Tydzień w gospodarce

Category: RaportyPrzegląd wydarzeń gospodarczych ubiegłego tygodnia (16–20.05.2022) – źródło: dignitynews.eu

Economist, works at NBP, specialises in monetary policy issues and FX markets

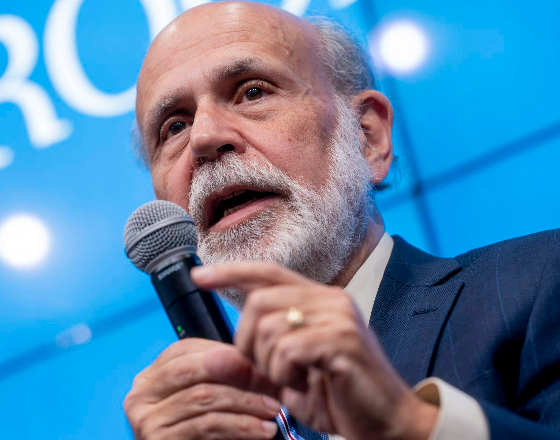

Ben Bernanke - Ex-Fed Chair, Nobel Prize winner

Many experts had already heard of Bernanke, when in February 2006 he took the helm of the largest central bank in the world. Others found out about him some three years later due to the launching of quantitative easing. However, Ben Bernanke had made a name for himself long before he became the head of the Fed, more than that – long before crossing the threshold of the American central bank. He had worked on his fame for many years in the charming and tradition-packed Princeton, less than 90km from New York. Probably at the end of the last century, in the privacy of his university office, after finishing classes with his students, he checked his paper and made the last corrections to it. It was on the Japanese economy and its author was very critical of the actions of the Japanese decision-makers. In those days many people loved to criticise Japan, but only Bernanke encouraged the authorities of this country to tackle deflation. Who knows whether the launching of quantitative easing by the Bank of Japan on 19 March 2001 would have been possible at all if it hadn’t been for his recommendations?

Ben Bernanke began working for the Fed in August 2002, when he became a member of the Board of Governors of the Federal Reserve System. It was just in time, because as early as May 2003 something happened that seemed incredible at the time. Suddenly, the Fed began worrying about inflation declining too quickly. Until then, banks (apart from the Japanese central bank) had usually been pleased with falling inflation. Although the threat of deflation in 2003 was averted in the USA, American decision-makers knew who to put their money on when it came to taking over after Alan Greenspan. Somewhat younger readers should be reminded that Greenspan left the Fed in a blaze of glory. Even his critics (including Alan Blinder, one of the Fed’s vice-chairs) did not hesitate to name him one of the greatest central bankers in history. Therefore, coming to grips with Greenspan’s legacy was a huge challenge requiring civil courage. Bernanke proved that he was the right man in the right place.

Maybe it was precisely the ability to face up to really big challenges that allowed Bernanke to tackle the biggest economic and financial crisis in almost 80 years. We don’t know whether Bernanke was aware when writing his paper that what he was preparing with the Japanese in mind would be tested on the domestic economy.

Not so long ago Bernanke dealt with yet another challenge, namely writing a good book. It should be stated right away that this is not a book about the crisis of 2008 – he already has such a book under his belt. Now Bernanke has made an attempt to present the last 80 years of the Fed’s policies, starting from 1951, when William McChesney Martin took over the helm of the central bank. In order to explain what the reviewed work offers us, it is worth recalling its full title: “21st Century Monetary Policy. The Federal Reserve from the Great Inflation to COVID-19”. It is my duty as a chronicler to add that the book was published on 17 May 2022 by the publishers W.W. Norton & Company.

The paperback version costs almost 140 zloty, but for those who count every penny (or grosz), an electronic version is available for just under 50 zloty. I made do with the latter and received about 500 pages of really interesting reading. However, is it possible to review a book written by a master of central banking? Is it appropriate to describe it as interesting? Still, the reviewer has to take some risks and write something more than just a recommendation to read the book.

