Irlandia dostała pomoc. Przed zapoznaniem się z reakcjami ekonomistów na ten fakt warto sprawdzić, jak swoją opinię na temat euro zmodyfikował największy zwolennik unii walutowej wśród amerykańskich keynesistów - prof. Barry Eichengreen.

Profesor dzieli się swoimi przemyśleniami dotyczącymi metod zapobiegania następnym kryzysom. I zaleca głębszą integrację finansową w Unii poprzez zwiększenie przejrzystości finansów publicznych w poszczególnych krajach. Eichengreen proponuje ustanowienie komisji ds. polityki fiskalnej, które określałyby poziom długu publicznego i deficytu.

They can create independent fiscal councils with the power to set debt and deficit limits. They need to work on the problem at the national level. Only this will solve the fiscal problem once and for all.

Profesor doradza też wprowadzenie bardziej restrykcyjnych regulacji, które pozwolą uniknąć boomu na rynku nieruchomości wywołanego przez rynki finansowe. Według niego, należałby stworzyć mechanizm restrukturyzacji trudnych do spłacenia rządowych długów.

Barry Eichengreen jeszcze rok temu o tej porze był przekonany, iż żaden kraj nie wyjdzie (zostanie wyrzucony) ze strefy euro. Dziś uważa, że prawdopodobieństwo tego zdarzenia nie wynosi zero. Niektóre państwa mogą zechcieć wprowadzić ponownie swoją walutę do obiegu bez względu na konsekwencje. Jednak prof. Eichengreen wciąż jest przekonany, iż euro wyznacza pewien proces historyczny integracji, która nie zostanie zatrzymana.

If there’s a run on your banking system anyway, then the deterrent to action no longer applies. If there’s a run on your banking system and you have to close down your banks and financial markets anyway, you may want to take that opportunity to reintroduce your own currency. I still don’t think that things will be allowed to get to this point, but I no longer attach a zero probability to a country’s exiting the euro – just a close to zero probability. Never say never, but I still believe that the euro is an example of a path-dependent historical process that is unlikely to be reversed.

Prof. Eichengreen nadal podtrzymuje swoje zdanie, iż wyjście ze strefy euro może być bardzo kosztowne. Dewaluując walutę można nie poradzić sobie z kosztami spłaty nawet zmniejszonych długów ze względu m.in. na ucieczkę inwestorów. I co gorsza, doprowadzić do prawdziwego kryzysu wywołując panikę na rynku.

(…)if the Greek government were to announce tomorrow that it had decided to reintroduce the drachma, it would precipitate the mother of all financial crises. Everyone would know that its intention was to depreciate the new drachma, so in the first minute everyone would rush to get their money out of the country, out of its banks, and out of its bond market. The result would be the biggest bank run and financial crisis the world has ever seen. This danger is a formidable deterrent to even contemplating going down this road.

Prof. Eichengreen rekomenduje 5 książek, które – jego zdaniem – umożliwiają zrozumienie idei wspólnej waluty.

- Tony Judt, Postwar: A History of Europe Since 1945

- David Marsh, The Euro: The Politics of the New Global Currency

- Peter Hall i David Soskice, Varieties of Capitalism

- Marco Buti, The Euro: The First Decade,

- Alberto Alesina i Francesco Giavazzi, Europe and the Euro, esej: Barry. Eichengreen, The Breakup of the Euro Area

W wywiadzie z Fivebooks profesor dzieli się ciekawą obserwacją, iż politycy, którzy nie przeżyli tragedii II wojny światowej, mogą nie potrafić kontynuować dzieła integracji europejskiej.

Calculated Risk przypomina informacje opublikowane przez Allied Irish Banks i Governor and Company of the Bank of Ireland, iż irlandzkie banki przeszly stress testy (The Central Bank and Financial Regulator CEBS July 2010 Stress Test Results Allied Irish Banks plc).

The exercise was conducted using the scenarios, methodology and key assumptions provided by CEBS. As a result of the assumed shock under the adverse scenario, the estimated consolidated Tier 1 capital ratio would change to 7.2% in 2011 compared to 7.0% as of end of 2009. An additional sovereign risk scenario would have a further impact of 0.70 of a percentage point on the estimated Tier 1 capital ratio, bringing it to 6.5% at the end of 2011, compared with the CRD regulatory minimum of 4%.

