The sanctions imposed on Russia by the Unites States, Canada, Norway and other Western countries, following the occupation of Crimea, did not in principle prevent the maintenance and expansion of economic relations between Russia and the individual EU member states.

(Gazprom, Public domain)

As the successor state to the Soviet Union, Russia is considered a superpower. Its President Vladimir Putin was invited (before the occupation of Crimea) to the meetings of the G-8 group. However, the potential of the economy with a population of almost 147 million citizens, as measured by GDP per capita, does not allow us to classify Russia as the economic power.

Although the media reports from the meetings of state leaders often paint a different picture, in reality Russia is only a secondary trading partner for the individual EU member states. In 2017, Germany exported goods worth EUR25.8bn to Russia (for comparison, it exported goods worth EUR59.5bn to Poland), and imported goods worth EUR31.5bn (Germany’s imports from Poland amounted to EUR51bn). Russia is only the 15th largest recipient of exports for France, while Poland is the 10th. For Italy, the Russian market is only the 13th top export destination, while Poland takes the 9th spot. Russia is the 27th largest recipient of the United Kingdom’s exports and the 24th largest supplier of goods to the United Kingdom (Poland ranks 22nd and 13th, respectively). Even for Hungary, which maintains an excellent relationship with Russia, the country is only the 17th largest recipient of exports and the 10th largest supplier of imported goods — Poland ranks 8th and 3rd, respectively.

Paradoxically, Russia is a much more important economic partner for Poland than for the majority of Western European countries, even though the relations between the two countries have been strained for years. Russia is the 7th largest recipient of Polish goods and the 3rd largest supplier of Polish imports. This, of course, is due to the imports of energy raw materials — crude oil, petroleum products and gas.

Each year Russia sells to other countries about 260 million tons of oil and a similar volume of petroleum products. Approximately 37 million tons are sold to the Netherlands, 28 million tons to Germany, and 20 million tons to Poland.

In 2017, Gazprom sold 242 billion cubic meters (bcm) of gas abroad. Out of that, 192.2 bcm were sold to European countries, including 158.38 bcm to EU member states (the 10 major recipients include Germany, Italy, the United Kingdom, France, Poland, Austria, Czech Republic, Hungary, the Netherlands and Slovakia). This means that the EU market accounts for two-thirds of the Russian gas exports and chances that Russia can quickly become independent from sales to EU member states are low.

