We are not facing another crisis yet, and wise policy could prevent it from occurring. In its latest World Economic Outlook, the IMF raised the global GDP growth forecasts for this year to 3.6 per cent, and for the next year to 3.7 per cent, in both cases by 0.1 percentage point above the previous forecasts and well above the 2016 level of 3.2 per cent.

The recovery is gaining momentum, estimates the IMF. This year it is taking place in the highly developed economies, and in the next year it will trickle down to emerging markets and developing countries. This fuels the hope that growth will consolidate and will set the conditions for the normalization of monetary policy.

“While waters seem calm, vulnerabilities are building under the surface. If left unattended, these could derail the global recovery, putting growth at risk,” said Tobias Adrian, the main editor of the Global Financial Stability Report (GFSR), during a press conference in Washington dedicated to the presentation of the report.

Risks to medium-term growth are appearing. In the latest GFSR , the IMF emphasizes that some of the factors that have resulted in improved financial stability could in the medium term pose a threat to growth, if appropriate political actions are not taken in order to remedy the growing difficulties. The normalization of monetary policy could act as a catalyst for the threats. That is why this process should be subtle and balanced.

Risks to growth

Thanks to the unconventional monetary policy, the financial environment has evolved in a favorable way since the crisis. The entire global financial system is far more secure now. The global systemically important banks (there are 30 such entities) raised their capital and are attempting to adapt their business models to the regulatory and market changes. Capital flows are once again supplying the emerging markets, and the financing costs are low – all of this is conducive to economic growth, which is spreading to an increasing number of economies – it is already recorded in 75 per cent of the world. The risks are low in the short term, probably at the lowest level since the crisis.

This is the effect of the regulators’ activities to strengthen the financial system and of the accommodative monetary policy. This policy also has other effects, however. One of them is the increase in asset valuations and growth in financial leverage. The stronger banks pose less of a threat to financial stability, but the risk has moved from their balance sheets into two sectors – shadow banking and the markets. Market risk is increasing.

The unconventional monetary policy and quantitative easing have led to a situation in which there is too much money and not enough assets available. Currently, less than 5 per cent of the investment grade bonds (i.e. USD1.8 trillion) have a profitability rate higher than 4 per cent. Before the crisis 80 per cent (USD15.8bn) had profitability higher than 4 per cent. Credit spreads are near the lowest levels in history in spite of the deteriorating health of corporate balance sheets.

The valuations of assets are going up, as investors are accepting higher credit and liquidity risk in the search for higher yield. The usual high-risk players present on various asset markets are being closely followed by institutional investors. In 2017, approx. USD300bn of portfolio investment will flow to the emerging economies. This is over twice as much as in the previous two years combined. In addition, the markets’ vigilance is dulled and the volatility in individual asset classes is small, as if investors believe that prices will always be resistant to shocks.

