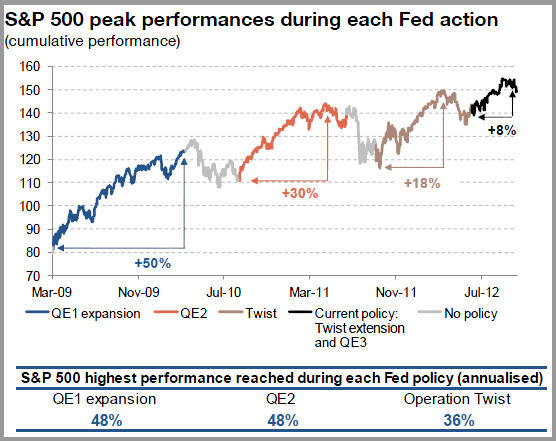

This Great Graphic comes from Zero Hedge, who got it from SocGen It purports to depict the performance of the S&P 500 and concludes that QE is generating diminishing returns.

Although our eyes can deceive us, we shouldn’t let it confuse our thinking. There is a logic fallacy embedded in here: post hoc ergo propter hoc. Just because something happened before some else does not mean it caused it.

The stock market rally during the period of QE1 is flattered by the end of the sharp downturn following the Lehman debacle. The poor performance noted under Operation Twist also corresponds to weaker earnings and concerns about the looming debt ceiling and fiscal cliff.

Moreover, we know that because the S&P 500 is weighted by market capitalization, the role of Apple has single-handily boosted the index. The Federal Reserve’s monetary policy cannot explain the stellar performance of Apple. Since March 2009, the start of QE1, the S&P 500 has risen almost 122% to the mid-September high. Apple shares have rallied over 800% in the same period.

Similarly, the poorer stock market performance of late is partly a function of a 16% slide in Apple over the past month. In addition, corporate earnings more broadly, and the future guidance provided, was the weakest since 2009.

It does not seem right or fair to reduce the S&P 500 to a function of US monetary policy. Does not the ebb and flow of the European debt crisis impact the investment climate? The reduction of the immediate tail risk,s first by the LTROs and then by OMT, helped shape the investment climate, no?

By focusing on the start and finish of the Fed’s balance sheet operations, the chart glosses over two other important considerations. First and foremost, the markets are anticipatory in nature and the Fed has telegraphed its intentions, especially after QE1. For example, the record will show the Bernanke tipped his hand at the Jackson Hole confab in Aug 2010 that a new round of asset purchases was likely and underscore that point at the following month’s FOMC meeting. Likewise the market knows when the program ends and this anticipation may also change behavior.

Second, it assumes that it is the purchases of new securities that is important. The Federal Reserve and many private sector economists argue that to the contrary, it is the stock not flows that is the key to the unorthodox monetary policy.

Lastly, the data does not bear out the conclusion. As measured by Soc Gen, the S&P 500 rally from low to high was essentially the same for QE1 and QE2. Operation Twist, arguably is not as strong as outright purchases (QE) and its impact on the market is a bit less, though in fairness it has not been completed, but the effects may be distorted by concurrently buying more Treasuries outright as well.

"If the auto industry collapses, Germany will collapse," writes Gabo Steingart emphatically in a recent article in Focus magazine. Many experts and commentators are increasingly drawing attention to the waning strength of Germany's flagship industry. German automotive has missed the electric age. Is it just a slightly longer pit-stop or is it irretrievably losing "pole position"?

Czołowe globalne korporacje takie, jak Apple, Microsoft czy Amazon odgrywają niezwykle istotną rolę we współczesnym świecie. Niejednokrotnie stają się one bogatsze i potężniejsze niż państwa narodowe. Odgrywają także większą rolę w codziennym życiu i w naszych umysłach.

Oczekiwaniom inflacyjnym gospodarstw domowych zazwyczaj nie poświęca się zbytniej uwagi przy monitorowaniu i prognozowaniu inflacji, częściowo dlatego, że wykazano, iż mediana ich oczekiwań ma mniejszą moc predykcyjną niż oczekiwania innych podmiotów. Niniejszy artykuł ma na celu dowieść, że zmiany w rozkładzie oczekiwań inflacyjnych gospodarstw domowych są istotne dla prognozowania inflacji w najbliższym czasie i oferują dodatkowe informacje w porównaniu z miernikami rynkowymi i oczekiwaniami prognostów. Sugeruje to, że oczekiwania inflacyjne gospodarstw domowych powinny odgrywać większą rolę w monitorowaniu inflacji, a w konsekwencji w kształtowaniu polityki pieniężnej.

