(By D. Gąszczyk)

From 1 January 2013, the amount of the contribution transferred by the Social Insurance Institution (ZUS) to OFEs will increase from the present 2.3% to 2.8% of the pension contribution calculation base. The gradual increase in contributions transferred to OFEs, to 3.5% from 1 January 2017, was a compromise agreed within the main ruling party, the Civic Platform. It aimed to weaken the negative reaction to other provisions, namely those of the Act of 25 March 2011 amending certain acts related to the functioning of the social security system, affecting OFEs.

Juggling with accounts

When the government worked on the 2013 budget, the question arose whether it intended to change the rules of financing OFEs. According to the statements of the Minister of Finance, Jacek Rostowski, and the Chairman of the Economic Council, Jan Krzysztof Bielecki, this case was neither considered by the government (nor by the Economic Council, which played an important role in 2011 as it prepared the justification for the reduction in OFE contributions). In other words, the government plans to raise, in accordance with the Act, the amount of OFE contributions, which will result in a decrease in the budget of the ZUS and the need for refinancing it by the State.

The draft 2013 budget envisages an increase in the refinancing of contributions from PLN 8.4 to 11.3 billion, or by about PLN 2.9 billion (with PLN 2 billion resulting from the increase in the level of the contribution, and 0.9 billion − from the increase in the payroll budget burdened with the contribution.

The government recognises that the issue of the functioning of the 2nd pension pillar is so delicate in political and social terms that currently it should not be raised. This does not mean that the government would not attempt to liquidate or put restrictions on the functioning of OFEs should major problems with maintaining public debt below 55% of GDP (according to the domestic methodology) arise.

One of the possibilities of closing the budget, which is considered by the commentators (the government neither confirms but also does not deny to mull the scenario) is to transfer savings accumulated in OFEs by persons in pre-retirement age to the ZUS. Owing to this operation (it was mentioned by minister Rostowski a couple of months ago), the government, instead of creating secure funds for people who will retire soon, would transfer the responsibility for managing them to the ZUS.

In Open Pension Funds, pension accounts of persons in a certain age would be liquidated and instead the ZUS would create sub-accounts for these persons, where pension liabilities would be recorded (similarly to sub-accounts to which contributions amounting to 5% of the calculation base are currently transferred). Also, contributions would be posted on the debit side and allocated for current payouts.

This operation would amount to a one-off injection of liquidity into the ZUS and reduction in the deficit of the ZUS, and thus no need to refund it from the budget. If pension liabilities posted to ZUS sub-accounts were not classified as public debt (as is the case now), taking over by the ZUS of the accounts of people in pre-retirement and retirement age would stand for a one-off reduction in public debt and a corresponding increase in uncovered pension debt. As the second category does not affect the current assessment of the financial condition of the State, the taking over of some OFE clients by the ZUS seems an easy way to “write off debt of the State.”