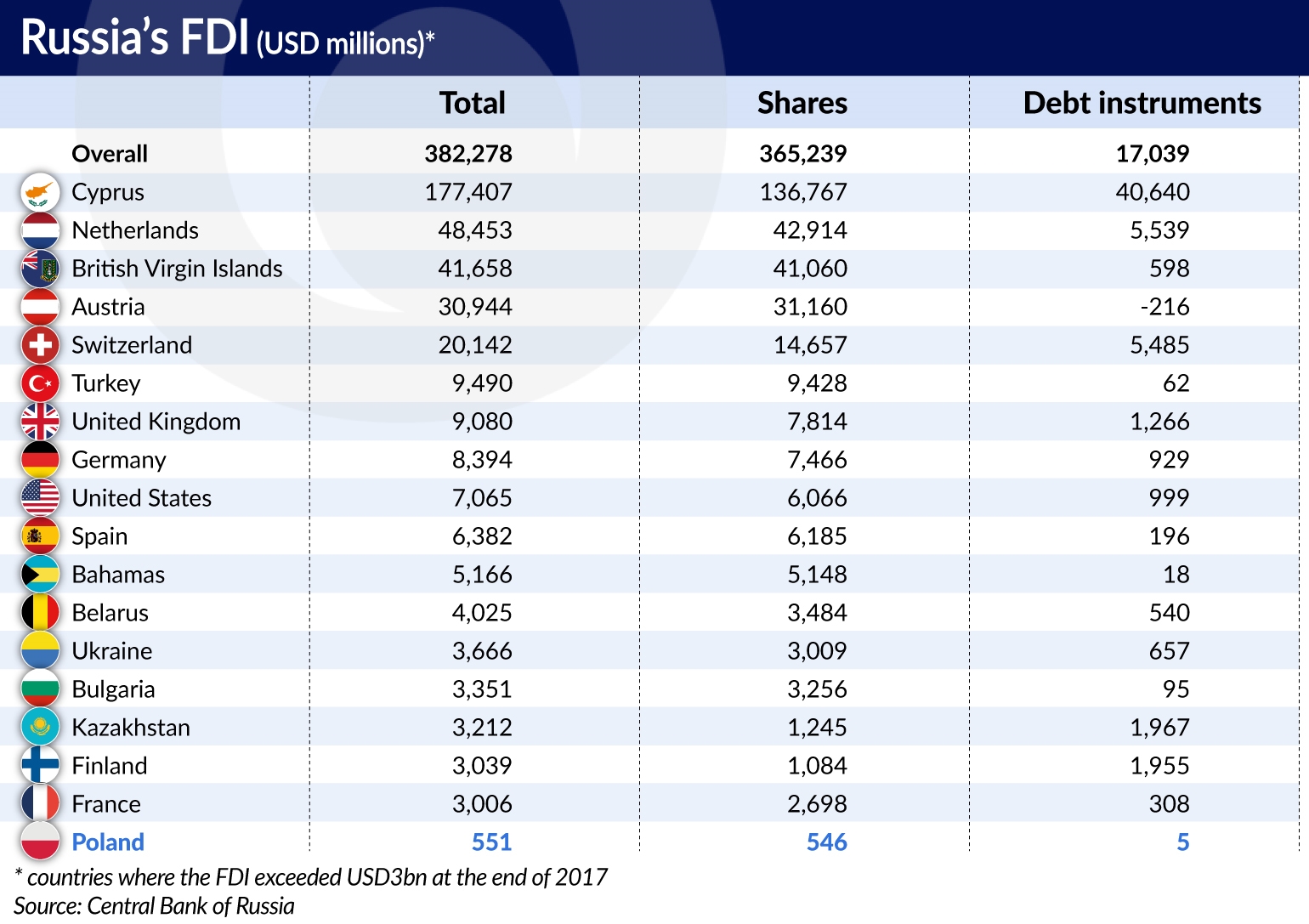

Russia is investing in Europe

According to the Central Bank of Russia, in 2017 the value of direct investments in Russia amounted to USD27.9bn, out of which USD14.2bn came from EU countries.

The total value of foreign direct investment (FDI) carried out in Russia thus far amounted to USD48bn (at the end of 2017), and the total value of Russia’s foreign investment reached USD382.3bn. At the end of 2017 the largest recipient of Russian investments (stock) was Cyprus, which accounted for up to 46 per cent of Russian capital invested abroad.

Some of the Russian capital is kept in tax havens. Among the EU member states, the largest recipients of Russian capital apart from Cyprus include the Netherlands, Austria, the United Kingdom, and Germany. According to data from the Central Bank of Russia, Russian entities have so far invested just over USD0.5bn in Poland, out of which almost USD100m was invested in 2017.

Russian capital is mainly invested in the energy sector. In Poland, Gazprom owns 50 per cent of a section of the Yamal gas pipeline through a subsidiary company. The largest Russian non-state owned corporation, Lukoil, also owns gas stations in the country.

Western European governments typically do not object to the takeover of local refineries and elements of gas and oil infrastructure by Russian corporations. In January 2017, Rosneft (50 per cent of its shares are held by the Russian state, 19.75 per cent belong to BP, and stakes are also held by the Swiss company Glencore) took control of an oil refinery in Schwedt in Germany and a minority stake in two other refineries in southern Germany. Alongside Gazprom, Rosneft is the largest Russian investor in Germany.

