In its annual report the Polish Institute of Economic Forecasts and Analyses indicates the day of the year on which the Polish economy symbolically emerges from the grey area. This year it was March 4th. This means that from the beginning of the year until that day, the annual added value is generated in the shadow economy. After this date all production is assumed to take place exclusively within the formal economy.

In order to avoid misunderstandings and incorrect interpretations, the analysis of the shadow economy is carried out in accordance with the national accounts method. In sociology or legal studies the grey area is understood more broadly. In the approach applied in economic studies, the activity in the shadow economy consists the creation of GDP, and more precisely, added value, outside of the formal economy — the activity is not reported in tax returns and statistical reports. This involves the production of goods and services which are delivered to the market and are priced on the market. This production satisfies demand and generates incomes.

The shadow economy involves:

- legally operating enterprises concealing the actual size of the production (hidden activity);

- informal activity conducted by unregistered natural persons;

- illegal activity, which in the official estimates of Statistics Poland (GUS) covers the production and distribution of drugs, cigarette smuggling, and profiting from prostitution.

Tax evasion

It’s worth adding that tax fraud, including the evasion of value added tax (VAT), is included in the category of the shadow economy, as it reduces the state budget revenues. When loopholes in the tax system are eliminated, that is, when undue earnings are taken away from dishonest entrepreneurs, the size of the shadow economy decreases, but no added value is created. The value added is simply shifted from the enterprise sector to the state budget. On the other hand, common theft does not belong in the category of shadow economy, because it does not generate any added value and merely leads to a change in the distribution of income.

However, Polish government’s hopes of further increasing budget revenues from the shadow economy as a result of continued elimination of the loopholes in the tax system are overly optimistic. This limitation results from the fact that a large percentage of the companies operating in the shadow economy are simply unable to obtain sufficiently high profits if they have to pay taxes. This is what pushes them into the informal economy in the first place. If they are forced to pay taxes, many of them will simply go out of business.

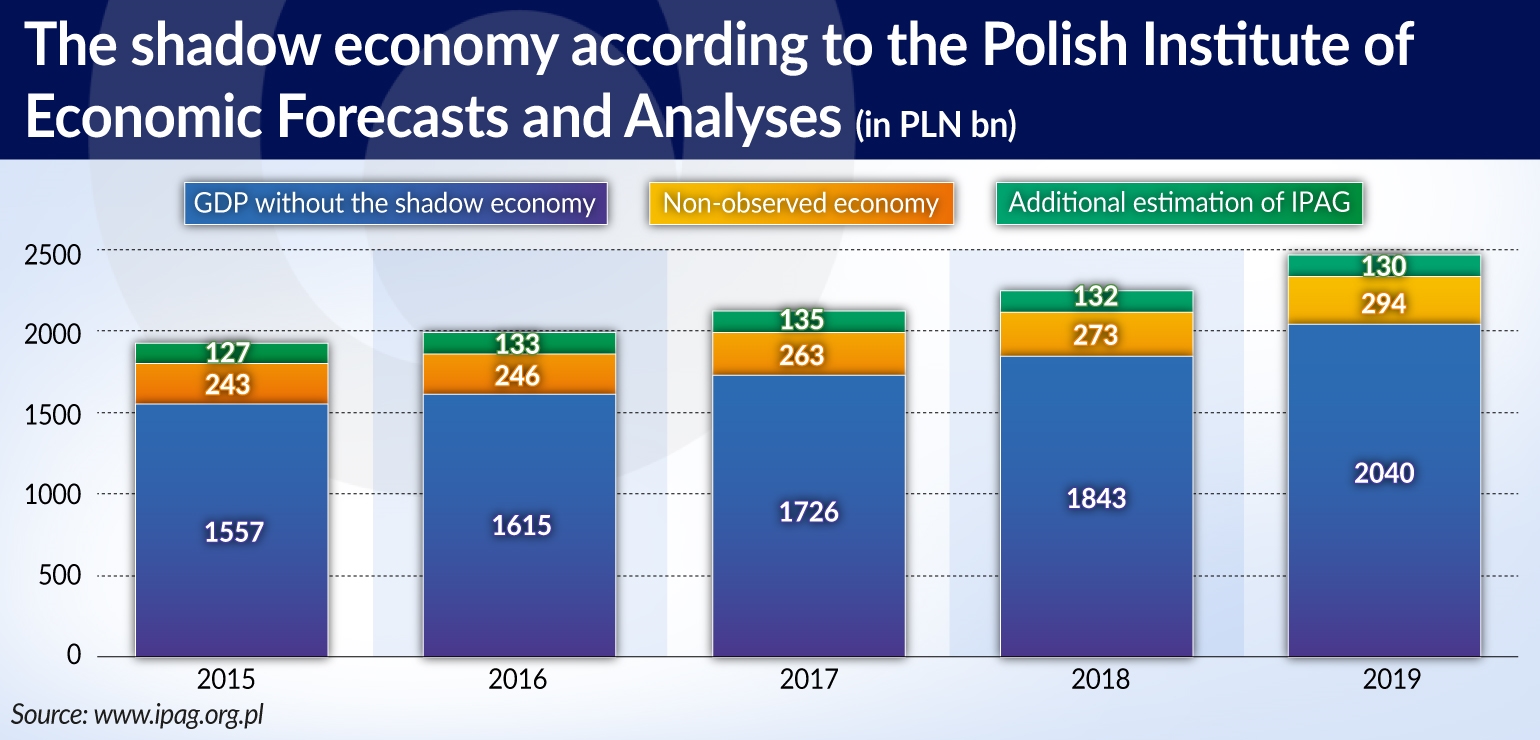

According to the forecast of the Polish Institute of Economic Forecasts and Analyses, in 2019 about 17.2 per cent of the GDP will be generated in the shadow economy. The most recent available estimates of Statistics Poland (the so called “non-observed economy” category), covering the period until 2016, were adopted as the starting point for the calculations.