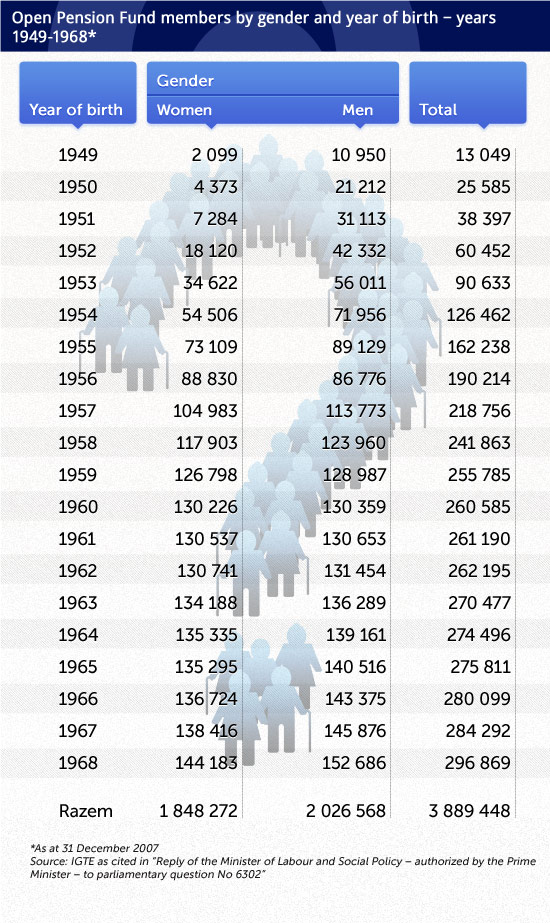

People born between 1949 and 1968 had a choice if they wanted to become OFE members or to remain with the ZUS. Many people, especially younger ones, decided to go for OFEs. If the ZUS obligatorily took over accounts of men who are 60 and women who are 55, next year OFEs would already lose about 660,000 members (500,000 women and 160,000 men), that is ca. 5% of its members. The value of their savings in OFE accounts is over PLN 20 billion, that is ca. 1.3-1.5% of GDP.

As people born in subsequent years would reach the retirement age minus five years, their savings from OFEs would be transferred to ZUS sub-accounts. Because there are more and more people born in subsequent years (to those born in 1968) who joined OFEs, the money accumulated in funds is larger (currently, men born in 1954 and women born in 1959 have collected about PLN 5 billion).

In addition, pension payouts from the ZUS would increase at a faster pace because it would pay the entire amount of the pension, not only the 1st pillar. Pension debt (which is currently not disclosed in national accounts statistics or in ESA 95) would become explicit debt.

(By D. Gąszczyk)

Responsibility without a guarantee

The manner of paying out pensions from OFEs has not been decided yet. We do not know who would pay them, whether they would be indexed and by what indicator. According to the initial objectives of the reform, pensions were to be paid by private funds, although other than OFEs. The pension amounts were to depend on accumulated savings and on life expectancy. They would be indexed only if the value of the investment portfolio grew.

Taking over Open Pension Fund money by the ZUS would be tantamount to taking over the responsibility for maintaining the real level of pensions by the State. With the declining growth rate of the economy, this would therefore translate into a need to subsidise the pension system by the budget.

During the discussion on the government’s proposals, the Minister of Finance used an argument that government guarantees for future pensioners were more reliable than market guarantees (resulting from the effects of the investment portfolio). The issue, however, is that the government may not be able to meet these commitments and an attempt to do this may lead to a public finance disaster.

The taking over of pension accounts of elderly people would mean a postponement of the debt issue in time. Would such an operation be profitable per saldo? Would it depend on the pace of economic growth in the subsequent years, the level of interest rates or inflation? If within several years successive governments abandon reforms allowing to reduce certain fixed expenditure and adverse demographic and economic trends persist (primarily, a reduction in the number of working persons as a result of the ageing of the population and emigration), the issues of deficit and increasing debt would soon re-emerge.

The threat also consists in the fact that a one-time inflow of funds into the Social Insurance Institution (and thus into the budget) discourages the authorities from seeking other ways of public finance consolidation.

Also, safer options of taking over OFE savings would be possible. The ZUS would not allocate them for current payouts, but run its own fund from which a part of pensions would be paid out. The decline in public debt would depend on the method of carrying out this operation.

The two major opposition parties have other suggestions concerning OFEs.

Law and Justice opts for free choice

In March, Law and Justice (PiS) presented a draft amendment to the Act on the social security system and to the Act on the organisation and functioning of pension funds. Law and Justice proposes that OFE members could decide whether their contributions are to be transferred to OFEs or to the ZUS and in what amount. The insured could determine on their own if this would be 1.5, 2.5 or 3.5%. In Law and Justice’s opinion, the vast majority of the insured would opt for the ZUS.

However, the proposal of Law and Justice is not consistent. On the one hand, it talks about the abolition of the obligatory OFE membership, on the other hand, this optionality refers to the future only. The people who start work who would not declare membership in any fund, would not be forced to do so by way of a draw. They would just remain in the ZUS. Also, the people insured in OFEs could resign from further transferring of their contributions to the funds.

