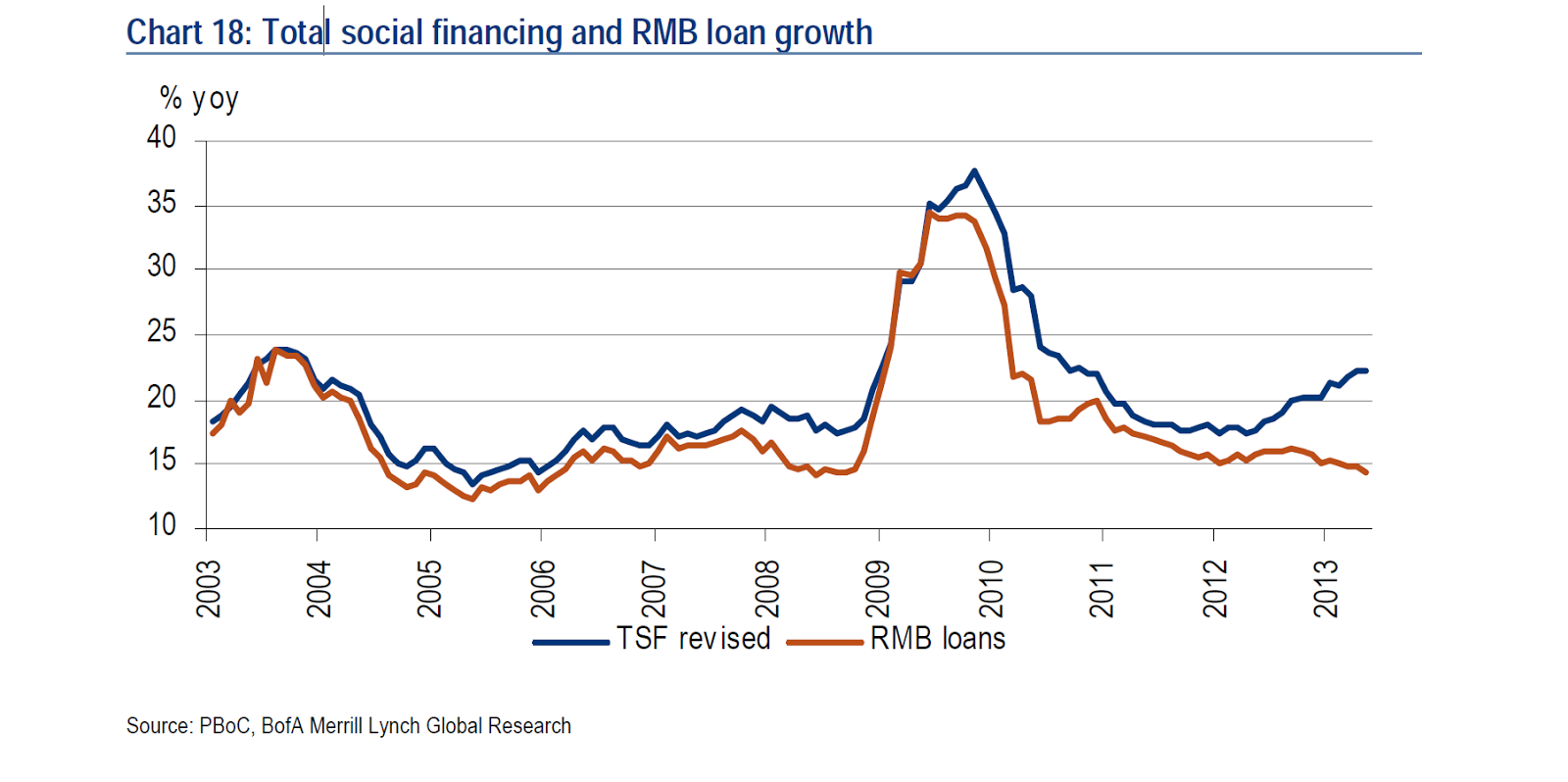

This Great Graphic was posted on the Financial Times’ new news delivery service called fastFT. It in turn picked it up from BofA Merrill Lynch, who drew on data from the China’s central bank.

The orange-ish line are the yuan loans made by China’s banks. The blue line a broader measure. It depicts what China officials call „social financing”, which, in addition to bank loans, it includes the fund raising of other financial and non-financial firms, as well as households. The measure was introduced by the PBOC in 2011, so the economists that put the chart together must of projected the social financing prior for the earlier period.

Chinese officials devised this tool to help it monitor the financial system evolved away from state-centric lending. This broad measure of credit activity. It is the total funds in the real economy generated by the financial system.

The gap between to two lines is the growing role of non-bank actors in the financial system This has been dubbed „shadow banking”. It is a nice moniker, but it is not very telling. It is simply the non-bank part of the financial system, which itself may be a function of the increasing complexity of the system. It is the dis-intermediation of banks.

Chinese officials do not have as much direct control over the shadow banking sector as they do the banking sector proper. Officials were able to slow bank lending, as they desired. However, credit creation in the shadow banking system was unchecked. The liquidity squeeze that has seen rates rise sharply in China, and while they might not be rising further, remain at elevated levels, is partly meant or tolerated to rein in the non-banking part of the financial system.

The falsified exports to conceal capital flows and practices around wealth management products were different, but similar ways to game and circumvent the system. Officials, in part, lost some control. The sale-and-buy-back scheme, that was banned last month, was one of the ways in which smaller financial institutions dealt with the inherent maturity mismatch in wealth management products that were attractive offered higher interest rates than deposits.

