The Federal Reserve is suggesting that barring a deterioration of economy activity in the coming months, it is preparing a protracted exit from the extraordinary monetary policy pursued since the credit cycle ended. Talking about it is part of the Fed’s forward guidance and is also part of the exit strategy. Investors, both retail and institutional are adjusting their positions accordingly.

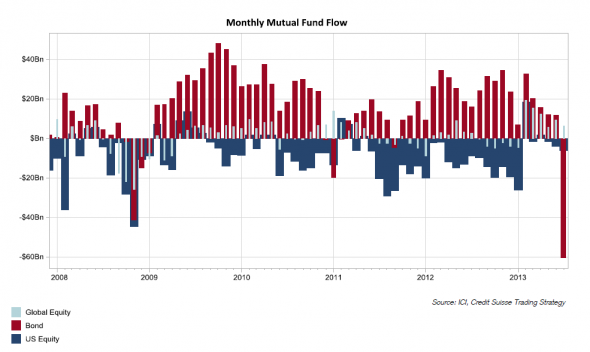

This Great Graphic was published on FT Alphaville, which in turn got them from Credit Suisse. The top chart tracks the flow of funds into three broad categories of mutual funds. The dark red bar is the flows into, and now out, of bond funds. The dark blue bar are the flows into/out of US equity funds. The light blue, (look closely) track the global equity funds. Roughly $60 bln has left the fixed income funds in June, apparently the most on record.

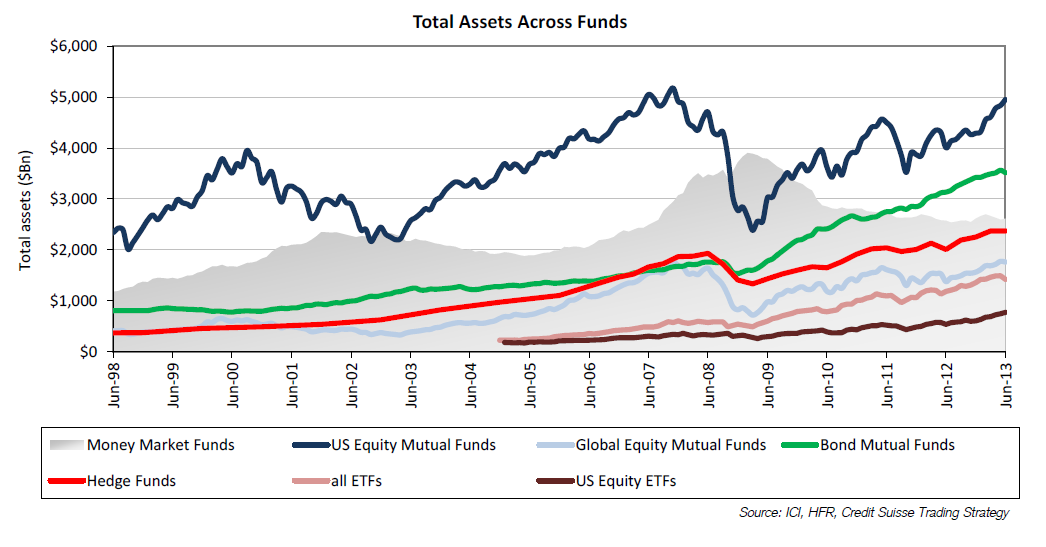

This has been represented in the popular and business press, but the second chart puts it in a larger context of the stock of investments that have accumulated in various investment vehicles since the late 1990s. For example, the green line, which tracks flows into bond mutual funds, shows that the stock of such investment is near $3.5 trillion. On the eve of the Lehman debacle, there was around $1.7 trillion under management by fixed income mutual funds. There is no compelling reason to think that there is a mean reversion process at work and all the funds that flowed into the bond funds will now flow out.

In addition, the bond mutual funds capture mostly retail interest. Institutional investors have also been selling fixed income We noted that Japanese investors, for example, have been significant sellers of foreign bonds this year and in May appear to have sold about $30 bln of US Treasury bonds and notes. We also know that the Fed’s custody holdings of Treasuries has fallen by about $26 bln from late May through early July.

Rosja przyjęła kolejny „wojenny” budżet na 2025 r. i lata 2026–2027. Wbrew wcześniejszym założeniom sytuacja się nie normalizuje, wydatki rosną w galopującym tempie, a deficyt narasta. Budżet nie jest w stanie wspierać innych sfer życia społeczno-gospodarczego decydujących o przyszłej pozycji Rosji, a jego stan pokazuje wymierne koszty wojny, te bieżące, jak również te, które będą obciążać rosyjską gospodarkę przez następnych wiele lat.