Is it a book for every reader? I don’t think so. I would go so far as to say that it isn’t even a book for every economist. In order to understand and above all get some joy from reading it, you should be interested in monetary policy and be somewhat acquainted with recent economic history. The author has put a huge effort into writing it, so it’s no surprise that he expects from us at least a little intellectual effort while reading it. A minimum dose of knowledge on the mechanisms of monetary policy will certainly make it easier to overcome the complexities of interest rates and central bank balance sheets.

Bernanke writes eloquently, among other things, about how he failed to smuggle anything into current economic jargon. While it’s true that he elaborated the scientific basis of quantitative easing and then put it into practice, the very concept was created by someone else. It was similar with the operations carried out by the Fed in September 2011, which the market called operation Twist, referring to similar operations in the 1960s. Bernanke preferred to refer to them as MEP, or Maturity Extension Program. Nevertheless, the book leaves no doubts as to who deserves the copyright to what we today call quantitative easing. This is not due to the author’s lack of modesty – it was Bernanke who prepared the theoretical foundation and was fortunate to put his scientific achievements into practice.

The book focuses primarily on two issues: inflation and the broadly understood concept of the interest rate.

The book focuses primarily on two issues: inflation and the broadly understood concept of the interest rate. This explains why, despite focusing on 21st century monetary policy, Bernanke refers to events from the previous century. It would probably not be an exaggeration to define quantitative easing as striving for a guaranteed minimum (even necessary) dose of inflation for the economy. Chronic inflation was up to then characteristic of the second half of the 20th century (not to jinx things). Therefore, if we are looking for minimum inflation, it is necessary to take the trouble to get to know this phenomenon thoroughly. Of course, there’s a difference between necessary inflation and inflation running out of control. How can the latter be prevented? The answer is simple: it is necessary to learn its history.

Therefore, Bernanke describes the terms of office of two chairmen: William McChesney Martin and Arthur Burns, the latter born on Polish soil. It was particularly Burns who was criticised for losing control of inflation. Bernanke comments on whether this criticism is right. Along the way he describes perfectly the history of the Phillips curve and exceptionally clearly, concisely and convincingly explains the reasons for the disappearance of the dependence illustrated by it. The author’s great teaching abilities can be seen many times. Among other things, he explains very clearly why the well-known monetary aggregates (or rather their dynamics) hardly reacted at all to the quantitative easing that he introduced and why they took off during the pandemic.

Bernanke devotes a lot of space to interest rates. He explains, among others, what would have happened with long-term interest rates if it hadn’t been for rather loose fiscal policy. Moreover, he makes us aware (without referring to complex macroeconomic concepts) that during his chairmanship the potential for exerting impact via interest rates had simply run out. The staff of the Fed’s research units led by him calculated that if quantitative easing had not been implemented, the fed fund rate would have to have been lowered to… minus 6.5 per cent.

In the book, we will find answers to many interesting questions, for example, about what qualities a good central bank governor should have. It is worth reaching for this book to know the answer to this question. I can only reveal that in Bernanke’s opinion, a good central bank governor does not need to be a professor or even a doctor. The author stresses that the best central bank managers had no academic titles.

His vast academic experience was certainly helpful in writing such an interesting book. The author of course considers himself the creator of the solution called quantitative easing, but he does not hide his inspirations. Among them were the Roman emperor Tiberius, who also had to deal with financial panic. We also learn that an ardent advocate of quantitative easing in Japan was no other than Milton Friedman himself.

Bernanke does not shy away from difficult topics during his chairmanship. This concerns at least two issues. One of those was the bankruptcy of the Lehman Brothers bank. Why this bank, and not AIG, which was bailed out the next day? As it turns out, there were investors keen on taking over Lehman Brothers; however, one of them changed his mind under the influence of a decision taken in London. Another issue is the famous taper tantrum – in other words, the frenzy that was triggered by the Fed’s plans to reduce the scale of asset purchases. So could it have been possible to prepare the markets in a different way for the possible reduction in these purchases? Some believe that it is never so good that it cannot be better, and according to Bernanke, this statement is also true in his case.

