Jan Frait: When no one sees the risks they are greatest

Iwould be cautious in declaring victory over inflation and at the same time a bright economic outlook. There is a really long delay between monetary policy measures and their effects, says Jan Frait, Deputy Governor of the Czech National Bank.

Obserwator Finansowy: Let’s start with the state of the global economy. When the Fed started raising interest rates, recession was widely feared. Now that the US interest rate is around 5 per cent, everyone is talking about a ‚soft landing’. Is such a thing really possible?

Jan Frait: Sure, soft landing is possible, but there is not a big case for overoptimism in the global economy. What we see, given the last few years, is that there is a really big lag between monetary policy actions and subsequent effects. So I am still concerned that concerted tightening by nearly all central banks in the advanced economies could have significant effects on the financial sector, financial stability and then on economic developments with some considerable lag. So I would be very cautious in declaring victory over inflation and at the same time bright economic prospects. Let us be very careful.

I also remember a sentence you quoted during the lecture on the instability paradox: “the system is often the most vulnerable when it looks the most robust”. What is this mechanism really about?

I am in the central banking community for a long time and, in particular, before the global financial crisis, between 2005 and 2007 everyone thought that we are in the middle of fantastic economic periods without any risk being generated and that we are moving to some kind of bright future. And on the surface it was right like this but in reality, in a latent way we generated sources of vulnerability and then some event came with a shock and we out of a sudden moved into a long-term deep crisis. So once people think that everything is fine and there are no risks, it is usually the situation when we are setting on a way to a major problem. So once you start definitely ignoring risks and once you start to calculate risks, this is the problem of the paradox of financial instability.

Is Central and Eastern Europe more influenced by Fed or ECB decisions?

Our models we use in central banks usually assume that the dominant force behind our cycles from the external part, monetary conditions, is the interest rates in the euro area and the ECB’s monetary policy. Nevertheless, if we look at the data from recent years, we can see global flows associated with the US Fed moves and with changes in the long-term interest rates in the US because they attract capital from emerging markets and from other regions. So, besides looking at the European interest rates, I do look out at the US interest rates. I think these are very important.

For our region, the German economy is also quite important. Is a recovery in Germany the only thing we can count on? Or can we imagine a different economic model than being a supplier to Europe’s largest economy?

The Czech Republic is very much dependent on the German economy. Actually, our economic model built over the years was very successful because the German economy was successful. But also if you concentrate your economy on one card you can be also exposed to this concentration risk. Germany now looks not as an economy in a very good shape, but we should not forget that the Czechs and the Germans have one thing in common ─ they tend to switch between excessive optimism and excessive pessimism. So I think currently we are in the face of very high pessimism but after a while people will realise that maybe they went too far and the economies are able to adjust to restructuring. So, with a certain lag we will go up again, but it can take some time.

How can we accelerate convergence, the process of catching up with Western Europe?

I think each country in Central Europe has different problems or, maybe, different positives. One of the most important things is to improve coordination between the private and public sectors and trying to learn how to agree on things, not to disagree. We have a serious and clearly visible problem in front of us, and that is the housing situation. We need to improve housing and the availability of housing because we need to attract people from outside to work in our countries. And this is quite an urgent need.

Most political forces declare that the legislation required on the road to the euro is their priority. “I expect that after the elections on 2 April, the parliament will quickly amend the four laws we still lack,' says Iliya Lingorski, a member of the board of directors of the Bulgarian National Bank.

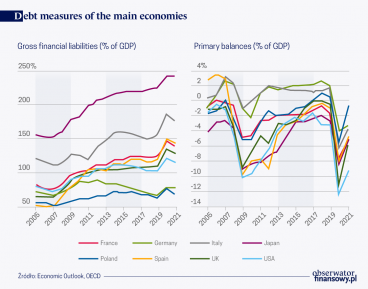

For well over a decade, governments in the developed countries have been borrowing at very low interest rates, sometimes even at negative rates. This is going to end, and probably for a long while.

Ukrainians have already started to think about development and how to reconstruct the country after the war – says Sergiy Nikolaychuk, Vice President, National Bank of Ukraine.