IPAG has projected the size of the shadow economy for the years 2017-2019 in the part covered by the estimates of Statistics Poland and has additionally estimated the size of several other areas of business activity which contribute to the shadow economy in Poland, and which were not fully taken into account by GUS.

Economic theory and empirical research indicate that excessive state regulations are the main systemic cause leading to the development of activities outside of the official economy. Other important factors include the bad economic situation in the individual industries, as well as the low tax morale of producers and consumers.

The analyses conducted by IPAG indicate that the vigorous activities undertaken by the tax authorities, the legislative changes, as well as coordinated actions within the governmental administration, in the years 2014-2018, led to a reduction in the size of the shadow economy from 19.5 per cent of GDP in 2014 to 17.2 per cent forecasted in the current year.

Cash settlements

Systemic measures aimed at reducing labor costs, reducing bureaucratic burdens, simplifying the administrative procedures and legal regulations, as well as limiting the volume of cash transactions, could prove to be equally effective in combating the shadow economy.

This is due to the fact that payments in the shadow economy are usually carried out in cash in order to cover the traces of concealed economic activity. Research and experience from various countries show that cashless transactions contribute not only to a reduction in the scope of the shadow economy, but also have a positive impact on economic growth.

Due to the actions of the Polish authorities over the last few years, the resilient representatives of the shadow economy have been forced to regroup. This was possible due to the fact that the shadow economy is spread out in the majority of economic sectors and has an illegal component.

The regrouping involved the withdrawal of capital from sectors where the actions of the authorities were being acutely felt, towards other areas of business activity, less exposed to detection by the authorities. Another method was to move the capital abroad. For example, illicit cigarette factories run by Polish citizens were detected in the Benelux countries. There are more examples of such activities. The results of Poland’s central bank, NBP research indicate that capital withdrawn from the shadow economy is probably responsible for a part of the increase in cash purchases of apartments. The value of cash purchases of apartments in the seven major cities grew from PLN2.03bn (EUR476m) in the Q4’14 to PLN4.83bn (EUR1.13bn) in the Q4’17, that is, by as much as 137 per cent.

Purchases of real estate can be seen as an example of attempts to move profits obtained from the informal economy towards safe investments. It could also indicate that some people are withdrawing from the shadow in favor of legal business activities after accumulating a sufficiently high level of capital. The official economy has always been intertwined with the shadow one, and this will likely continue to be the case in the future.

Underreporting of sales and turnover figures

The reduction in the size of the shadow economy in some business sectors was accompanied by its expansion in others, which may have been influenced by certain elements of the state’s economic policy. Surveys and estimates of GUS indicate that the largest portion of the shadow economy is attributed to legally operating enterprises which underreport their turnover figures.

This primarily relates to small enterprises and micro-enterprises. In the case of the latter, there is little difference between the average wages of their employees and the official minimum wage, which has been significantly increased over the years. In 2018, the gross minimum wage amounted to PLN 2,100 (EUR492) and was 86.5 per cent higher than 10 years ago. Meanwhile, the remunerations of non-minimum wage employees increased at an incomparably slower rate.

According to estimates prepared by IPAG, in 2018 the average gross remuneration of nearly 70 per cent of employees working in micro-enterprises did not exceed the amount of PLN2,500 (EUR586). Such a ratio of the minimum wage to the average wage contributes to a phenomenon in which employees receive a part of their remuneration “under the table”.

As a result, companies obtain unrecorded revenues, most often by failing to issue fiscal receipts to their customers. This primarily applies to a wide range of services provided to the public, in which it is absolutely necessary to employ qualified workers. In its report, IPAG also discusses the issue of foreigners’ employment in the shadow economy. The average number of such employees in 2018 was estimated at approximately 571,000.

Shadow economy in the Mazowieckie voivodeship

Another topic presented in the report is an experimental study — based on economic modelling — striving to identify the distribution of the shadow economy in the individual voivodships in Poland. The study shows that the share of the shadow economy ranges from 12 per cent of GDP in the Kujawsko-Pomorskie voivodship (northern Poland), to 21 per cent of GDP in the Mazowieckie voivodship (central Poland).

The report also includes an analysis of the shadow economy in the housing rental market, and especially the short-term apartment rental market. This sort of activity provides competition not only for the hotels, but also for companies operating so-called condo hotels and apartment hotels, which operate legally, mainly in large cities and tourist resorts. In this market segment, the main source of problems for all the stakeholders is the lack of clear regulations and their coherent interpretation. As a result, flat-rate taxation is applied to premises rented out for commercial purposes, even though that tax measure was solely provided for the renting of apartments for residential purposes.

One of the three elements of the shadow economy is cigarette smuggling and the illegal production of cigarettes. IPAG estimates the value of cigarette smuggling at PLN3.4bn (EUR796.4m) and the value of illegal domestic production of cigarettes at PLN0.7bn (EUR164m) in 2018. The share of the shadow economy in the cigarette market has been falling since 2015, when it reached 19 per cent. By the Q3’18 it dropped to 11.4 per cent. This is the result of a number of regulatory measures and systemic changes. In the near future we can expect a further reduction of the shadow economy in the tobacco industry.