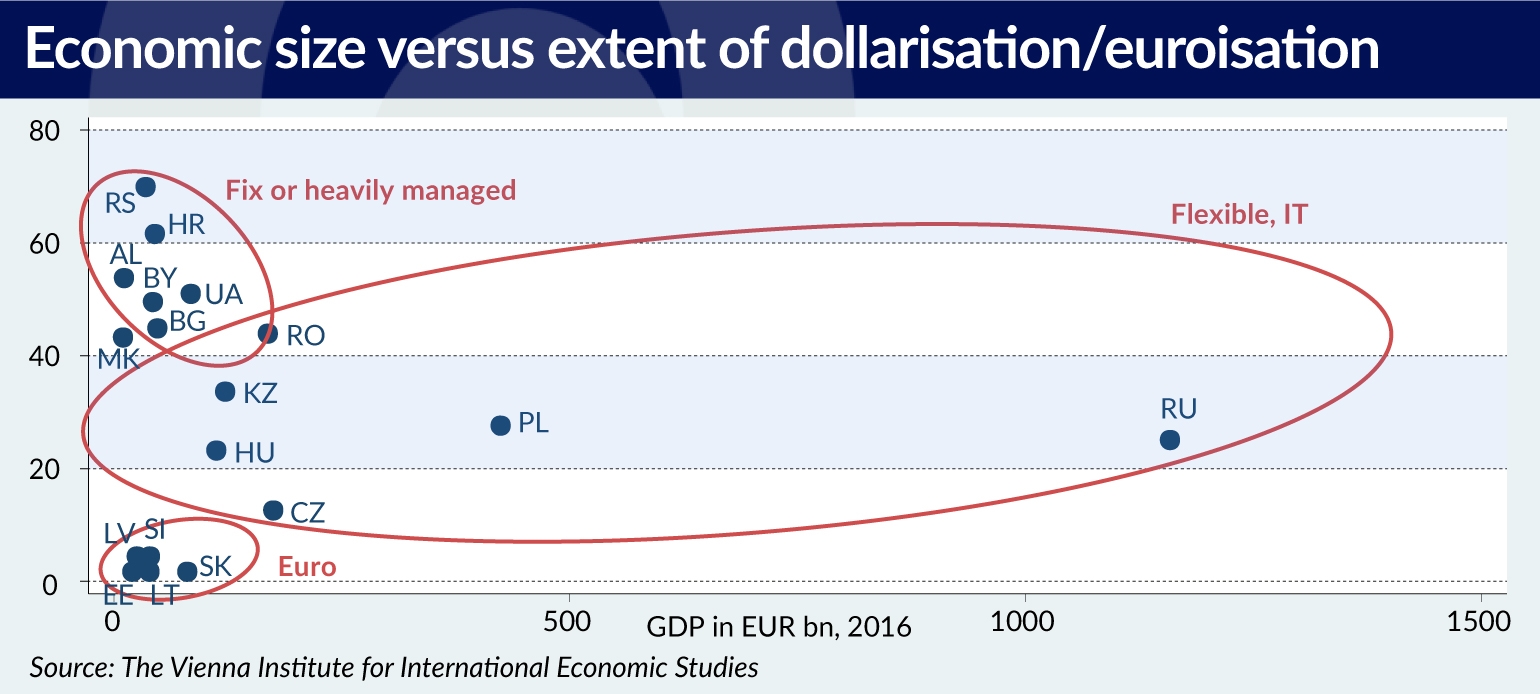

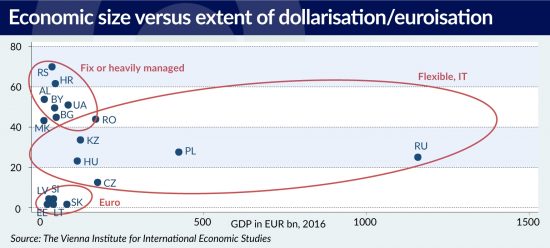

Of what relevance are the above theoretical considerations for Ukraine? Ukraine’s economy is not only ‘small and open’ (its GDP is about the same size as Slovakia’s), but also highly dollarized, reflecting the long-standing tradition of mistrust in domestic currency. Around half of bank loans are still denominated in foreign currency (mainly USD), despite the enacted ban on new foreign currency lending after the global financial crisis of 2008-2009.