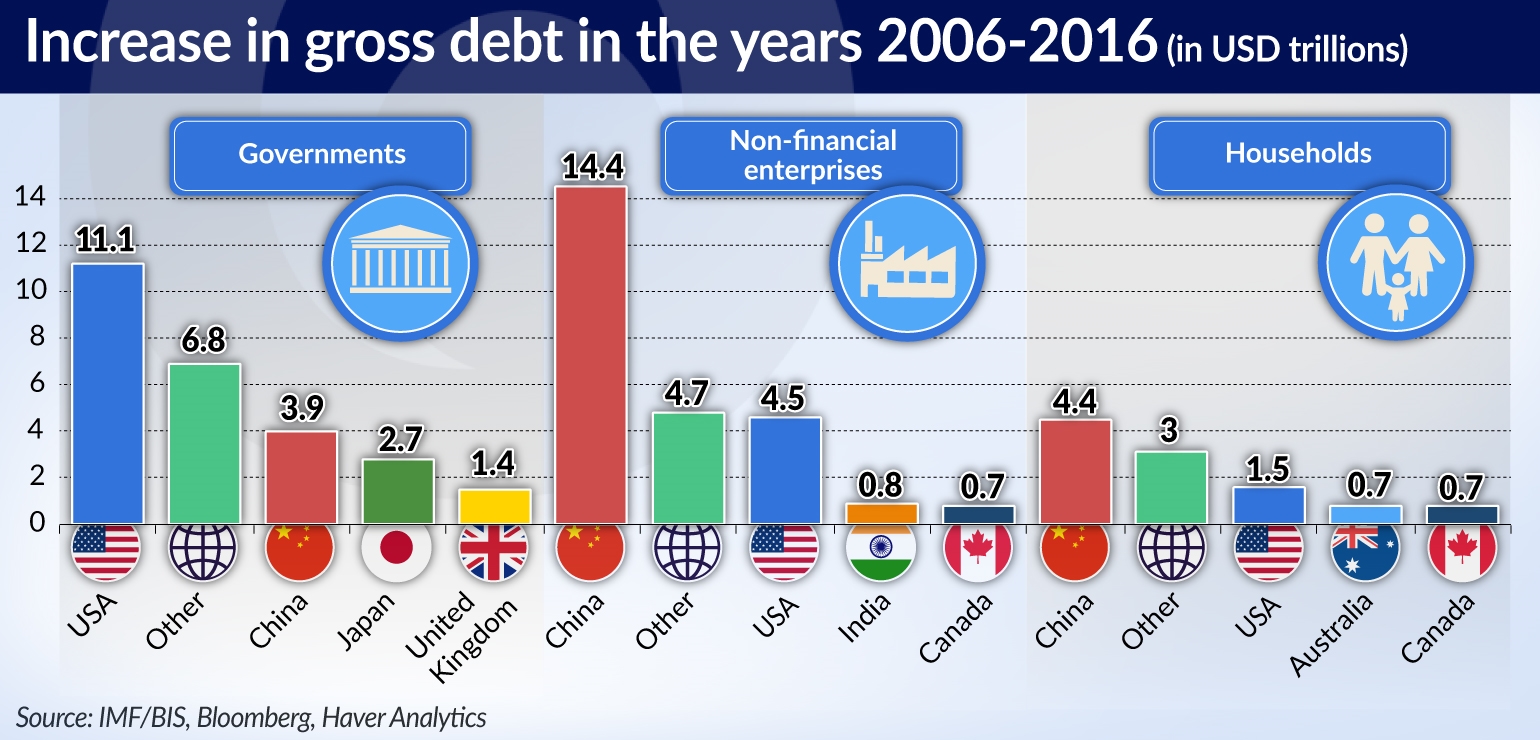

At the same time, the debt of the world’s largest economies has increased. Taking into consideration only the G20 states, the leverage in their entire non-financial sector is now higher than before the crisis. Even now, amid the lowest interest rates in the history of many countries, in numerous sectors the ability of the weaker borrowers to service their debt is decreasing. This applies to such large economies as Australia, Canada, China and South Korea. Their vulnerability to the deterioration of financial conditions is already high.

„Leverage in the private sector is now higher than prior to the financial crisis,” said Tobias Adrian.

China poses a special and perhaps most complex problem. Despite growth stabilizing at lower levels and the tightening of credit policy, the sheer size, complexity and the growth rate of the Chinese financial sector – and especially the non-bank financial sector – entails high risks for financial stability.

The assets of the local banking sector already amount to 310 per cent of GDP, compared with 240 per cent of GDP at the end of 2012. The banking sector is becoming intertwined with the shadow banking sector, with the two providing each other with mutual short-term wholesale funding, while corporations and enterprises are borrowing from both sectors. To what extent can the policy towards the financial sector be tightened without slowing down growth? In this case the line is difficult to draw.

No time for complacency

Household debt poses a separate risk for the sustainability of growth. There are big differences around the world in this respect. During the period of the global crisis, there was a pause in the growth of debt; however, in the last decade the trend has still been rising.

In developed countries, the ratio of household debt to GDP increased from 35 per cent in 1980 to approx. 65 per cent in 2016, and has been growing steadily since the crisis, albeit at a slightly lower pace. While in emerging economies the debt-to-GDP ratio itself is much lower – approx. 20 per cent – its growth rate has also been very high since the crisis. This ratio increased from about 5 per cent of GDP back in 1995. We should add that in Poland household debt (in the banking sector alone) amounted to approx. 35 per cent of GDP at the end of last year.

In the short term, the increase in household debt stimulates consumption, and therefore leads to accelerated GDP growth. In the medium term, however, it creates risks for macroeconomic and financial stability. It causes growth to slow down, reduces consumption and employment, and increases the risk of banking crises – diagnoses the IMF.

Among banks of global significance, one-third, representing total assets of USD17 trillion, are still struggling to achieve sustainable profitability.

If there was any change in the perception of risk, that would lead to a further development: a significant increase in the cost of credit, a decline in asset prices, and the withdrawal of capital from the emerging markets. Another crisis would take place. It wouldn’t be as powerful as the last one. It would have one-third of the strength of the previous one. Global GDP would rise at a rate 1.7 percentage points slower than the IMF baseline forecast.

