Tak sugeruje jeden z dobrze poinformowanych ekonomistów-analityków Vitaliy Katsenelson. Chiny mogą nie dać rady pociągnąć boksującej Unii Europejskiej. Według prof. Paula DeGrauve i Marginal Revolution UE nie pomogła sobie zamieniając w przypadku Irlandii dług prywatny na publiczny. Eurostrefa jest słabsza - sugeruje raport Legatum Institute. A Pragmatic Capitalism uważa, że mimo wszystko Niemcy nie opuszczą unii walutowej.

Wygląda na to, że debata na temat euro przybiera kształt podobny do tej, która poprzedziła utworzenie wspólnej unii walutowej. Coraz więcej publikacji dotyczy kwestii fundamentalnych związanych z eurostrefą.

Legatum Institute opublikował raport pt. „Can the Euro survive?”, w którym sugeruje, iż kraje PIIGS mogłyby szybciej wydźwignąć się z kryzysu, gdyby wyszły z unii walutowej. W innym wypadku zapowiadane przez Unię oszczędności budżetowe spowodują długotrwałą recesję.

A second area where extraordinarily large imbalances have emerged in Europe’s periphery has been in the housing markets of Ireland and Spain. Fuelled by easy access to global credit, as well as by the ECB whose one-size-fits-all interest rate policy kept interest rates too low for too long for Europe’s periphery, Ireland and Spain experienced housing bubbles that make that experienced in the United States pale. (…) The bursting of the housing bubbles in Ireland and Spain has been a primary driver in the dramatic deterioration in their public finances. It has also been the primary factor in the rise in unemployment in Ireland and Spain to their present levels of around 13 percent and 20 percent respectively.

Autorzy raportu twierdzą, że finanse krajów peryferyjnych (Grecji, Hiszpanii, Portugalii i Irlandii) są niemożliwe do naprawienia. Nie pomogą zapowiadane poprawki do traktatu ani zaostrzenie polityki fiskalnej eurostrefy. Ponadto ratyfikacja traktatu wymaga czasu, którego brakuje w czasie obecnego kryzysu.

While the treaty modifications now being proposed would have had great merit when the Euro was launched in January 1999, how relevant they are today at a time when the periphery’s public finances have been compromised beyond repair and when there is every indication that the periphery’s crisis is deepening is questionable. While the periphery’s sovereign debt crisis is playing out in real time, past experience would suggest that treaty modification, which requires unanimous ratification by all European Union members, will take years to effect. In addition, it would appear that the proposed reforms overlook the fact that the major part of the periphery’s budget deficits is primary in nature.

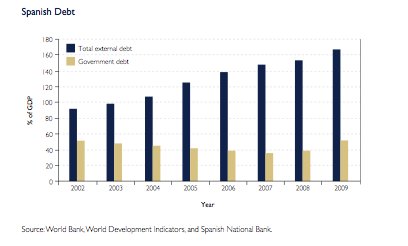

Nie pomoże też częściowa redukcja długu państw peryferii. W odróżnieniu od innych tego typu opracowań raport szczególnie zwraca uwagę na wpływ zadłużenia zewnętrznego. Wartość kredytów udzielonych deweloperom przez hiszpańskie (połączone nierozerwalnie z europejskim systemem bankowym) jest odpowiednikiem 45 proc. PKB tego kraju.

As such, even if the debt of the periphery were to be substantially written down, the periphery would still be left with very large budget deficits. And reducing these very large budget deficits to sustainable levels would still involve very deep recessions if such an exercise were attempted within the straitjacket of continued Euro membership.

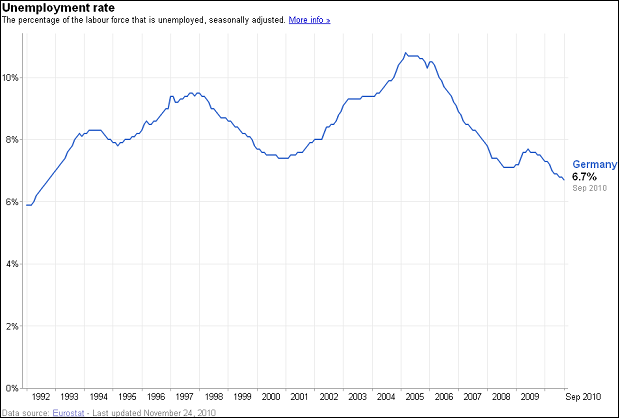

Mimo wszystkich problemów wbrew pogłoskom Niemcy raczej nie zechcą wycofać się z euro. Z wykresu można dowiedzieć się, że stopa bezrobocia w Niemczech wynosi około 6 proc. (i jest najniższa w Unii) i że wciąż spada.