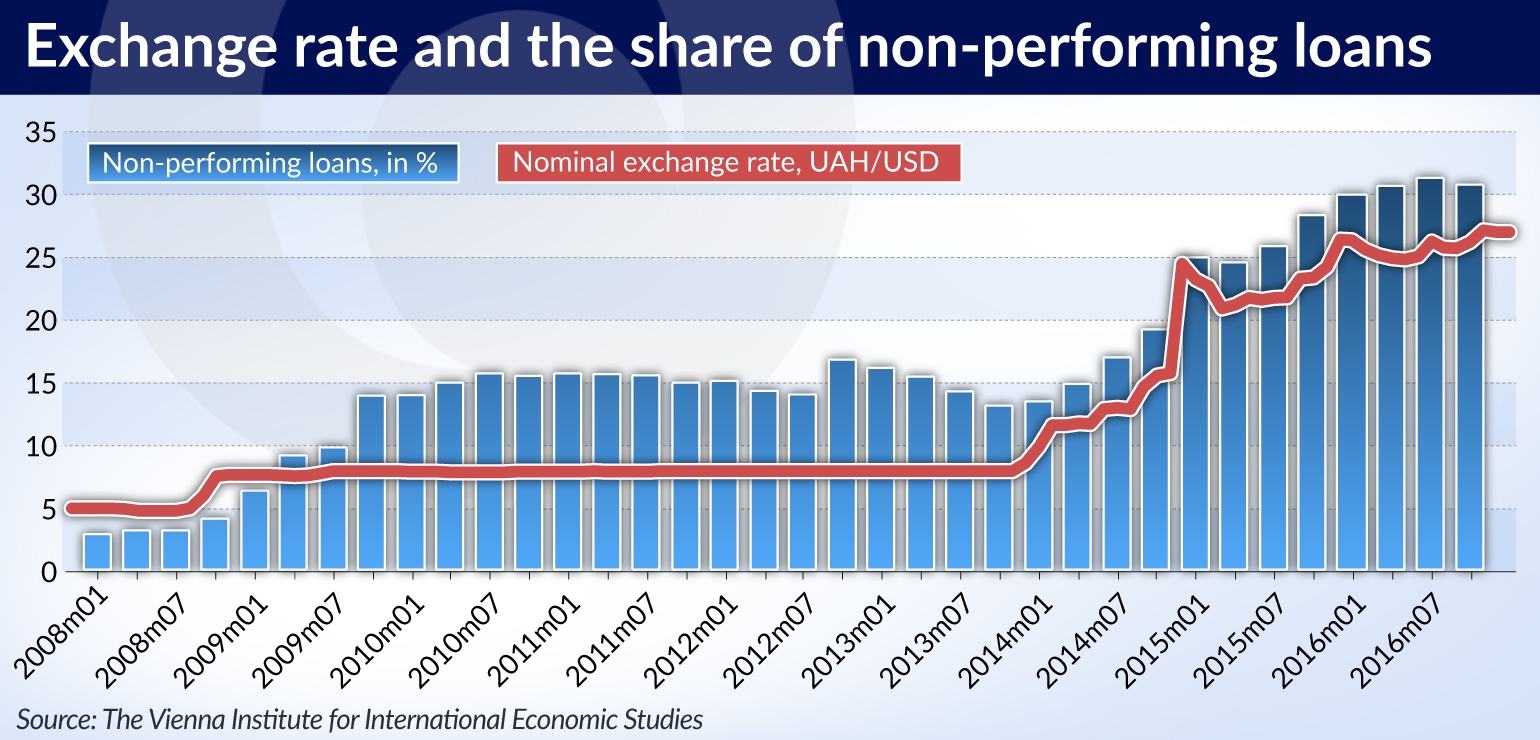

Given the high degree of dollarization, it is little wonder that the recent history of economic crises in Ukraine fits well the above ‘balance-sheet’ theoretical narrative. Figure above demonstrates that every recent episode of currency devaluation has resulted, with a certain time lag, in surging non-performing loans. During the most recent such episode (following a switch to a floating exchange rate regime in 2014), the UAH depreciated around four times, which put the vast majority of foreign currency borrowers under pressure. The ‘balance sheet’ effect has also manifested itself in the dynamics of Ukraine’s public debt, 70 per cent of which is denominated in foreign currency. In 2014 alone, it jumped by 30 pp of GDP, mostly on account of the valuation effect of exchange rate depreciation. The fiscal consolidation package enacted as a result of this surge has suppressed domestic demand still further. At the same time, inflation soared (to 48 per cent in 2015, far above the official target of 20 per cent), forcing NBU to hike its discount rate markedly, up to 30 per cent p.a. and keep it at this level for quite some time. No wonder, credit expansion stalled: as a result, the stock of credits to non-financial private sector contracted in real terms by one-third within just two years (2014-2015). Needless to say, the impact on the real economy was highly contractionary, adding to the pains induced by the depreciation. All in all, in 2014-2015 Ukraine’s real GDP declined by 16 per cent as a result.