A crisis would hurt the emerging economies the most. The IMF estimates that approx. USD100bn would flow out from these countries within four quarters. The deterioration of credit conditions would create a threat for the banks – especially those with weak capital and those that have the largest exposures to corporate loans and mortgages.

How to avoid another crisis

What to do in order to avoid the dark scenario? The list of tasks is very long. The largest central banks should not rush with the normalization of monetary policy. The process of winding down the balance sheet should be very gradual, smooth, well-considered, well communicated, and should be spread out over several years. Apart from the impact on the markets’ risk assessment, an excessively rapid normalization would remove the stimulus for output growth and the still-desired increase in core inflation.

However, if monetary policy is to remain accommodative for a longer period of time in order to sustain the global recovery, policymakers will have to face some challenges. They have to ensure that the financial system is stable and prevent unrest in the markets. The IMF believes that macro-prudential policy should be introduced universally, and that its tools should be enhanced to ensure that the supervisory bodies have the ability to limit leverage and to intervene in those segments of the market where bubbles are forming. The supervisory institutions have to keep a close eye on the largest banks, because some of them still have trouble with changing their business models.

The IMF calls for the completion of the reform of the banking system and the implementation of the post-crisis banking regulation (Basel III) on a global scale. We know that this includes, among others, the introduction of comparability between the standard risk weights and those derived from the internal rating methods, which was proposed by the Basel Committee on Banking Supervision. The latter method is applied by the largest banks in the world.

The IMF believes that in the case of banks with more risky borrowers, capital requirements should be even higher, and that banks should be encouraged to lend to less risky sectors. Meanwhile, the stress tests conducted by the supervisory bodies should assume greater shocks in the assets markets.

Banking regulations should be introduced and should be adhered to on a global scale, just like the coordination of the struggle against cybercrime. It is necessary to strengthen the regulations of the shadow banking sector in order to prevent risk migration and excessive financing from the capital market.

Emerging countries should take advantage of the good financing conditions, not in order to increase leverage, but to eliminate imbalances and improve their competitive position, which will increase their resilience to the possible outflow of capital associated with the normalization of monetary policy. They should also attempt to reduce leverage in the private sector and improve the management of external public debt. Meanwhile, Chinese policymakers should strive to strengthen the financial system, introduce reforms aimed at making economic growth less dependent on rapid expansion of credit, and should in particular restrict the lending activity of the shadow banking sector.

Take advantage of the opportunities provided by the recovery

The long list of recommendations included in the GFRS is not complete. Christine Lagarde, the Managing Director of the IMF, added a few more points. The accelerating growth of the global economy creates opportunities which should be used. Growth should be expanded in order to include those who are not yet benefiting. At a news conference she said that the legacy of the financial crisis is the stagnation of wages, limited employment opportunities, and technological exclusion.

Structural reforms are easier to pursue when the economy is strong, and such reforms are necessary for the growth to be more sustainable. The three priorities that should guide the governments are a return to the fundamental principles of the economy, more decisive tackling of the issue of excessive inequality, and ensuring bright prospects for the young generations.

“We must not waste this opportunity,” said Christine Lagarde.

Growth also means an opportunity for fiscal reforms and implementation of strategies that reduce high debt levels. In addition, we need reforms that can boost productivity and potential output. Labor and product market reforms are more potent during economic upswings.

Excessive inequality hinders growth, erodes trust, and fuels political tensions. Although poverty and inequality between countries has been falling over the past generation, income and wealth inequality within countries has been rising. Investments in human capital are of key importance and must include health care, education, lifelong learning, creating a social safety net, improving the fiscal tools and increasing the employment of women.

“Our research shows, for example, that some advanced economies could raise their top tax rates without slowing growth, which would provide resources for priority needs or debt reduction”, said Christie Lagarde.

Corruption costs more than USD1.5 trillion per year, nearly 2 per cent of global GDP. Our analysis shows that moving from high to low perceived corruption levels can increase public investment efficiency by 50 per cent and raise real per capita product by nearly one percentage point. Corruption is unacceptable, just like money laundering and the financing of terrorism. It is a threat for every economy.

The last, but not least important challenge is climate change, which disproportionately affects low-income countries. IMF studies show a relationship between temperature increases in tropical countries and a decline in GDP. The Fund calls for the elimination of subsidies for energy production associated with carbon dioxide emissions.