Tydzień w gospodarce

Category: Trendy gospodarczePrzegląd wydarzeń gospodarczych ubiegłego tygodnia (30.05–03.06.2022) – źródło: dignitynews.eu

Poland was moved from the Advanced Emerging Markets category to the Developed Markets category. The decision was taken in September 2018 by the independent FTSE Russell Country Classification Advisory Committee. September is the month when the FTSE Global Equity Index Series — an entire family of capital market indices — is subjected to a review.

This decision means that Polish assets will have their share in the FTSE Developed All Cap Index. Previously, they were included in the FTSE Emerging All Cap Index. What is also important is that the weight of the Polish assets in the emerging markets index is now 1.33 per cent, and the country’s reclassification to the developed markets index (starting from September) that weight is expected to reach 0.154 per cent. The developed markets index includes capital market assets from 23 countries, which means that the Polish assets will have a very modest weight.

FTSE Russell said that the decision was the result of “continuous improvement in Poland’s capital market infrastructure, supported by the country’s steady economic progress”. It was also motivated by the fact that Poland is the largest economy in Central and Southeast Europe (CSE), that is, a region in which no country had been classified as a developed market before. Moreover — Poland has been waiting on the agency’s watch list since 2011.

FTSE Russell is a global provider of benchmarks, analyses and other solutions for the analysis and processing of market data and for their collection. It belongs to the London Stock Exchange group and has been operating for over 30 years. Asset managers, ETF providers and investment banks around the world compare the performance of their investments with its indices. These indices are used for the creation of investment funds, ETF funds, structured products and index-based derivatives. Investments benchmarked by the FTSE Russell indices are worth about USD15 trillion, which of course does not mean that all of them are strictly linked to these indices.

Let’s admit it right at the start — FTSE Russel is an important provider of stock market indices, but it not the most important one. That position is occupied by MSCI, a company that was created by the American investment bank Morgan Stanley. Poland is included in the MSCI Emerging Markets Index, which has been computed since 2001, among 23 other countries representing 10 per cent of global stock market capitalization. This index reflects approx. 85 per cent of the free float on each of the 24 markets. Shares from China have the highest weight in the MSCI EM index, accounting for approximately 30 percent.

MSCI also calculates a separate index for Poland (MSCI Poland Investable Market Index) which comprises the shares of 39 companies listed on the Warsaw Stock Exchange. Ten companies from the WIG20 list account for two-thirds of the overall index weight. The market capitalization of these companies is USD74.7bn, while the capitalization of the MSCI EM index is USD5.48 trillion. Any reshuffles within the MSCI Poland index are of considerable importance for the stock quotes of Polish companies. When it was announced in mid-May, that Tauron (one of the energy companies with State Treasury as a shareholder) would be dropped from the index, the prices of the company’s shares embarked on a sharp downhill ride, losing 15 per cent in the space of a few days. Will the shares behave similarly in the case of FTSE Russell classification changes?

„This index is not as closely followed by investors, and the impact probably won’t be very big”, says Emil Łobodziński, investment advisor at the Brokerage House of PKO Bank Polski S.A.

Apart from MSCI and FTSE Russell, another global index provider is STOXX, whose EURO STOXX and STOXX Europe 600 indices are important benchmarks for the stock markets in the Eurozone. It also publishes the STOXX Poland TMI index. The Standard and Poor’s and Cboe index families do not cover Poland.

Therefore, the “promotion” of the Polish capital market by FTSE Russell is mainly of symbolic significance. What is interesting, however, is how the agency justified the „maturity” of the Polish market.

FTSE Russell emphasized that this is the first such promotion of a country from the Advanced Emerging market category to the Developed market category in nearly a decade. What were the criteria for this historical — in a certain sense — decision? The agency’s current classification system has been in place since 2004, and the criteria that countries have to meet in order to be included in a given category are quite strict.

They cover four areas: Market and Regulatory Environment, Custody and Settlement, Dealing Landscape, and Derivatives. These areas are further divided into 21 categories. In order for a country to be qualified to a given category, it has to pass an appropriate number of criteria. These mainly relate to the quality of the market. In order to be included in the developed markets category, all 21 criteria have to be met.

Additionally, the country must have a relatively high gross national income per capita. This is the first surprise when it comes to Poland’s promotion. In this respect, Poland could be compared with other advanced emerging markets, such as the Czech Republic or Hungary within CSE, or Turkey outside of it. The poorest country among the developed markets, i.e. Portugal, has a gross national income per capita that is over 50 per cent higher than Poland, and the vast majority of other countries have incomes that are at least twice higher. On the other hand, in the category of advanced emerging markets these disparities are also large. Some countries have a gross national income per capita that is more than twice as large as that of other countries, like Taiwan and South Africa. This means that this criterion is not entirely unambiguous.