Jak Stany Zjednoczone radziły sobie wcześniej z wysoką inflacją

The relationship between the Fed chairmen and the US presidents is also interesting. Much depends on the behaviour of the presidents – after all, they appoint the Fed chairmen. Moreover, as one may guess, the presidents can make the life of the Fed chairman very difficult. Of course, the best example is Donald Trump, who wanted to dismiss Jerome Powell, the current Chairman of the Fed, who Trump after all had appointed. Fortunately, Powell took no notice of these attacks and did his own thing, gaining with time not only the approval of Trump, but also the appreciation and sympathy of Bernanke. However, sometimes it is the central bank governors that get under the skin of the US presidents which, in the author’s opinion, is best evidenced by the complex relations between Alan Greenspan and George Bush senior.

In his book, Bernanke does not focus solely on monetary policy. A lot of space is devoted to whether the central bank should engage in activities promoting financial stability. He also touches on the question of the digital dollar or the broadly understood issue of the central bank digital currency in general. He also appreciates the importance of communication with the environment and this is why he spares no praise for Powell for launching the “Fed Listens” programme, providing information about how monetary policy impacts on the lives of citizens. According to Bernanke, it is precisely thanks to such activities that the bizarre situation which Alan Blinder pointed out in 1996 will not come about. The Vice Chair of the Fed heard that millions of US citizens associated the Federal Reserve System with an institution managing the forests, in which bears and bulls play in harmony, and on the horizon you could see hawks and doves flying by. In addition, the author devotes some space to the issue of the so-called social inclusion, expressing his regret that many racial minorities are still inadequately represented in the Fed.

He also appreciates the importance of communication with the environment and this is why he spares no praise for Powell for launching the “Fed Listens” programme, providing information about how monetary policy impacts on the lives of citizens.

I’m afraid that after reading the book, people who are interested in operational policy will be left wanting more. Bernanke belonged to the academic world and it is probably noticeable that this issue does not preoccupy him much. Of course, he mentions Paul Volcker’s reform of 6 October 1979 (by which the Fed referenced pure monetarism). However, I expected that the author would devote more space to such an important event. I had a similar feeling when reading the rather superficial (in my opinion) description of the events of September 2019 in the money markets in the USA. And yet, it was because of these events that the Fed had to return to the policy of quantitative easing when nobody had even heard of COVID-19 yet.

In his book, Bernanke defends very strongly the idea that the central bank should not focus on measures to ensure the financial stability of a given country. He has the right to do that, just as he has the right to criticise Sweden’s Riksbank for presenting a different view. However, the problem is that Bernanke focused only on the arguments of the former Deputy Governor of Riksbank, Lars Svensson, who is quite popular in the USA, and who resigned in protest after losing an intellectual battle with his immediate superior. I fell that Bernanke should also present the arguments of those who thought differently, above all, the Governor of Riksbank, Stefan Ingves. However, he failed to do so.

Finally, we come to the issue that perhaps I should have started this review with. Of course, Bernanke could not have foreseen the outbreak of war on our border, let alone estimate its impact on inflation. The author can speak of bad luck; however, for this reason his book loses a little freshness and even requires an urgent update. In many countries inflation has reached double digits and Bernanke’s deliberations on the measures aimed at guaranteeing a minimum level of inflation may even irritate some readers. However, perhaps it will encourage the author to update the book quickly, which would be beneficial for all of us. However, even without these changes the reader receives a truly great book written by an outstanding man. I stand by my opinion that it is not for everyone. For those who are interested in monetary policy I highly recommend it, and for those who conduct research into monetary policy it is a must-read which no specialist literature review can do without.

The author expresses his own opinions and not the official position of NBP.