Pragmatic Capitalism przekonuje, że to właśnie niemieckie banki (bezpośrednio lub pośrednio) są w dużej mierze wierzycielami długu państw peryferii.

Jednak coraz więcej ekonomistów pyta dlaczego w przypadku Irlandii Unia zdecydowała się zamienić prywatny dług na publiczny? Marginal Revolution cytuje prof. Paul DeGrauve ( z tekstu „A Mechanism of Self-Destruction of the Eurozone”), który uważa, że UE stała się, wskutek tej decyzji, bardziej podatna na kryzysy. Jego zdaniem to dług banków i gospodarstw domowych rósł niemal w sposób niekontrolowalny, a dług publiczny był utrzymywany na racjonalnym poziomie.

Surprisingly, the only sector that did not experience an increase in its debt level during that period was the government sector, which saw its debt decline from 72 to 68% of GDP. Ireland and Spain, two of the countries with the severest government debt problems today, experienced the strongest declines of their government debt ratios prior to the crisis. These are also the countries where the private debt accumulation was the strongest.

Interesującą myśl podsuwa jeden z czytelników w dyskusji pod postem.

European leaders probably recognized then that their banking system was overleveraged, and they may need to cut government programs (or raise taxes) to shoulder new private debt from the the private banking system.

In other words, they never believed, nor could you have rationally believed, that there was really a plan to for the Europeans to „austere” their way out of a recession.

All three have high net foreign liability positions, liabilities are highly concentrated through banks who are borrowing overseas, all three have experienced some form of housing boom and lift in consumption, and finally all three appeared to have a relatively strong fiscal position before the GFC before moving into fiscal deficits after the shock. And yet (so far) while the Irish and Greek economies and banking systems have collapsed, New Zealand’s has been fine.

Jednak Nowa Zelandia sprywatyzowała wszystkie banki, a jej stopy procentowe są płynne. I większość długu została zdenominowana w nowozelandzkim dolarze. (Na ten temat także Matt Nolan).

Jeden z dobrze poinformowanych ekonomistów-analityków na temat sytuacji gospodarczej Chin Vitaliy Katsenelson uważa, że wzrost gospodarczy Chin oparty jest na nietrwałych podstawach. Chiński rząd zarządza kapitałem tak by realizować krótkoterminowe cele. Katsenelson przytoczył przykład budowania osiedli mieszkalnych, z których nikt nie mieszka. Jedno z nich, Ordos, które do dziś stoi puste, dla 1,5 mln mieszkańców powstało w środkowej Mongolii.

The vacancy rate on commercial real estate in China is fairly high, but they still keep on building new office buildings because they think they will always grow. So therefore as long as they keep building, that activity will be registered as growth, until they stop. And when they do stop, they’ll drown in overcapacity, and they won’t be building new skyscrapers for a very long time.

Katsenelson nazywa China superbańką.

Dla tych ekonomistów, którzy nie ufają statystykom chińskim poleca inną metodę obserwacji gospodarki. Przylądanie się danym: zużycia elektryczności (spadła w czasie recesji), sprzedaży żywności w restauracjach fast-food, ilość towarów transportowanych koleją a także sprzedaży amerykańskich i europejskich firm w Chinach.

"If the auto industry collapses, Germany will collapse," writes Gabo Steingart emphatically in a recent article in Focus magazine. Many experts and commentators are increasingly drawing attention to the waning strength of Germany's flagship industry. German automotive has missed the electric age. Is it just a slightly longer pit-stop or is it irretrievably losing "pole position"?

Współczesną rzeczywistość charakteryzuje szybki postęp. Dynamiczny rozwój technologii informatycznych i cyfryzacja gospodarki wymuszają zmiany także w funkcjonowaniu systemu płatniczego i w samych płatnościach. Zjawisko to ma zasięg globalny. Dotyczy również strefy euro. W dyskusji publicznej pada pytanie, czy po 25 latach od wprowadzenia banknotów i monet euro nadszedł już czas na równoległe wprowadzenie przez Eurosystem (tj. Europejski Bank Centralny i 20 banków centralnych państw strefy euro) cyfrowego odzwierciedlenia gotówki?

Globalne rynki finansowe stają się coraz bardziej powiązane ze sobą. Nasz artykuł analizuje potencjalne skutki uboczne wstrząsów pochodzących z Chin dla rynków finansowych gospodarek wschodzących, z rozróżnieniem zakłóceń związanych z polityką pieniężną i tych związanych z rozwojem makroekonomicznym Chin.

Rośnie PKB, spada inflacja – listopadowa projekcja Departamentu Analiz i Badań Ekonomicznych NBP przynosi dobre wiadomości. Za tempo wzrostu gospodarczego mają odpowiadać głównie środki z KPO, a inflację w ryzach utrzymywać towary z Chin.

