The balance of foreign trade is still positive and in a better state than the economy; however, recent months show a significant change in this trend.

Back in 2012, despite the soaring oil prices, Russia recorded a growing decline in economic activity. The situation deteriorated further as a result of the sanctions against the country introduced in 2014 and above all, as a result of the dramatic fall in oil prices starting from Q4’14.

Thus Russian GDP fell by 3.7 per cent in 2015. The other leading macroeconomic indicators, such as investment, industrial output, income and real wages as well as foreign trade – both exports and imports – also fell significantly. Against this background, the claim that Russia is overcoming the crisis seems over-optimistic.

The analysis of the causes of the improvement of Russia’s balance of payments in 2015 compared to 2014 is interesting. There was a significant increase in the positive balance of the current account and also a reduction of the outflow of capital – more than could have been expected. Moreover, this was in conditions of continuing repayment of the foreign debt.

Balance of foreign trade

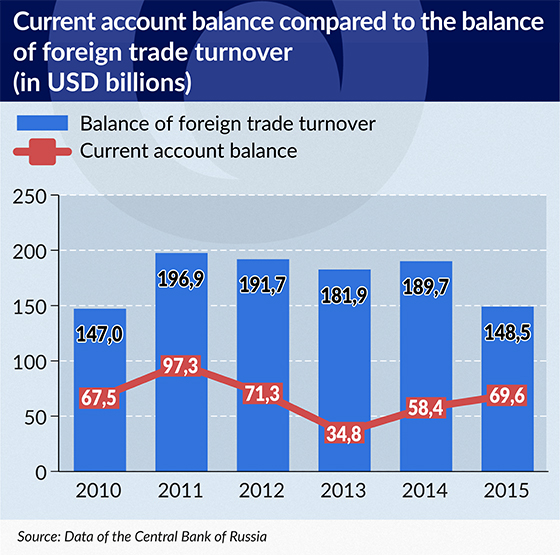

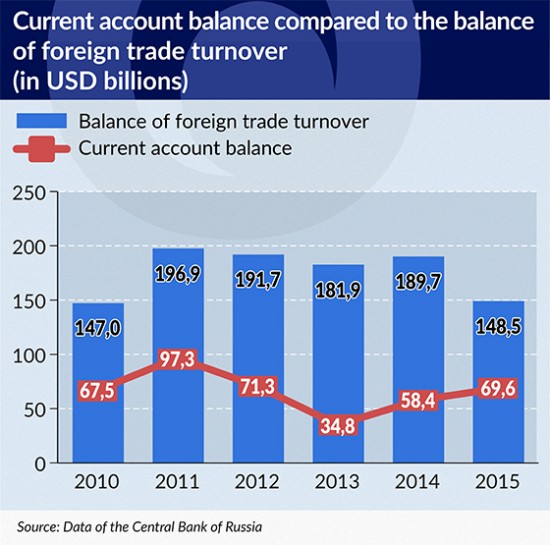

The high positive balance of the foreign trade has a decisive impact on the state of the Russian balance of payments. In the last dozen or so years, the rapidly growing volume of foreign trade has been the most recognisable feature of the Russian economy. On the export side, the primary causative factor in this process is the rapidly growing fuel and commodity prices, including above all oil and gas prices. On the import side, it was investment and the rapidly growing income and real wages of the population, giving rise to investment and consumer demand, satisfied in the main part by imports.