Around 85% of the wealth management products mature 6 months or less. To get a higher yield the proceeds were invested in bonds. This is the maturity mismatch and the sale-and-buy-back scheme that was used to manage this is no longer available. Part of the increase interest rates in China may reflect the sales of those bonds in an illiquid market.

"If the auto industry collapses, Germany will collapse," writes Gabo Steingart emphatically in a recent article in Focus magazine. Many experts and commentators are increasingly drawing attention to the waning strength of Germany's flagship industry. German automotive has missed the electric age. Is it just a slightly longer pit-stop or is it irretrievably losing "pole position"?

Definiując pojęcie kompetencji finansowych (financial literacy), warto odwołać się do podejścia zaproponowanego przez Organizację Współpracy Gospodarczej i Rozwoju (OECD). Jest ono bowiem na świecie powszechnie akceptowane i wykorzystywane w badaniach. Przez kompetencje finansowe należy rozumieć „kombinację świadomości, wiedzy, umiejętności, postaw i zachowań niezbędnych do podejmowania skutecznych decyzji finansowych i ostatecznego osiągania indywidualnego dobrobytu finansowego” (OECD/INFE Guidance on digital delivery of financial education, OECD 2022). Nawet z bardzo pobieżnej analizy tej definicji widać, że pojęcie kompetencji finansowych jest wielowątkowe i zawiera kilka wzajemnie uzupełniających się komponentów.

Początki australijskiej bankowości wiążą się z przybyciem, do ówczesnej kolonii karnej znanej jako Nowa Południowa Walia, w 1810 r. gubernatora Lachlana Macquarie. Została ona założona na terenach dzisiejszej południowo-wschodniej Australii. Macquarie, dziś uznawany za jedną z kluczowych postaci w historii tego kraju, odegrał istotną rolę w przekształceniu tej bardzo odległej od Europy i ponurej kolonii karnej w kraj wolnych ludzi.

Gotówka to wolność? A może zbędny, trącący myszką, relikt? Jak przekonuje Brett Scott w książce „Cloudmoney”, to jeden z niezbędnych aspektów niezależności w wymiarze społecznym i indywidualnym.

W przełomowym ruchu członkowie NATO poparli nowy narodowy wskaźnik wydatków: 5 proc. PKB na wojsko. W przeszłości do takiego zobowiązania nawoływał m.in. prezydent RP Andrzej Duda, ale decydujący był sygnał nadany przez prezydenta USA Donalda Trumpa.

Rewolucja Generatywnej Sztucznej Inteligencji (GenAI) obiecuje skokowy wzrost globalnej produktywności, którego skala jest porównywalna jedynie z epoką elektryfikacji. Historyczne analizy wskazują jednak, że obecna trajektoria innowacji może wprowadzić rynek pracy w pułapkę technologiczną.

Rosja od lat starannie przygotowywała swoją gospodarkę na czas konfrontacji z Zachodem. Sankcje, które zostały nałożone na nią po inwazji na Ukrainę, nie przyniosły spodziewanego rezultatu. Czy „forteca Rosja” jest odporna na presję i czy jest bliska samowystarczalności, jak chciałby tego Putin, czy może znajduje się już na krawędzi załamania?

Unia Europejska coraz bardziej zacieśnia relacje polityczne, gospodarcze i handlowe z Republiką Mołdawii – jednym z najmłodszych państw Starego Kontynentu, które Rosja uznaje za swoją strefę wpływów.

Na październikowym posiedzeniu Rada Polityki Pieniężnej (RPP) obniżyła stopy procentowe NBP o 0,25 pkt. proc. w tym referencyjną do 4,50 proc. Co dalej? „Członkowie Rady widzą przestrzeń do obniżek, ale kiedy to nastąpi jeszcze nie wiedzą” - poinformował prof. Adam Glapiński.

Nie istnieje jedna ponadczasowa i prawdziwa historia o inflacji; ceny potrafią rosnąć z różnych powodów, a podnoszenie stóp procentowych to nie jedyne remedium – o czym starają się przekonywać Mark McGann Blyth i Nicolo Fraccaroli w „Inflation: A Guide for Users and Losers”.

Czy ludzkość nauczy się kontrolować ogień gwiazd? Fuzja termojądrowa, choć wciąż odległa, może fundamentalnie zmienić globalny paradygmat energetyczny i geopolityczny. O tym, dlaczego fizyka jądrowa to coś więcej niż technologia, opowiada prof. Michał Kowal z Narodowego Centrum Badań Jądrowych.

Polska chce zablokować umowę o wolnym handlu z krajami Ameryki Południowej. Powodem są głównie obawy rolników o konkurencyjność ich produktów. W jaki sposób realizacja umowy z Mercosur może wpłynąć na unijne rolnictwo i jakie mogą być też jej inne skutki?

Czy Polska rzeczywiście dokonała gospodarczego cudu? Ostatnie trzy i pół dekady pokazują, że odpowiedź może być tylko jedna – tak. Nowy numer kwartalnika „Obserwator Finansowy” to opowieść o sukcesie, który nie wydarzył się w naszej gospodarce sam, ale był efektem odwagi, determinacji i pracy całego społeczeństwa. A także o wyzwaniach, które dopiero przed nami.

Rosnące napięcia geopolityczne, demontaż globalnych łańcuchów dostaw, protekcjonizm, wojny handlowe i ekspansja sztucznej inteligencji coraz mocniej kształtują nowy, wielobiegunowy ład gospodarczy. Najnowszy numer kwartalnika Narodowego Banku Polskiego stawia pytania o przyszłość światowej gospodarki.