What may seem surprising, is the fact that among the countries of our region, only the Czech Republic and Hungary are classified in the advanced emerging markets category, while Russia is included in the „secondary emerging markets” category. All the other countries — Bulgaria, Croatia, Estonia, Latvia, Lithuania, Macedonia, Romania, Serbia, Slovakia and Slovenia — are classified in the „frontier markets” category, alongside countries such as Argentina. This is a category of markets that are at an early stage of development and that are considered relatively risky, even though some of them belong to the euro area, and the credit ratings of a few of them are higher than that of Poland. The same is also true for the MSCI classification.

This clearly indicates that the attractiveness of a given capital market does not have to be closely linked to the given country’s wealth or its economic or social development. So what is the factor determining whether a given market is seen as developed or not?

What matters above all is the size of the economy. That is the obvious reason for Poland’s „promotion” and the marginal position of some other Central European economies. Poland is the seventh largest economy in the European Union and by far the largest one in the region. All the smaller economies are simply too small from the point of view of global investors. And as a consequence they are classified as less „developed”.

The capital market infrastructure is of a key importance in the classification. While the bonus for the size of the economy seems obvious in the case of Poland, the criteria related to the infrastructure are much more challenging. After a quarter-century of developing the capital market in Poland, it was finally noticed on the global scale, although for the time being its weight only constitutes a fraction of a per cent.

The most important criteria relate to the quality of the capital market. What is taken into consideration here is the market and regulatory environment. This includes the existence and operation, as well as the quality of regulators monitoring the stock market, the recognition and observance of minority shareholders’ rights, lack of restrictions on foreign ownership, lack of restrictions on transfers of capital and dividends, the liquidity of the stock market and the foreign exchange market, and whether the registration process for foreign investors is not too complicated.

The next group of criteria covers issues related to the settlement and custody of securities. This means that errors in settlements should be rare, that the custodian institutions should provide high quality services, that investors should be able to choose from a large number of such entities, and that settlements should be carried out quickly — the T+2 standard is desirable (up to two days after the transaction).

The key criteria also include those relating to the rules of trading (so-called „dealing landscape”) and the associated infrastructure. This mainly relates to the requirement of sufficient competition, ensuring high quality of brokerage services. Other very important criteria include the sufficient liquidity of the broad market, the possibility of short selling and lending stocks, as well as the ability to conclude off-session transactions. What is also important is the transparency of the transactions, and not just the of issuers, i.e. open and timely of trade reporting process.

Another group of criteria cover the access to the market and the associated costs. The point is that international investors should be able to invest and withdraw funds in a timely and safe manner at a reasonable, fair and competitive cost, without incurring hidden fees. The assessment of the cost of access to the Warsaw stock market as „reasonable” could serve as an important argument in many ongoing domestic discussions concerning stock exchange fees or the fees of the National Depository for Securities. Of course, these costs are viewed somewhat differently from the perspective of London than they are in Warsaw.

Before any country is classified or reclassified to any of the categories, it is subjected to long-term observation and is placed on a watch list. During this time, the agency analyzes the legislation and its changes, the reforms and their pace as well as the ongoing business practice. Once the decision-making bodies determine that the changes are established, permanent and sufficient — they move the market from one category to another. However, they always do it gradually — the countries are always promoted or demoted by one category at a time.

These decisions are not made very quickly. The Advisory Committee analyzes the reports of the local market authorities and then verifies them directly. There are discussions with a wide range of stakeholders, and the entire process is consulted with the agency’s clients. To put it briefly — FTSE Russell provided the Warsaw stock market with a certificate of credibility.