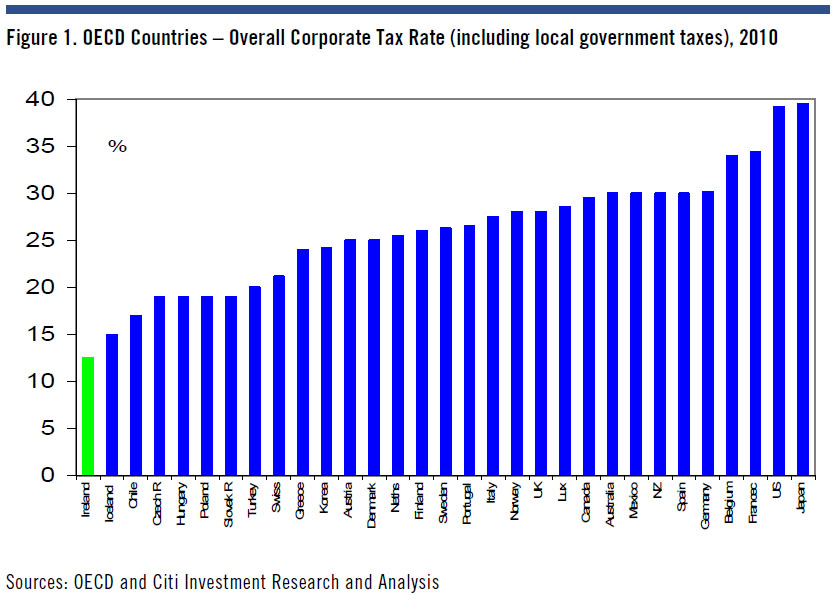

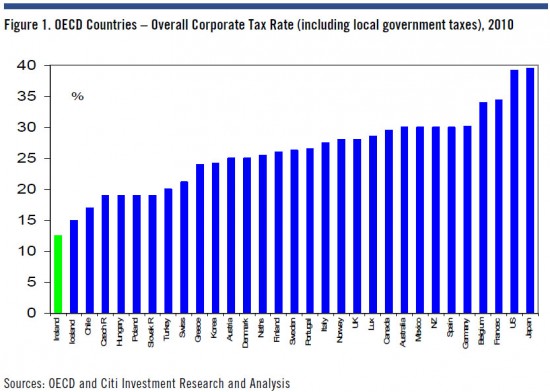

Zero Hedge twierdzi, iż Irlandia podwyższy podatki, zwłaszcza korporacyjny. Tak wynika z zapowiedzi komisarza Oli Rehna. Zero Hedge twierdzi, iż nie jest oczywiste, jakie będą tego konsekwencje dla gospodarki.

Either of these options will have a negative outcome to corporate cash flows and EPS in the short term, and in the case of i), to the balance sheet as well (in the case of Google potentially costing the firm up to $100/share in embedded benefits as discussed elsewhere). We are just surprised that so far the market has been rather oblivious to the possibility that Ireland will have to ultimately cave the interests of its new banking overlords.

Felix Salmon dokonuje rachunku, ile z sumy wykupu zaoferowanej przez EU wystarczy na wydatki rządu irlandzkiego. Według niego suma wykupu jest stanowczo za mała, zwłaszcza środki (15 mld) przeznaczone dla banków. Bo wartość czarnej dziury w nieruchomościach komercyjnych wynosi 50 mld.

When a residential property bubble as big as Ireland’s bursts, there will be always enormous bank losses. But because those losses haven’t materialized yet, everybody in Ireland and the EU is sticking their heads in the sand, pretending that they’re never going to arrive at all.

Business Insider przekonuje trzema argumentami, dlaczego tzw. wykup Irlandii nie będzie operacją skuteczną. Przede wszystkim umowa nie zawiera żadnych szczegółów. Zaproponowane środki pomocowe są niewystarczające, a oszczędności budżetowe nie pomogły dotąd Irlandii. W jaki sposób miały pomóc tym razem?

Po wykupie Irlandii rodzi sie naturalne pytanie, kto nastepny? Pragmatic Capitalism publikuje fragment informacji Danske Bank, iż kolejnych turbulencji rynkowych powinna się spodziewać Portugalia. Analitycy obawiają się jednak, że kryzys może ponownie objąć Hiszpanię i Wlochy. Jeśli Wlochy potrzebowałyby wykupu analitycy nie wykluczają, że mogłoby się to skonczyć wyjściem ze strefy euro kilku krajów.

It is debatable how much lending is really available from the EFSF. Given that Greece, Ireland and others being helped will not contribute and also that the guarantee must be 120% of lending and that it is the guarantee that adds up to the EUR440bn in the EFSF, there is only around EUR350bn available for lending by the EFSF. In addition there is EUR60bn in the stabilization mechanism and EUR30bn + EUR175bn (50% of EUR350bn) from the IMF. Consequently, around EUR600bn should be on the table, enough to help Ireland, Portugal and Spain (Greece has its own EUR110bn package). But Italy is not affordable. Italy’s funding requirement is five times that of Greece, and there are fewer countries left to help out the bad apples (Italy and Spain are the 3rd and 4th largest economies in the euro area). If Italy needs to be bailed out we will need to consider scenarios including less orderly defaults and the possible exit from the euro area for one or more countries.

Intelligence Europe pisze, że niemiecki minister finansów powiedział w środę na forum Bundestagu, iż euro może nie przetrwać kryzysu.

the German finance ministry, (..) he told the Bundestag that the euro might not survive the crisis. As Reuters reports from he said: „I’d like to make clear that our joint currency is at stake and we have to take over responsibility,” but then went on to propose austerity, and more austerity as the solution to this crisis.

Wiele wskazuje więc na to, że – jak mawiał prof. Milton Friedman – kapitalizm bez bankrutów jest jak katolicyzm bez piekła.

Opracował: Tomasz Pompowski