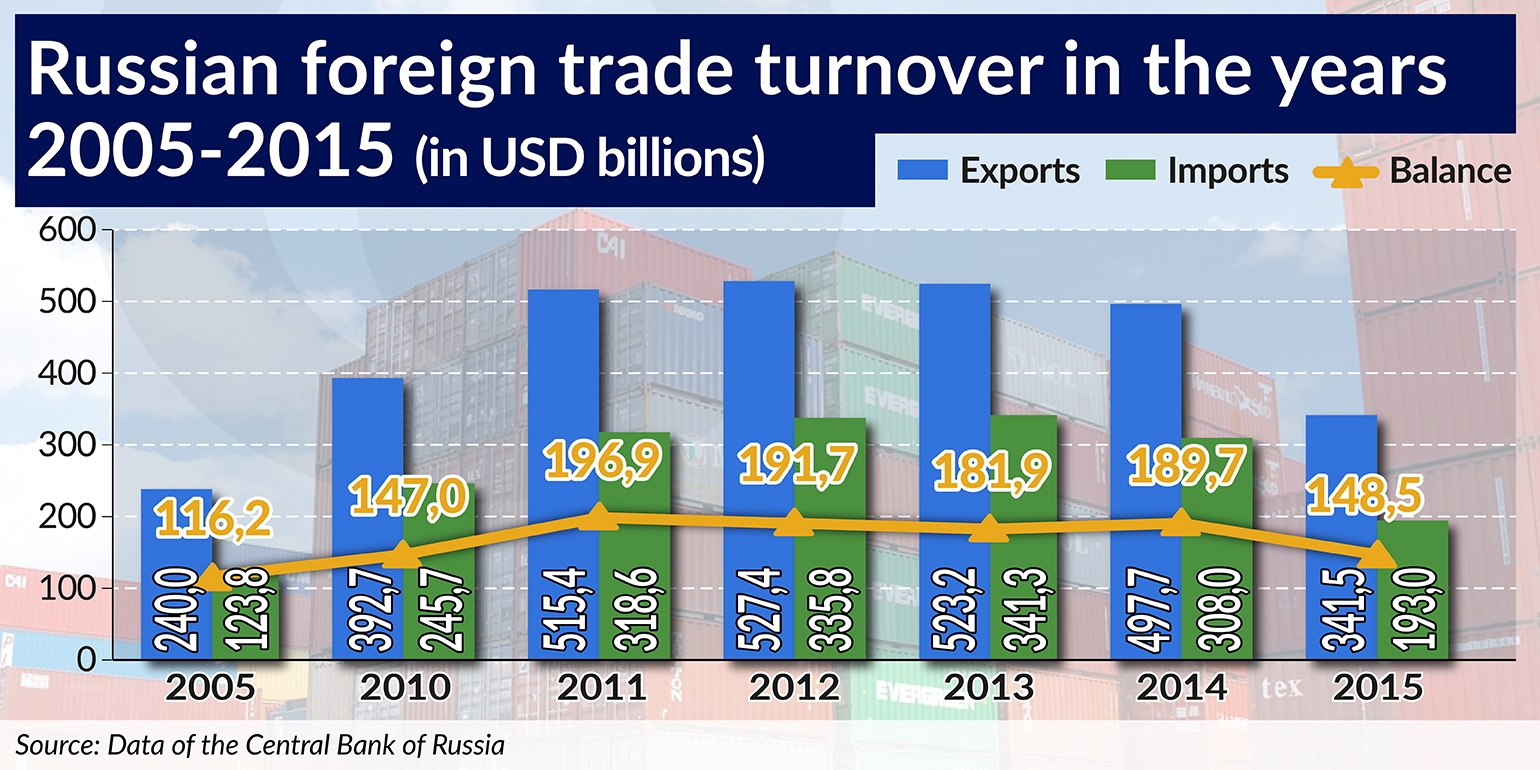

A crucial period in this process was 2005, when for the first time in history the value of exports exceeded USD200bn (reaching USD240bn) and imports stood at USD123.8bn. The positive balance stood at USD116.2bn was also a record.

(Infographics Bogusław Rzepczak)

Another landmark was when exports exceeded USD500bn and imports exceeded USD300bn in 2011. Then, the highest ever level of the positive balance of foreign trade turnover was achieved, approaching USD200bn. In the following years, despite falling, the balance remained high at USD180-190bn. It was only in 2015 that a significant adjustment took place.

The positive balance of foreign trade decreased from USD189.7bn in 2014 to USD148.5bn in 2015. This balance was achieved amid a significant fall in both exports and imports. Exports fell to USD341.5bn, i.e. by 31.4 per cent (USD156.3bn) compared to 2014, when exports stood at USD497.7bn.

The collapse of Russian exports is mainly the result of a significant deterioration in the situation in the global fuel and commodity market, the visible effect of which was the fall in prices. The prices of goods in Russian exports fell by 35.2 per cent, while the tone was set by energy commodities, including oil, with a fall of 47.5 per cent, oil products with a fall of 44.0 per cent and natural gas – 30.2 per cent.