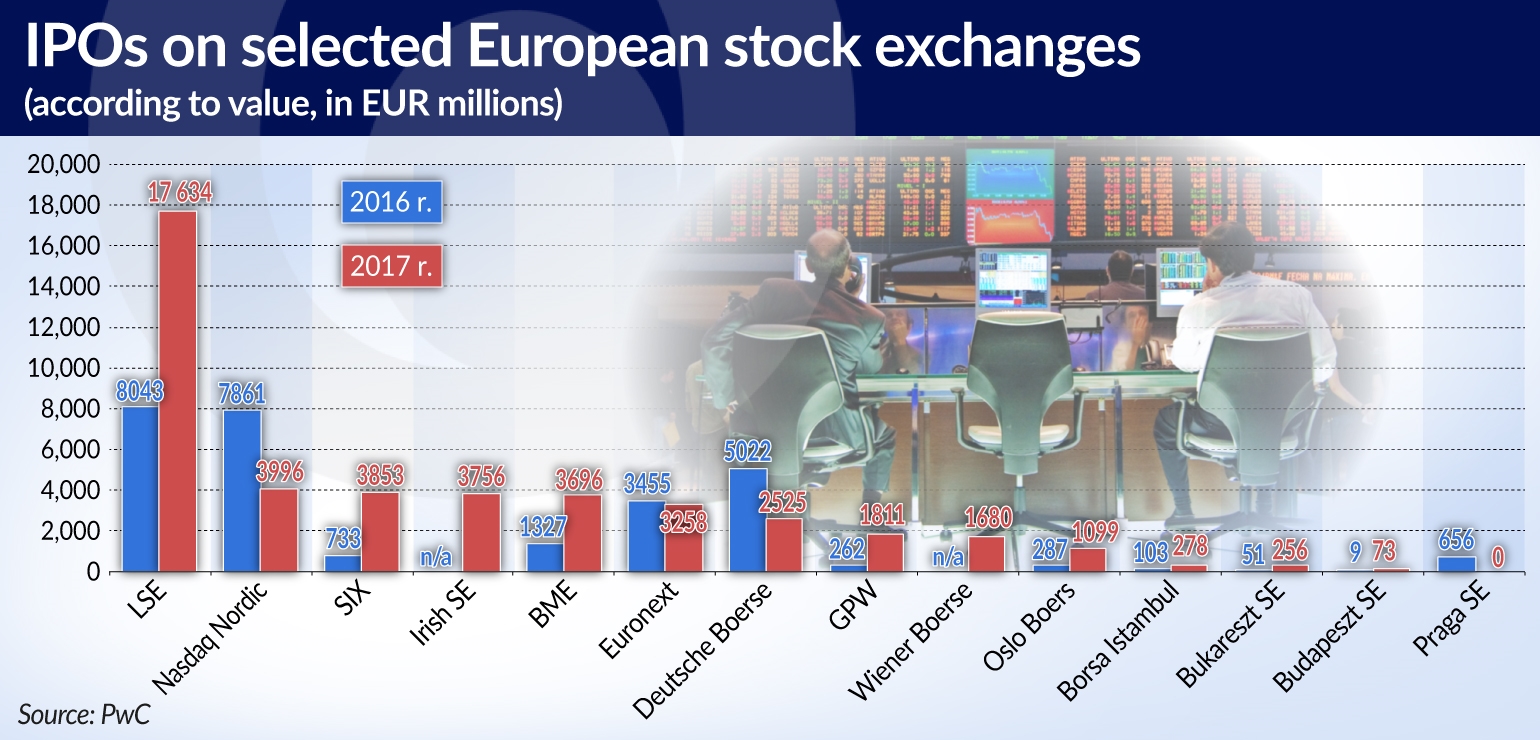

FTSE Russell reports that its decision was influenced by the fact that the Polish market is not only quite large but is also steadily growing. The turnover on the Warsaw Stock Exchange increased by 28 per cent in 2017. The arguments for the promotion also stemmed from the fact that the WSE was the third largest capital market in Europe in terms of the number of Initial Public Offerings (IPOs).

„Taking into account the energy market, the CO2 emissions allowances and the Catalyst market, the statistics and initiatives indicate a likely deepening and strengthening of Poland’s capital markets in the years to come”, the PwC wrote.

Concerns related to the reclassification were mainly associated with the question of whether the Polish market would suffer any losses due to the fact that its weight in the developed markets index will be so low. This should not be the case, however. The capitalization of the FTSE Developed Markets index is USD44.6bn, while the capitalization of the FTSE Emerging Markets index is USD4.7bn. An index weight of 0.154 per cent translates (statistically) into nearly USD70bn. The current weight of the Polish market in the FTSE Emerging Markets index corresponds to a value of approximately USD62bn. This means a reserve of approx. USD8bn. That amounts to just over 2 per cent of the market capitalization of the Warsaw Stock Exchange.

„From the point of view of the whole country, this is good news, but from the point of view of the individual companies — not necessarily. The reclassification does not have to be beneficial at all, and for some companies it may even result in a decline in their importance”, says Emil Łobodziński.

According to the stock market analysts, the largest and most liquid companies should benefit the most. This includes PKO BP (the biggest bank in Poland) and PZU (the biggest insurer in Poland), and perhaps PKN Orlen (the biggest oil&gas company in Poland), which also have the largest shares in the MSCI index.

Institutions investing in developed markets will likely gradually increase their portfolios of Polish stocks. These will mainly be stable and long-term investors, such as pension funds. They will be less susceptible to swings between risk appetite and risk aversion exhibited by investors in emerging markets. And another such swing is approaching right now in connection with the normalization of the monetary policy by the Fed and the outflow of capital to the United States. Therefore in the long term, the decision of FTSE Russell should stabilize the Polish stock market — even though it only accounts for such a small fraction of the index. At the same time, however, the decision was taken shortly before the Warsaw capital market was left in shock after the debt collection company GetBack failed to redeem its bonds and filed a motion for restructuring proceedings. The market participants admit that this case could shatter the confidence of investors.

One of the players on the capital market said that some financial institutions offered to their clients the bonds placed by GetBack in private offerings, which constitutes a circumvention of the Public Offering Act. That piece of legislation allows the sale of securities by way of a private placement (non-public offering) to no more than 149 identified entities. On the one hand, the quality of the Polish capital market legislation is high — on the other hand, we can see have fragile it really is.

If all the allegations raised in connection with GetBack’s insolvency are confirmed, it could turn out that the Polish capital market, as observed on the ground in Warsaw, is in fact much less mature than it seems from the perspective of London. This case will likely not affect the decision made by FTSE Russell, however. From London’s perspective, it’s difficult to even notice the GetBack case.