In October 2014, after the introduction of sanctions against Russia, Gazprom finalized the takeover of the largest gas warehouse in Western Europe, located in Rehden in Lower Saxony, Germany. The facilities were purchased from Wintershall Holding, a subsidiary company of the BASF group. In return, BASF acquired a 25.01 per cent stake in the project for the extraction of oil, gas and condensate from the Urengoyskoye field in West Siberia. Gazprom has shares (in some cases 100 per cent stakes) in dozens of companies in the European Union member states, including 11 in the Netherlands, 10 in Germany, 9 in Cyprus, 7 in Austria, 6 in Hungary, 6 in the United Kingdom, and 2 in Italy.

In 2014, the German government also approved the sale of the German energy group DEA to the Russian oligarch Mikhail Fridman. DEA was previously owned by RWE. The company possesses gas storage facilities in southern Germany. The transaction was worth many billions of EUR, but it did not appear in the statistics of Russian investments, as the official buyer was the company LetterOne based in Luxembourg.

Russia’s relations with the Netherlands were seriously strained after a Malaysian airplane, in which the majority of passengers were Dutch citizens, was shot down over Ukraine in March 2014. However, the Netherlands are the most important trading and investment partner of Russian companies outside Germany, and the incident did not change that. Lukoil has a 50 per cent stake in the Zeeland Refinery (the other 50 per cent stake is held by the French group Total). Gazprom has concluded a number of partnership agreements with Dutch companies, both in the field of production and shipping of natural gas, even though the Netherlands is a large gas producer itself.

Banks with Russian capital operate in the European Union member states. This includes Sberbank, which is the largest bank on the continent in terms of capitalization. Sberbank Europe AG, with its seat in Vienna, operates in Croatia, the Czech Republic, Germany, Hungary, Slovenia and countries of the former Yugoslavia that don’t belong to the EU.

Who will profit from Nord Stream 2

Gazprom has a 100 per cent stake in the Nord Stream 2 AG project company, which is headquartered in Zug in Switzerland. In April 2017, Nord Stream 2 AG signed agreements with five Western European energy companies — Engie, OMV, Shell, Uniper and Wintershall — on the financing for the construction of an undersea gas pipeline. Engie is a French company, OMV is an Austrian enterprise, Royal Dutch Shell is a mixed British-Dutch company, while Uniper and Wintershall are German. These are all private companies listed on the stock markets, but the French government owns more than 24 per cent of shares in Engie, while the state institution ÖBIB owns over 30 per cent of shares in OMV. Wintershall is owned by the chemical giant BASF. The remaining companies have negligible or no state shareholding at all, but these corporations are so important that they consult their strategic investment decisions with the governments. France, the Netherlands and Germany supported the sanctions against Russia. However, they did not stop the corporations from becoming involved in the Nord Stream 2 project, quite the opposite — they supported the project.

“Nord Stream 2 is the shortest route for gas supplied to Central Europe,” said in March Joachim Pfeiffer, a CDU politician specializing in energy issues. Pfeiffer is a member of an informal German-Russian working group on energy cooperation, which includes members of parliament from both countries, as well as representatives of the business community. “We believe that this is not a political, but a private project, exclusively financed with private and not public funds. It will increase competition and security of supply,” he added

Gazprom claims that 200 companies in 17 European countries will be involved in the construction, and that 1,000 additional jobs will be created. The pipes are being stored in Germany, Finland and Sweden. The latter country did not support the project, but it did not object to it either and issued a positive opinion on the investment’s environmental impact. The total cost of the investment is estimated at EUR9.5bn, and the European corporations will provide EUR950m each.

The Russian side will assume the entire risk related to the profitability of the undertaking. If the investment doesn’t pay off (e.g. due to gas supplies lower than planned and lower gas prices), the losses will be borne by Gazprom, and not by the financial investors.

In May 2018, the construction of the pipeline started in Lubmin on the German coast of the Baltic Sea, and according to schedule it will be completed in 2020. The pipeline will run along the bottom of the Baltic Sea, parallel to the original Nord Stream gas pipeline launched in 2011. The twin-string pipeline will have a capacity of 55 bcm per year, which means that it will be able to deliver one-third of all gas exported to Western Europe. Because gas production in the EU will decrease in the coming years due to natural reasons, the largest importers, including Germany, Italy, Austria and France, do not want to hear about applying sanctions against Nord Stream.