Russia reacted to the deteriorating situation on the commodities market like a typical country with a monoculture export structure. The fall in prices was partly compensated for by a 4.5 per cent increase in export volumes. The largest increase was in the case of energy commodities, including oil (an 8.9 per cent increase in volume) and natural gas (6.4 per cent increase). Exports of the remaining goods expressed in physical terms increased by 3.3 per cent.

The decline of 37.4 per cent in Russian imports, i.e. USD115bn from the level of USD308bn in 2014 to USD193bn in 2015, is a cumulative effect of the worsening economic situation of Russia, resulting in a fall in demand both for imported investment goods and consumption goods as well as the devaluation of the ruble against the dollar exceeding 30 per cent. The Russian counter-sanctions, covering a ban on imports of food products from certain countries also contributed, albeit much more modestly than the above-mentioned factors. Unlike the case of exports, the fall in imports was mainly a fall in their physical volume – by 22.3 per cent – alongside a fall in prices of 18.9 per cent.

Current account balance

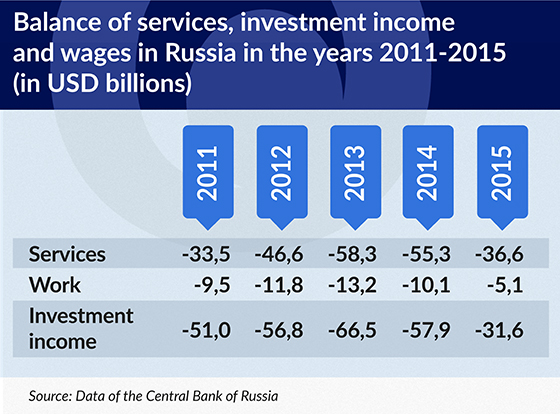

The primary factor adding to the current account is the high positive balance of foreign trade. However, the negative balance of investment income, services and transfers related to wages causes the outflow of funds from this account..

(Infographics Bogusław Rzepczak)

Investment income includes income received by Russians from assets held abroad or income paid from assets held by foreigners in Russia. This includes interest, dividends and other forms of income.

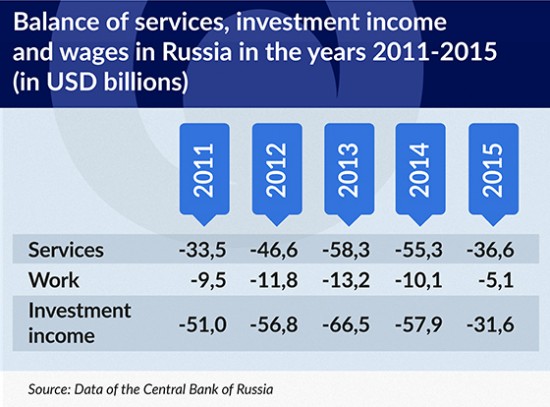

Dividends from invested capital are the decisive factor here. The negative balance of investment income grew in recent years from USD51.0bn in 2011 to USD66.5bn in 2013. The economic collapse, especially in 2015, and the related withdrawal of foreign investors from Russia, as well as the reduced payments from dividends, brought the negative balance in this item down to USD31.6bn. In the case of outflows, transfers declined at the same time from the level of USD90-105bn in the years 2011-2014 to just over USD65bn in 2015. In the case of inflows, however, in the same period they fell from USD38-43bn to just under USD34bn.

(Infographics Bogusław Rzepczak)

In addition to the negative balance of investment income, an equally significant burden on the current account is the negative balance of services. With a positive balance of transport services standing at USD2-3bn in the years 2011-2013 and USD5bn in the years 2014-2015, the item “trips”, which in practice boils down to expenses and income from tourism, has a decisive impact on the negative balance of services. The rapidly growing negative balance of this item increased from USD21.3bn in 2011 to USD32bn in 2012 and USD41.5bn in 2013. Despite falling to USD38.6bn in 2014 and USD26.5bn in 2015, it still creates more than 72 per cent of the negative balance of services.

The expenditure of Russians related to foreign tourism in recent years has grown rapidly. In the years 2011-2013 it increased by almost 63 per cent, i.e. from the level of USD32.9bn in 2011 to USD42.8bn in 2012 (an increase of over 30 per cent) and USD53.5bn in 2013 (an increase of over 25 per cent).