Gotówka to wolność? A może zbędny, trącący myszką, relikt? Jak przekonuje Brett Scott w książce „Cloudmoney”, to jeden z niezbędnych aspektów niezależności w wymiarze społecznym i indywidualnym.

W przełomowym ruchu członkowie NATO poparli nowy narodowy wskaźnik wydatków: 5 proc. PKB na wojsko. W przeszłości do takiego zobowiązania nawoływał m.in. prezydent RP Andrzej Duda, ale decydujący był sygnał nadany przez prezydenta USA Donalda Trumpa.

Zimbabwe jest krajem o wyjątkowo turbulentnej historii monetarnej. Pokazuje ona między innymi, do czego może doprowadzić brak niezależności banku centralnego.

Rewolucja Generatywnej Sztucznej Inteligencji (GenAI) obiecuje skokowy wzrost globalnej produktywności, którego skala jest porównywalna jedynie z epoką elektryfikacji. Historyczne analizy wskazują jednak, że obecna trajektoria innowacji może wprowadzić rynek pracy w pułapkę technologiczną.

Problem dostępności mieszkań, które swoimi cechami, przede wszystkim standardem technicznym i wielkością odpowiadają potrzebom gospodarstw domowych nie ma prostego wyrazu statystycznego. Samo przeliczanie zasobu mieszkaniowego na populację nie obrazuje poziomu (nie)zaspokojenia potrzeb.

Unia Europejska coraz bardziej zacieśnia relacje polityczne, gospodarcze i handlowe z Republiką Mołdawii – jednym z najmłodszych państw Starego Kontynentu, które Rosja uznaje za swoją strefę wpływów.

Na październikowym posiedzeniu Rada Polityki Pieniężnej (RPP) obniżyła stopy procentowe NBP o 0,25 pkt. proc. w tym referencyjną do 4,50 proc. Co dalej? „Członkowie Rady widzą przestrzeń do obniżek, ale kiedy to nastąpi jeszcze nie wiedzą” - poinformował prof. Adam Glapiński.

Nie istnieje jedna ponadczasowa i prawdziwa historia o inflacji; ceny potrafią rosnąć z różnych powodów, a podnoszenie stóp procentowych to nie jedyne remedium – o czym starają się przekonywać Mark McGann Blyth i Nicolo Fraccaroli w „Inflation: A Guide for Users and Losers”.

Czy ludzkość nauczy się kontrolować ogień gwiazd? Fuzja termojądrowa, choć wciąż odległa, może fundamentalnie zmienić globalny paradygmat energetyczny i geopolityczny. O tym, dlaczego fizyka jądrowa to coś więcej niż technologia, opowiada prof. Michał Kowal z Narodowego Centrum Badań Jądrowych.

Polska chce zablokować umowę o wolnym handlu z krajami Ameryki Południowej. Powodem są głównie obawy rolników o konkurencyjność ich produktów. W jaki sposób realizacja umowy z Mercosur może wpłynąć na unijne rolnictwo i jakie mogą być też jej inne skutki?

Czy Polska rzeczywiście dokonała gospodarczego cudu? Ostatnie trzy i pół dekady pokazują, że odpowiedź może być tylko jedna – tak. Nowy numer kwartalnika „Obserwator Finansowy” to opowieść o sukcesie, który nie wydarzył się w naszej gospodarce sam, ale był efektem odwagi, determinacji i pracy całego społeczeństwa. A także o wyzwaniach, które dopiero przed nami.

Rosnące napięcia geopolityczne, demontaż globalnych łańcuchów dostaw, protekcjonizm, wojny handlowe i ekspansja sztucznej inteligencji coraz mocniej kształtują nowy, wielobiegunowy ład gospodarczy. Najnowszy numer kwartalnika Narodowego Banku Polskiego stawia pytania o przyszłość światowej gospodarki.