In May, the United States warned that the US sanctions could be applied against companies financing and implementing the Nord Stream 2 project. European companies believe that this is a part of a game played by the Americans who want to become a significant exporter of gas to the European market themselves.

Russia’s influence is greater than the size of the trade exchange

Russia’s influence in many EU member states is much larger than what could be expected based on the size of the mutual trade turnover. Russia is still a significant power in terms of military capacity, and has an extensive network of diplomatic and intelligence services. There are suspicions that it attempts to affect the results of elections in many foreign countries.

The most famous European lobbyist for Russian interests is the former German chancellor Gerhard Schröder. In 2005, during his last weeks in office, he signed an agreement with Russia on the construction of the Nord Stream 2 gas pipeline on the bottom of the Baltic Sea, bypassing Poland, Ukraine and the Baltic States. Shortly after leaving his post, the ex-chancellor became a member of the supervisory board of the Nord Stream 2 consortium tasked with the construction of the pipeline. In 2017, he became the chairman of the Board of Directors of Rosneft.

In 2011, the OPAL gas pipeline was launched, and its shareholders are two German companies: Wingas (80 per cent stake) and E.ON Ruhrgas (20 per cent stake). That pipeline is the eastern branch of the Nord Stream gas pipeline’s inland extension. The OPAL pipeline was exempted from the application of the German and EU regulations concerning competition on the gas market. It is primarily used by Gazprom, which controls the Wingas company.

Russia’s relations with Italy had been close already in the time of the Soviet Union, as well as during the reign of Silvio Berlusconi. Italy supported the creation of a NATO-Russia Council, advocated for Russia’s inclusion in the European Union’s Eastern Partnership program and opposed the tightening of sanctions against Russia in response to Russian military operations in Ukraine and Syria.

The Italian corporation Eni has a 50 per cent stake in the Blue Stream undersea gas pipeline connecting Russia with Turkey via the Black Sea. About 30 per cent of Eni’s natural gas comes from Russia. Additionally, Eni is Rosneft’s partner in the implementation of two exploration projects in the Russian sections of the Barents Sea and in the Black Sea. The Italian company SAIP supplies oil and gas extraction equipment to Russia.

The Intesa Sanpaolo banking group has been operating in Russia for 40 years. In 1989, it created the International Moscow Bank together with Russian shareholders. It was one of the main organizers of financing for the Blue Stream project in 2000. In 2003, the company opened ZAO Banca Intesa — the first bank registered in Russia that is fully owned by Italian capital.

Moscow has established close relations with the Five-Star Movement (MS 5) and La Lega, the Italian Euro-sceptic parties that formed the new Italian government a month ago. MS 5 calls for a reduction in national defense spending and is reluctant towards NATO, which is in line with Russia’s interests.

In France, Russia sponsored the National Front party in last year’s elections. The right-wing candidate, François Fillon, who was seen as the favorite but ultimately lost the election, held a position that was favorable to Russia. In an interview he said: “Russia is a huge country that we cannot treat flippantly. The idea that we can break down Russia by imposing economic sanctions is naive. Our relationship with Russia should be rebuilt.” President Emmanuel Macron is not regarded as a friend of Mr. Putin, but in May he willingly participated in the St. Petersburg International Economic Forum (SPIEF). “France wants to become the biggest direct investor in Russia,” said the French President during the forum and added: “French companies currently employ 170,000 Russian citizens. In the past 10 years, no French company has withdrawn from the Russian market.”

France encouraged Russia to become involved in the fight against the Islamic State in Syria, where (incidentally) it is involved itself. Another common problem for both countries is the maintenance of the nuclear agreement with Iran, associated with the permission for Iranian oil to be exported to the world markets. In addition to the previously mentioned Total and Engie, the French corporations doing business with Russia include Électricité de France, which cooperates with the Russian company AvtoVAZ, and the banking group Société Générale, which owns the Rosbank in Russia.

