The Stability and Growth Pact (SGP) is a good tool to stop sovereign European nations from becoming too indebted. Traditionally, Southern European countries were fiscally irresponsible, and Central European countries tried and tame that behaviour with the SGP.

Low interest rates resulted as a positive consequence: even though German rates were low due to the European Central Bank decreasing the Main Refinancing Rate (as a result of its control of inflation), spreads of PIGS countries with respect to the German benchmark also posted historical lows due to the newly engineered fiscal austerity.

However, we are facing what could represent the limits of the SGP: the Law of Unexpected Consequences. Or in other words: there can be too much of a good thing.

Currently we are experiencing the beginning of a double whammy: on one hand, monetary policy is starting to become contractionary. The European Central Bank is phasing out its extraordinary liquidity measures, and it will become to hike its Main Refinancing Rate beginning 2011. On the other hand, the SGP forces European countries to comply with a 3% deficit by 2013 by restricting their fiscal policy.

As a consequence, one can expect that these two contractionary forces will result in negative effects on the countries that are farther away from the constraints defined by the SGP.

One could ask, then, if the limits of the SGP could become too dangerous. To give an answer to this question, one would need to have good forecasting tools for GDP, and we do not have any. For example, the Spanish government expected, in 2008, that the Spanish economy would grow at around 3.5% in 2009. Instead, it ended up growing at -3.6% … more than a 7% error!

But we could check if current actions are leading towards reasonable outcomes. I want to present a piece of evidence showing than it could be that the SGP is forcing European countries to take on wrong and dangerous actions, just for the sake of complying with the SGP but devoid of a meaningful economic sense.

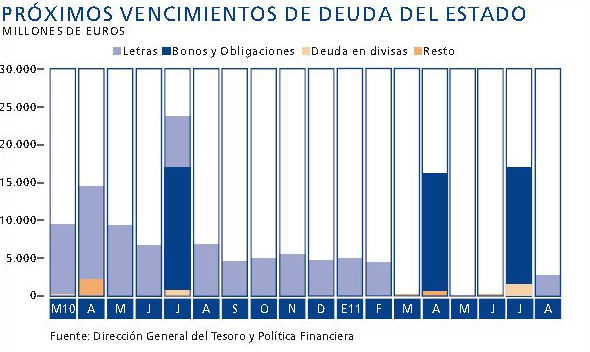

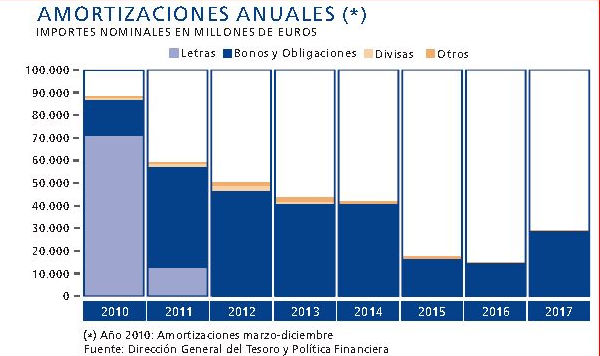

From the charts shown above, one can see that even though it is common for the Spanish Treasury to issue mainly long term bonds to finance Spanish public debts, in 2009 the Treasury issued mostly short term bonds for this task. Why was that? Why did the Spanish Treasury diverged from standard practice, both at the international level, and its own reasonable tradition of the past?

The reason is the interest rate curve was massively steep: short term bonds were yielding less than 1%, and long term bonds were at around 4%. As such, under the strong constraints of the SGP, one reasonable action was to switch from long term bonds to short term bonds, and save around 3% of financing costs.

However, this action leads to increased liquidity risk: the Spanish Treasury has to refinance the debt not in 10 or 30 years, but in one year. And if there are stresses in the world financial markets, this may become a game over for the country. In my opinion, it is better to control liquidity risk than to save one or two points of deficit.

To sum up: even though the SGP may be a reasonable measure under normal circumstances, it may be that it is becoming too stressful for Southern European countries suffering from both restrictive monetary and fiscal policies.

The Treaty of Versailles is another example of a highly constrained measure that even though it made sense originally, it created a worse problem than the one supposed to be solving.

"If the auto industry collapses, Germany will collapse," writes Gabo Steingart emphatically in a recent article in Focus magazine. Many experts and commentators are increasingly drawing attention to the waning strength of Germany's flagship industry. German automotive has missed the electric age. Is it just a slightly longer pit-stop or is it irretrievably losing "pole position"?

Pod względem innowacji Europa pozostaje w tyle. Niniejszy artykuł opisuje, w jaki sposób jej przemysł zdaje się tkwić w pułapce średniozaawansowanych technologii, która nie sprzyja opuszczaniu utartych ścieżek. Autorzy argumentują, że polityka innowacyjna UE powinna wspierać przełomowe innowacje, aby przełamać tę zależność, ale wymaga to głębokich reform, zarówno pod względem struktury, jak i finansowania.