Disinflation in Ukraine only became possible, once extensive capital controls (including a surrender requirement on export proceeds, limits on withdrawals of foreign currency deposits, caps on dividend repatriation, etc.) were imposed in spring 2015 and the exchange rate stabilized accordingly. As a result, in 2016 inflation was brought down to 12.4 per cent – thus meeting the official inflation target of NBU (12 per cent). Thus, the success of macroeconomic stabilization in Ukraine has been basically the success of implemented capital controls rather than of Inflation Targeting. In fact, the stabilization only became possible once the IT regime was effectively abandoned. But the existence of capital controls contradicts the very idea of Inflation Targeting, where the exchange rate should be equilibrated by market forces, and – if maintained over a longer period of time – may jeopardize the country’s attractiveness for investments. Even regardless of the objective negative consequences of capital controls for the economy in the medium and long run, the IMF will likely put pressure to gradually abolish foreign exchange controls.

Can it be safely assumed that once capital controls are lifted, the exchange rate of UAH will remain reasonably stable and shocks like those observed in 2008 and 2014 will be avoided? If yes, one could argue that the vulnerability of economy to contractionary ‘balance-sheet effects’ (and the related problems with the implementation of a ‘pure’ Inflation Targeting regime) are less of an issue. Unfortunately, there are good reasons to believe that the exchange rate – if allowed to float again – will likely remain volatile. Instead of being an infamous ‘shock absorber’, it can well become a source of a ‘shock’ itself, with potentially destabilizing consequences for the real economy – especially if amplified by a pro-cyclical Inflation Targeting regime.

The most recent UAH devaluation in 2014-2015 is the best illustration of this. Although it cannot be denied that by the end of Mr. Yanukovych’s presidency, Ukraine has accumulated unsustainable external imbalances, making exchange rate adjustment only a matter of time, the extent of subsequent UAH devaluation cannot be explained other than by purely speculative factors, triggered by political and geopolitical tensions (political instability following the ‘Maidan revolution’, the secession of Crimea, military conflict in Donbass, etc.) Many of these factors may become relevant again anytime: the semi-frozen conflict in Donbass may become ‘hot’ anytime, geopolitical tensions surrounding Ukraine-Russia relations/sanctions have not been resolved, political stability within Ukraine itself remains shaky, and any abortion of the IMF loan program may trigger another wave of speculations against the UAH. Even disregarding the specific political and security challenges Ukraine is facing, its market for foreign exchange is fundamentally ‘thin’: the daily turnover on the interbank market only reaches USD200-300m, making UAH an easy target for speculations.

The above suggests that the adoption of ‘pure’ IT, accompanied by a fully flexible exchange rate regime as Ukraine’s new monetary policy framework, is at the very least pre-mature. The success of macroeconomic stabilization in Ukraine so far has had nothing to do with Inflation Targeting but has been basically due to imposed capital controls. Once those are lifted, the exchange rate is likely to become vulnerable to speculative attacks once again. As argued above, attempts at macroeconomic stabilization in response to such shocks using ‘pure’ Inflation Targeting instruments (such as policy interest rates) will likely have a pro-cyclical impact and thus be painful for the real economy. A better strategy under these circumstances would be to smooth exchange rate fluctuations via direct foreign currency interventions rather than using ‘pure’ monetary policy instruments.

Active management of exchange rate would also help anchor inflationary expectations, which – as researches strongly suggests – are dependent much more on expectations of the exchange rate than on NBU actions (itself a manifestation of low credibility of the latter, which is another problem for a successful Inflation Targeting implementation). Adopting a ‘managed’ exchange rate regime – which could be formally integrated into Inflation Targeting – would be well in line with the experience of a number of countries in Central and Eastern Europe whose circumstances (small open economies with a high degree of euroization) are similar to those of Ukraine.

Vasily Astrov is an economist at The Vienna Institute for International Economic Studies and an expert on Ukraine, Russia and other CIS countries. He assembled comprehensive academic and international experience in the United Kingdom (University of Warwick), Germany (Westfälische Wilhelms Universität), Norway (University of Oslo) and Russia (St. Petersburg State University) and graduated in economics (M.Sc., Dipl.-Vw) and geography (B.A.).