In Hungary, the government of Victor Orban maintains a special relationship with Russia, which granted a loan of EUR10bn for the expansion of the nuclear power plant in Paks. The power plant is located 100 km south of Budapest and was built in the 1980s with the use of reactors produced in the Soviet Union. Its four operating reactors provide about 40 per cent of the country’s demand for electricity.

At the beginning of 2014, Hungary signed an intergovernmental agreement on the extension of the power plant with the Russian state-owned company Rosatom. This will be the largest investment in Hungary after 1989. Its costs are estimated at USD12bn, a large part of which is supposed to go to Hungarian companies that will carry out various works at the power plant. The two new reactors in Paks will produce more energy in total than the current four, which will be shut down in the years 2032-2037.

A unique position in Russia’s economic strategy is occupied by Cyprus. About 40,000 people with Russian citizenship live on that island today — the vast majority reside in Limassol, where there are several Russian schools, nurseries and kindergartens. The Russian Commercial Bank (currently RCB Bank) was founded there in 1995. Its headquarters are located in Limassol and it also has branches in other parts of Cyprus and in Luxembourg. One of the members of its management board is the Nobel laureate Prof. Christopher Pissarides.

Almost one-fifth of all the people employed in companies with Russian capital in Cyprus work in the financial sector. Other areas dominated by Russian capital include tax consultancy, corporate services, beauty and health services, tourism, marketing services, and aircraft leasing. Many Cypriot companies with Russian capital invest in the European Union.

After the European Union imposed sanctions on Russia, many Russians left the EU member states in which they lived. This didn’t happen in Cyprus, whose government maintains excellent relations with Moscow, even though it did not veto the sanctions. Last year the island was visited by 3.6 million tourists, 1 million of whom were Russians. According to the Cypriot law, a foreigner who invests at least EUR2m in real estate obtains the citizenship of Cyprus within six months. Russians are the main group taking advantage of this mechanism – last year they purchased real estate worth EUR4bn.

The Russians in Cyprus refer to the city of Limassol as Limassolgrad. Until recently, they also jokingly referred to the British capital as Londongrad. The United Kingdom, and especially London, was the most favorite investment destination for wealthy Russians. However, the United Kingdom is one the countries which treat the sanctions against Russia seriously, especially after the murder of Alexander Litvinenko, likely committed by the Russian secret services. This radical approach was further strengthened after the poisoning of Sergei Skripal, a former Russian intelligence officer.

The British authorities carefully verify the capital and people allowed into the country. Special visas for persons investing over GBP2m have been subjected to verification since 2015. After the United Kingdom began meticulously checking whether the funds intended for investments were derived from legal sources, the number of applications for such visas decreased by as much as 84 per cent. A new law came into force this February, which allows the British authorities to demand that foreigners prove how they obtained assets of “dubious origin’ if their value exceeds GBP50,000. In the event of refusal the funds may be confiscated.

Roman Abramovich, one of the richest Russian oligarchs, closely associated with Mr. Putin, has encountered difficulties with renewing his visa. In 2003, Abramovich purchased the English football club Chelsea and has lived in London since then. He invested over the GBP1bn in the club, turning Chelsea into one of the best teams in Europe. Jim Ratcliffe, the owner of the petrochemical giant Ineos and the wealthiest man in the United Kingdom, has recently made an offer to buy the club. Abramovich didn’t sell, however, has abandoned his plans to expand the stadium. Instead, he started investing in Israel. In 2015, Abramowicz bought the Varsano Hotel in the Neve Tzedek district in Tel Aviv, turning it into his Israeli home. Every fifth inhabitant of Israel has Russian roots and the country will certainly not join in the sanctions against Russia.

Russia is a small country. From an economic perspective, that is. According to the IMF, the country’s GDP amounted to $1.7 trillion in 2021. That is barely 10% of the European Union’s GDP, or roughly the combined output of Belgium ($620 billion) and the Netherlands ($1.1 trillion).