For the time being the changes have not caused a shock, but they may at any time lead to disturbances with far-reaching consequences. Although there is growth in the economy, the balance of other risks does not change.

The joint committee of the agencies that make up the European financial safety net, i.e. the EBA, the ESMA and the EIOPA, announced a new biannual report on risks and vulnerabilities in the European financial system. The previous report, published in autumn 2016, mentioned weak economic growth and low rates of return, low profitability of the financial institutions and the growing interconnectedness of the financial system as key systemic threats.

Towards the end of 2016 the financial markets saw the emergence of expectations of an increase in the risk premium and the diversification of its valuation in different classes of assets. The agencies indicate that so far yields in the European Union exhibited a moderate response, but the search for higher yield continues in various classes. In addition, the tendency for a relatively low credit risk premium in the EU might not be sustained in the long term if the interest rates disparity continues to deepen.

Liquidity problems have increased along with an increase in price volatility. The risks associated with the valuation of assets remain at a high level. From time to time there are episodes of high price volatility, and all of this is reinforced by political risks.

How could the markets react to political events? The coordination of international financial reforms, also in the future, has been called into question. This leads to an increase in the risk of regulatory arbitrage, including the relocation of the activity of financial institutions to countries with more lax regulations.

China is currently in the process of change towards an economy based on consumption. The manufacturers of goods have to adapt to moderate price levels. This puts into question the viability of various kinds of businesses.

Politicians undermine the effectiveness and benefits of mechanisms making up the standards of international cooperation, which is especially visible in the context of the Brexit. This results in uncertainty as to which markets will benefit from these decisions, and which of them will lose as a result.

The result is that the yield curves in the EU have become steeper and more irregular, although the asset purchase program carried out by the European Central Bank causes the expected risk premium to remain relatively low.

The reason for the constant sudden increases in the valuation of risk premium is obviously also the low profitability of the financial sector in an environment of historically low interest rates. Additionally, banks are struggling with poor asset quality, a high level of non-performing loans, and high cost of penalties for legal violations. Their balance sheets are still excessively bloated, and the institutions are not able to come up with credible strategies for a return to long-term profitability. Confidence in the sector remains low despite the constant strengthening of the capital base.

Between the Q3’2015 and the Q4’2016 the net interest income of banks decreased by 6.9 per cent, net fee and commission income by 7 per cent, and net trading income by 7.4 per cent. Banks are trying to improve profitability primarily by increasing fee and commission income; however, they face strong competition of non-bank financial intermediaries, i.e. fintech companies.

The greatest risk for insurers is that long-term interest rates may not be enough to finance the rates of return contractually guaranteed to clients. In turn in the asset management industry the low return on assets translates directly into low rates of return on fund shares, which could potentially mean that the clients’ returns are devoured by the fees and the costs of distribution. In 2016 the flow of resources into funds across the EU only reached EUR300bn.

Such a situation encourages market participants to seek higher rates of return. The search for higher yield increases the risk of a drop in the prices of riskier asset classes. Such short-term responses in the prices of fixed-income instruments occurred at end of 2016, although they have not led to a sustainable diversification of prices.

On the one hand, a steeper yield curve and a change in its course provide an opportunity for financial institutions to improve profitability, but they are not a stabilizing factor. They mean that the risk of asset valuation may materialize again at any time.