"If the auto industry collapses, Germany will collapse," writes Gabo Steingart emphatically in a recent article in Focus magazine. Many experts and commentators are increasingly drawing attention to the waning strength of Germany's flagship industry. German automotive has missed the electric age. Is it just a slightly longer pit-stop or is it irretrievably losing "pole position"?

Rosyjska gospodarka od przeszło pięciu kwartałów rośnie w tempie ponad 5 proc. To rekordowe tempo, ostatni raz odnotowywane na takim poziomie na przełomie lat 2011 i 2012. Czy Rosja, mimo sankcji, odcięcia od najnowszych technologii, inwestycji zagranicznych i wiodących światowych rynków eksportu oraz importu zaczyna osiągać to o czym od dawna mogła tylko marzyć? Czy też jest to wstęp do sagi „miłe złego początki”?

Gotówka to wolność? A może zbędny, trącący myszką, relikt? Jak przekonuje Brett Scott w książce „Cloudmoney”, to jeden z niezbędnych aspektów niezależności w wymiarze społecznym i indywidualnym.

W przełomowym ruchu członkowie NATO poparli nowy narodowy wskaźnik wydatków: 5 proc. PKB na wojsko. W przeszłości do takiego zobowiązania nawoływał m.in. prezydent RP Andrzej Duda, ale decydujący był sygnał nadany przez prezydenta USA Donalda Trumpa.

Rewolucja Generatywnej Sztucznej Inteligencji (GenAI) obiecuje skokowy wzrost globalnej produktywności, którego skala jest porównywalna jedynie z epoką elektryfikacji. Historyczne analizy wskazują jednak, że obecna trajektoria innowacji może wprowadzić rynek pracy w pułapkę technologiczną.

Rosja od lat starannie przygotowywała swoją gospodarkę na czas konfrontacji z Zachodem. Sankcje, które zostały nałożone na nią po inwazji na Ukrainę, nie przyniosły spodziewanego rezultatu. Czy „forteca Rosja” jest odporna na presję i czy jest bliska samowystarczalności, jak chciałby tego Putin, czy może znajduje się już na krawędzi załamania?

Unia Europejska coraz bardziej zacieśnia relacje polityczne, gospodarcze i handlowe z Republiką Mołdawii – jednym z najmłodszych państw Starego Kontynentu, które Rosja uznaje za swoją strefę wpływów.

Na październikowym posiedzeniu Rada Polityki Pieniężnej (RPP) obniżyła stopy procentowe NBP o 0,25 pkt. proc. w tym referencyjną do 4,50 proc. Co dalej? „Członkowie Rady widzą przestrzeń do obniżek, ale kiedy to nastąpi jeszcze nie wiedzą” - poinformował prof. Adam Glapiński.

Nie istnieje jedna ponadczasowa i prawdziwa historia o inflacji; ceny potrafią rosnąć z różnych powodów, a podnoszenie stóp procentowych to nie jedyne remedium – o czym starają się przekonywać Mark McGann Blyth i Nicolo Fraccaroli w „Inflation: A Guide for Users and Losers”.

Czy ludzkość nauczy się kontrolować ogień gwiazd? Fuzja termojądrowa, choć wciąż odległa, może fundamentalnie zmienić globalny paradygmat energetyczny i geopolityczny. O tym, dlaczego fizyka jądrowa to coś więcej niż technologia, opowiada prof. Michał Kowal z Narodowego Centrum Badań Jądrowych.

Polska chce zablokować umowę o wolnym handlu z krajami Ameryki Południowej. Powodem są głównie obawy rolników o konkurencyjność ich produktów. W jaki sposób realizacja umowy z Mercosur może wpłynąć na unijne rolnictwo i jakie mogą być też jej inne skutki?

Czy Polska rzeczywiście dokonała gospodarczego cudu? Ostatnie trzy i pół dekady pokazują, że odpowiedź może być tylko jedna – tak. Nowy numer kwartalnika „Obserwator Finansowy” to opowieść o sukcesie, który nie wydarzył się w naszej gospodarce sam, ale był efektem odwagi, determinacji i pracy całego społeczeństwa. A także o wyzwaniach, które dopiero przed nami.

Rosnące napięcia geopolityczne, demontaż globalnych łańcuchów dostaw, protekcjonizm, wojny handlowe i ekspansja sztucznej inteligencji coraz mocniej kształtują nowy, wielobiegunowy ład gospodarczy. Najnowszy numer kwartalnika Narodowego Banku Polskiego stawia pytania o przyszłość światowej gospodarki.