The deteriorating economic situation, resulting in falling wages and real incomes, as well as the ongoing depreciation of the ruble, have begun to restrict the foreign tourist trips of Russians and the expenditure related to this. In 2014 it fell to USD50.4bn. A further deepening of negative economic phenomena – the fall of 4.0 per cent in income, 9.5 per cent in wages, and above all the further depreciation of the ruble, whose average level of RUB37.97/USD in 2014 rose to RUB60.66/USD in 2015 – have translated into a dramatic drop in the number of tourist trips. This trend has been strengthened by fears related to the Russian plane crash over the Sinai and the worsening relations between Turkey and Russia. There was a further decrease in expenditure related to this of over 35 per cent to the level USD34.9bn.

The heading “wages” includes income related to the work of Russian citizens abroad and expenditure connected with the work of foreigners in Russia, mainly from the remittances of the wages of immigrants employed in Russia from the Commonwealth of Independent States from Central Asia, Ukraine, Moldavia, etc. After a period of growing negative balance from USD9.5bn in 2011 to USD11.8bn and USD13.2bn in the following two years, the deteriorating economic situation in Russia, above all the depreciation of the ruble, has reduced the attractiveness of the Russian labour market. This resulted in a fall in the negative balance to USD10.1bn in 2014 and USD5.1bn in 2015. This last result is due to the 50-70 per cent fall – according to estimates – in the influx of guest workers to Russia and a fall in the related expenditure to the level of USD8.6bn in 2015 compared to USD14.2bn in 2014 and USD17.4bn in 2013.

It’s better because everything is falling

In 2015 the Russian current account balance was positive at the level of USD69.9bn compared to USD58.4bn in 2014. The USD11.2bn improvement, i.e. almost 20 per cent, took place despite a significant fall in the positive balance of foreign trade turnover. It fell by USD41.2bn from USD189.7bn in 2014 to USD148.5bn in 2015.

However, at the same time, there was an offsetting effect of more than USD50bn in the form of a significant fall in the negative balance of other components of the current account. The negative balance of services shrank in comparison to 2014 by USD18.7bn, including tourist services by USD12.1bn, investment income (reduced payments of dividends and other payments arising from capital invested in Russia by foreigners) by USD26.3bn and wages by USD5.1bn.

The export of capital from Russia in 2015 stood at USD58.1bn compared to USD152.9bn in 2014. In contrast to the situation in previous years, repayment of the foreign debt was the primary item in the breakdown of the export of capital. The most significant item here was the reduction of foreign liabilities of banks by USD59.8bn. This was at the cost of a decrease in foreign assets of Russian banks (a fall of USD25.8bn) and in the weight of accumulated funds on the current account.

At the same time the significant positive balance on the current account allowed the remaining sectors, despite being cut off from the funds of the international financial market, to not only reduce their foreign liabilities, although only slightly (by USD7.2bn), but to increase their foreign assets, although at a much smaller scale than in previous years (by USD22.4bn), mainly in the form of a direct investment.

Simple reserves have run out

Preliminary estimates of the Central Bank of Russia indicate that in Q1’16 the decline in the positive balance of the current account will deepen. It stood at USD11.7bn compared to USD30bn in the corresponding period of the previous year. Its decline is primarily the result of the further significant deterioration in the positive balance of foreign trade turnover. This fell from USD45.5bn in Q1’15 to USD21.6bn in the corresponding period this year. This process is taking place amid a significant fall in exports by 35 per cent and a slowdown in the fall in imports to 15 per cent.

The impact of the offsetting elements has also been reduced significantly in the form of a further reduction in the negative balance of services (by USD4.7bn in 2016 and USD8.3bn in 2015) and investment income (USD3.4bn compared to USD4.8bn).

In Q1’16, the export of capital declined almost five-fold. Compared to the corresponding period in 2015, it fell from USD37.9bn to USD7bn. Capital export continues to be primarily related to the repayment of foreign liabilities. This applies in particular to banks, whose reduction of foreign liabilities by USD8.0bn was associated with a decrease in their foreign assets by USD7.8bn.

The persistence of unfavourable geopolitical factors and those related to the business cycle and prices in the global fuel and commodities market will result in continued deterioration of all the basic parameter of the balance of payments, including primarily the current account. Under the conditions of being cut off from the international finance-credit market and the necessity of repaying the foreign debt, this will translate into the need for further divestment of foreign assets. The years of external investment expansion of Russian entities from the banking and non-finance sector could soon become history.