Wydarzenia z marca 2023 r. w Stanach Zjednoczonych i Szwajcarii uwidoczniły – nie po raz pierwszy – utrzymującą się kruchość systemów bankowych. Autorzy najnowszego Raportu genewskiego na temat gospodarki światowej oceniają, czy dotychczasowe reformy wystarczą, aby stawić czoło zmianom otoczenia gospodarczego i postępującym przekształceniom strukturalnym oraz jakie dodatkowe reformy systemów bankowych mogą okazać się konieczne. Co prawda konkretne przyczyny słabości banków są różne w rozmaitych jurysdykcjach, ale wiele wniosków zawartych w raporcie dotyczy ogółu systemów bankowych.

Gotówka to wolność? A może zbędny, trącący myszką, relikt? Jak przekonuje Brett Scott w książce „Cloudmoney”, to jeden z niezbędnych aspektów niezależności w wymiarze społecznym i indywidualnym.

W przełomowym ruchu członkowie NATO poparli nowy narodowy wskaźnik wydatków: 5 proc. PKB na wojsko. W przeszłości do takiego zobowiązania nawoływał m.in. prezydent RP Andrzej Duda, ale decydujący był sygnał nadany przez prezydenta USA Donalda Trumpa.

Zimbabwe jest krajem o wyjątkowo turbulentnej historii monetarnej. Pokazuje ona między innymi, do czego może doprowadzić brak niezależności banku centralnego.

Rewolucja Generatywnej Sztucznej Inteligencji (GenAI) obiecuje skokowy wzrost globalnej produktywności, którego skala jest porównywalna jedynie z epoką elektryfikacji. Historyczne analizy wskazują jednak, że obecna trajektoria innowacji może wprowadzić rynek pracy w pułapkę technologiczną.

Problem dostępności mieszkań, które swoimi cechami, przede wszystkim standardem technicznym i wielkością odpowiadają potrzebom gospodarstw domowych nie ma prostego wyrazu statystycznego. Samo przeliczanie zasobu mieszkaniowego na populację nie obrazuje poziomu (nie)zaspokojenia potrzeb.

Unia Europejska coraz bardziej zacieśnia relacje polityczne, gospodarcze i handlowe z Republiką Mołdawii – jednym z najmłodszych państw Starego Kontynentu, które Rosja uznaje za swoją strefę wpływów.

Na październikowym posiedzeniu Rada Polityki Pieniężnej (RPP) obniżyła stopy procentowe NBP o 0,25 pkt. proc. w tym referencyjną do 4,50 proc. Co dalej? „Członkowie Rady widzą przestrzeń do obniżek, ale kiedy to nastąpi jeszcze nie wiedzą” - poinformował prof. Adam Glapiński.

Nie istnieje jedna ponadczasowa i prawdziwa historia o inflacji; ceny potrafią rosnąć z różnych powodów, a podnoszenie stóp procentowych to nie jedyne remedium – o czym starają się przekonywać Mark McGann Blyth i Nicolo Fraccaroli w „Inflation: A Guide for Users and Losers”.

Czy ludzkość nauczy się kontrolować ogień gwiazd? Fuzja termojądrowa, choć wciąż odległa, może fundamentalnie zmienić globalny paradygmat energetyczny i geopolityczny. O tym, dlaczego fizyka jądrowa to coś więcej niż technologia, opowiada prof. Michał Kowal z Narodowego Centrum Badań Jądrowych.

Polska chce zablokować umowę o wolnym handlu z krajami Ameryki Południowej. Powodem są głównie obawy rolników o konkurencyjność ich produktów. W jaki sposób realizacja umowy z Mercosur może wpłynąć na unijne rolnictwo i jakie mogą być też jej inne skutki?

Czy Polska rzeczywiście dokonała gospodarczego cudu? Ostatnie trzy i pół dekady pokazują, że odpowiedź może być tylko jedna – tak. Nowy numer kwartalnika „Obserwator Finansowy” to opowieść o sukcesie, który nie wydarzył się w naszej gospodarce sam, ale był efektem odwagi, determinacji i pracy całego społeczeństwa. A także o wyzwaniach, które dopiero przed nami.

Rosnące napięcia geopolityczne, demontaż globalnych łańcuchów dostaw, protekcjonizm, wojny handlowe i ekspansja sztucznej inteligencji coraz mocniej kształtują nowy, wielobiegunowy ład gospodarczy. Najnowszy numer kwartalnika Narodowego Banku Polskiego stawia pytania o przyszłość światowej gospodarki.