Niegdyś odległa perspektywa Dnia Kwantowego (Q-Day) – momentu, w którym komputery kwantowe złamią globalne szyfry – stała się horyzontem bieżącej dekady, przesuwając ryzyko technologiczne na czoło strategicznych zagrożeń dla stabilności makroekonomicznej.

W drugim tygodniu października 2025 zostały wręczone Nagrody Nobla. W całej historii Nagród 67 razy otrzymały ją kobiety, ale jedynie trzy w dziedzinie nauk ekonomicznych. Pierwszą, która otrzymała Nagrodę w dziedzinie nauk ekonomicznych, po czterdziestu latach od jej utworzenia, była Elinor Ostrom.

Objęcie urzędu premiera przez pierwszą kobietę w Japonii, spadkobierczynię powszechnie szanowanego Shinzō Abe, pobudza nadzieje na przełamanie długoletnich negatywnych trendów w gospodarce tego kraju. Nie będzie to łatwe, zważywszy na starzejącą się szybko populację, ogromny dług, duże uzależnienie od paliw kopalnych i mało stabilne globalne otoczenie.

Dla Duńczyków to jest szok, że rząd nagle im mówi, że powinni mieć w domu i gotówkę, i radio na baterie, i dodatkową żywność w puszkach. Świadomość niepewnej sytuacji geopolitycznej rośnie i będzie wpływała na naszą gospodarkę – stwierdził w rozmowie z „Obserwatorem Finansowym” Jan Størup Nielsen, dyrektor Nordea Markets.

Czym jest inwestowanie odpowiedzialne społecznie? Czy można na nim zarabiać i w jaki sposób? Na te i wiele innych pytań związanych z tematyką ESG odpowiada skrzyżowanie monografii z poradnikiem „Zrównoważone inwestowanie. Wszystko, co warto wiedzieć” autorstwa H. Kenta Bakera, Huntera M. Holzhauera i Johna R. Nofsingera.

Rosja od lat starannie przygotowywała swoją gospodarkę na czas konfrontacji z Zachodem. Sankcje, które zostały nałożone na nią po inwazji na Ukrainę, nie przyniosły spodziewanego rezultatu. Czy „forteca Rosja” jest odporna na presję i czy jest bliska samowystarczalności, jak chciałby tego Putin, czy może znajduje się już na krawędzi załamania?

Wodór to paliwo przyszłości, ale jego przechowywanie i transport to ogromne wyzwania. O bezpieczeństwie, nowoczesnych materiałach i szansach Polski na rozwój technologii wodorowych mówi prof. Mariusz Krawiec, kierownik Katedry Fizyki Powierzchni i Nanostruktur w Instytucie Fizyki na Wydziale Matematyki, Fizyki i Informatyki UMCS w Lublinie.

Gotówka to wolność? A może zbędny, trącący myszką, relikt? Jak przekonuje Brett Scott w książce „Cloudmoney”, to jeden z niezbędnych aspektów niezależności w wymiarze społecznym i indywidualnym.

Wenezuela posiada najbogatsze na świecie zasoby ropy. Jednocześnie od ponad dekady (z wyjątkiem lat 2020 i 2024) dzierży tytuł kraju o najwyższej stopie inflacji. W tym samym czasie jej PKB skurczył się o ponad 80 proc. O przyczynach wenezuelskiej katastrofy gospodarczej napisano już niemal wszystko, a mimo to mnożą się pytania, jak chociażby to, czy odpowiadają za nią jedynie czynniki ekonomiczne.

Polska chce zablokować umowę o wolnym handlu z krajami Ameryki Południowej. Powodem są głównie obawy rolników o konkurencyjność ich produktów. W jaki sposób realizacja umowy z Mercosur może wpłynąć na unijne rolnictwo i jakie mogą być też jej inne skutki?

Czy Polska rzeczywiście dokonała gospodarczego cudu? Ostatnie trzy i pół dekady pokazują, że odpowiedź może być tylko jedna – tak. Nowy numer kwartalnika „Obserwator Finansowy” to opowieść o sukcesie, który nie wydarzył się w naszej gospodarce sam, ale był efektem odwagi, determinacji i pracy całego społeczeństwa. A także o wyzwaniach, które dopiero przed nami.

Rosnące napięcia geopolityczne, demontaż globalnych łańcuchów dostaw, protekcjonizm, wojny handlowe i ekspansja sztucznej inteligencji coraz mocniej kształtują nowy, wielobiegunowy ład gospodarczy. Najnowszy numer kwartalnika Narodowego Banku Polskiego stawia pytania o przyszłość światowej gospodarki.