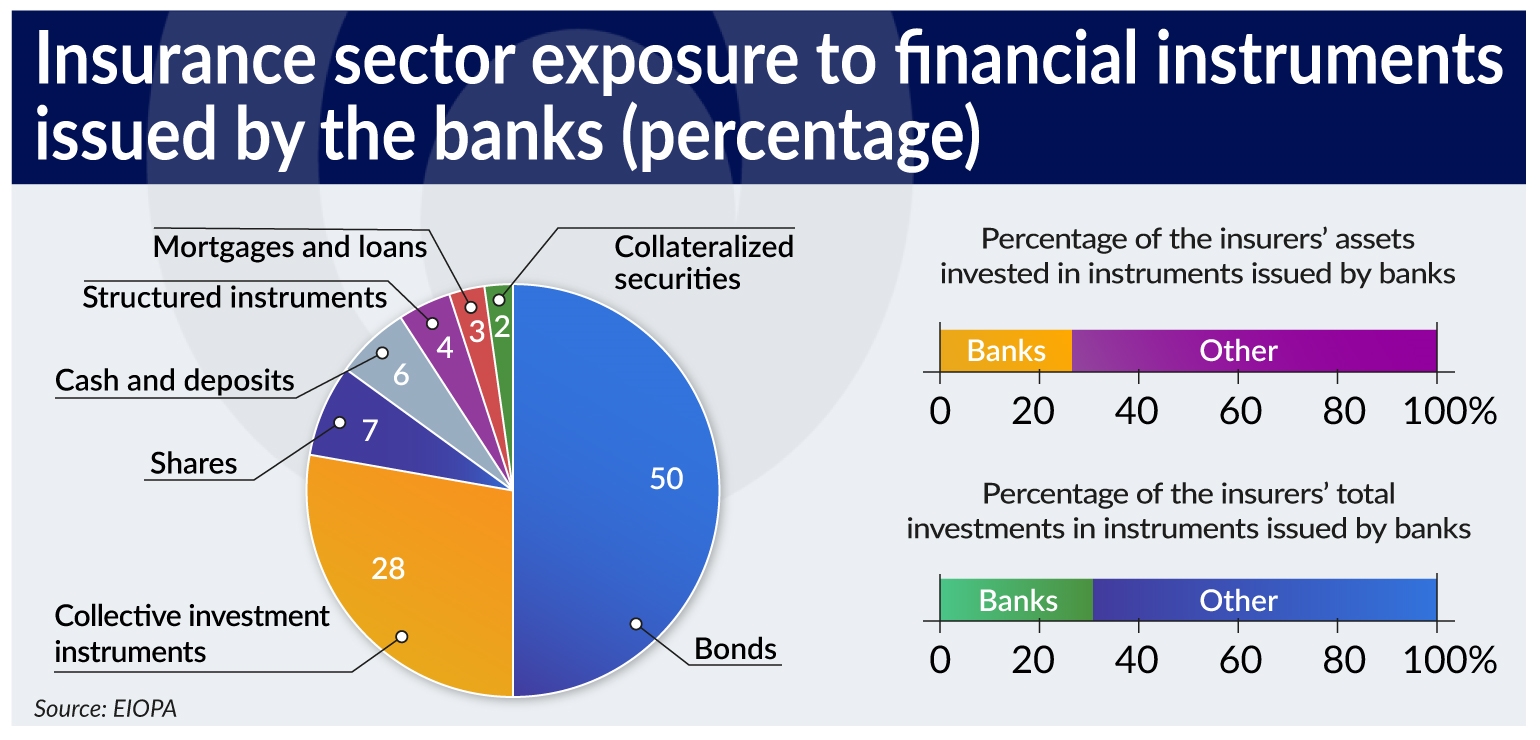

High interconnectedness increases the risk for the entire financial sector, in particular, through the decline in asset prices and direct exposures. The risk is concentrated commensurately in the insurance and the banking sector, as the insurers from the EU have high exposures to banks, and therefore a decline in the valuations of banks’ shares will cause a drop in the valuations of the insurers.

The low-quality of assets in many banks, and the risks associated with the conduct of business are additional challenges for financial institutions. The sector is increasingly exposed to risks associated with technology. Rapid changes in this area will over time significantly impact the business models of financial institutions. The banks’ central systems are aging, which forces them to make larger investments in the IT infrastructure, further aggravating profitability issues.

The risk associated with cybercrime threatens data integrity and business continuity in the entire system. The demand for cybersecurity is growing; however, the products that are to protect against attacks are still relatively new in the market, and have not been tested in practice. Addressing the problems related to cybersecurity will have a key impact on investor confidence in financial institutions and the ability of the sector to finance economic growth in the long term.

The full report is available here.