Yet, the draft Act does not provide for transferring the already accumulated savings from OFEs to the ZUS. Also, Law and Justice does not explain to the public that its proposal would not stand for returning to the situation prior to the pension reform. The basic principle of the reform − defining the contribution, not benefits, would be maintained.

It is difficult to estimate the consequences of adopting the Law and Justice’s proposal. PiS experts believe that the majority of the insured would choose the ZUS, but it does not have to be provided that the effects of the changes are properly explained and understood.

Similarly as in the case of the taking over of savings of people in pre-retirement age by the ZUS, the consequence of the Law and Justice’s proposal and of “the return of Open Pension Fund members to the Social Insurance Institution” would be taking over the responsibility for the amounts of future pensions by the State. Consequently, this could lead to uncontrolled debt growth in the future, provided that the next government does not withdraw from this commitment.

Democratic Left Alliance opts for a state-owned Open Pension Fund

The Left proposes establishing a state-owned Open Pension Fund, competitive for those already existing ones. According to the Democratic Left Alliance (SLD), the advantage of this solution would be to force private funds to reduce their running costs.

The state-owned fund could invest in a fixed basket of financial instruments (Treasury bonds, Warsaw Stock Exchange indices and several other markets, gold, crude oil). Such a balanced portfolio does not require considerable activity on the part of fund managers and thus commissions for its management would be low. Experience shows that in the long run portfolios of this kind yield returns no worse than those of actively managed portfolios.

The risk connected with this solution consists in the possibility of its politicization. Anyway, SLD does not hide it. In its programme, it announces the use of the money from the state-owned pension fund for financing various projects − for example, building the infrastructure, new technologies and even renewable energy.

Therefore, it would be highly risky or, by definition, low profit-yielding projects (infrastructure). Investing in these areas would require new instruments that would have to be guaranteed by the State. The result could be losses which would increase State debt. An additional disadvantage of this kind of strategy would be making the results of the State open pension fund conditional upon the standing of public finance. If the State has more and more difficulties with debt servicing, guarantees granted to the instruments in which the fund would invest would lose their value.

Of course, a similar situation may occur in the case of Treasury bonds. If the State has debt repayment problems, OFEs whose portfolio covers more than 50% of such securities, would suffer losses.

Balancing the pensioner

In this case, losses would also be borne by pensioners receiving their pensions from the ZUS, whose income depends on the inflow of the current stream of taxes (contributions). Therefore, it is essential that the State, when modifying the pension system, bore its balancing in mind.

It is obvious that the more generous promises made to future pensioners, the greater risk of the system’s failure in the future. From this point of view, both a reduction in the pension contribution transferred to OFEs and proposals for taking over a part of retirement savings by the State or further reduction in the stream of contributions to OFEs increase the risk of the system’s insolvency.

It is worth remembering that the pension system, which was established in 1999, had gaps from the beginning, and they were closed only partially. In the future, guaranteeing the minimum pension by the State will be the most expensive.

As life expectancy increases (if not accompanied by the concurrent extension of the period of paying contributions), the increasing part of pensions, resulting from accumulated contributions, would be below the guaranteed level. Subsidising them would burden the current State budgets, which at some point could result in a collapse of the pension system.

Privatisation of accounts

It would be the safest solution for State finance and our future pensions to privatise OFE accounts − to transfer the money accumulated in the accounts to fund participants who could pay it into a savings or investment account of their choice in any bank or fund. The amount of contributions transferred to pension accounts from that moment on would depend on individual decisions.

In addition, the State should encourage savings by increasing the limit of funds not taxed with the personal income tax or the capital gains tax. Currently, only up to 4% of the remuneration may be written off from the personal income tax base, not more than PLN 4,030 a year transferred to Individual Pension Security Accounts. This limit should be raised, at least to 10% of the remuneration. Also, it is necessary to change the method of guaranteeing pensions paid out by the State, including the minimum ones. Pensions must depend on the amount of revenues of the State pension system. Otherwise, the system would become a mere pyramid scheme, with all the consequences.

(oprac. graf. DG/CC By desbyrnephotos)

OF